{kind=link}

[ad_1]

Below time strain to avoid wasting taxes, you purchased a conventional life insurance coverage plan within the final week of March with an annual premium of Rs 1 lac. After a few months, while you bought time to evaluation the product, you didn’t prefer it any bit.

You wished to do away with the plan, however the free-look interval was already over.

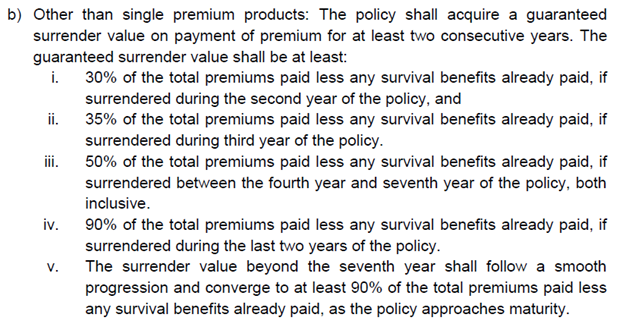

And while you checked with the insurance coverage firm in regards to the give up prices, you had been politely informed that you simply wouldn’t get something again since you have got paid only one premium. Your woes didn’t finish there. Even in the event you had the endurance and cash to pay a couple of extra premium installments, you don’t get a lot aid. Within the preliminary years, in the event you give up, you gained’t get greater than 30-40% of the whole premiums paid again.

Don’t know whether or not to name this good or dangerous. Many traders persist with such plans (regardless of not liking them) merely due to the give up prices. The nice half is that such heavy give up costs assist traders persist with the funding self-discipline and develop their financial savings.

The dangerous half is that such exorbitant exit penalties take the freedom away from the traders.

What in the event you later notice that the product just isn’t good for reaching your targets? Or that the product gives extraordinarily low returns?

What in the event you later notice that you simply signed up for too excessive a premium?

You’re simply caught. Can’t do something. And that’s by no means good from prospects’ perspective.

However why are the give up prices so excessive?

The first purpose is the front-loaded nature of commissions within the sale of conventional insurance coverage merchandise. “Entrance-loaded” means the majority of the compensation for the sale is paid within the preliminary years. For example, within the sale of conventional life insurance coverage merchandise, the first-year fee might be as excessive as 40% of the annual premium.

Now, in the event you had been to give up the plan inside a few years and the commissions can’t be clawed again, who will bear the price of refunding you the premiums? Therefore, you’re penalized closely in the event you give up the plan.

The front-loaded nature of commissions additionally encourages mis-selling on the a part of insurance coverage brokers and intermediaries. I’ve thought-about so many circumstances of blatant mis-selling by insurance coverage intermediaries, particularly the banks, on this weblog.

I’m NOT saying that every one insurance coverage brokers and intermediaries are dangerous. Am certain there are numerous who’re doing a beautiful job. However I have to say that the gross sales incentives and the traders’ pursuits are misaligned.

What’s the IRDA saying about give up prices?

IRDA realizes that every little thing just isn’t proper with conventional life insurance coverage gross sales. Give up prices being one among them. The exit prices are simply too excessive and can’t be justified.

Why does the investor should lose all or say 3/4th of the cash if he/she doesn’t just like the product?

Therefore, IRDA has proposed a change. Only a proposal. Has invited feedback. Nothing is closing.

- There shall be threshold premium on which give up costs will apply.

- Any extra premium above that threshold is not going to be topic to give up costs.

Allow us to perceive with the assistance of an illustration. And I take the instance from the IRDA proposal itself.

Allow us to say the annual premium is Rs 1 lac.

And the edge is Rs 25,000.

You may have paid premiums for 3 years. Rs 1 lac X 3 = Rs 3 lacs whole premium paid.

Therefore, give up costs will apply solely on 25,000 X 3 = Rs 75,000.

Let’s say you will get solely 35% of such premium again in the event you give up after 3 years.

So, of this Rs 75,000, solely 35% shall be returned. You get again Rs 26,250.

The remaining (1 lac – Rs 25,000) X 3 = Rs 2.25 lacs gained’t be topic to give up costs.

Therefore, the web quantity returned to you = Rs 2.25 lacs + 26,250 = Rs 2,51,250. This worth is named Adjusted Assured Give up Worth and shall be the minimal give up worth.

The Give up Worth shall be greater of (Adjusted Assured Give up Worth, Particular Give up Worth).

Unsure how the Particular Give up worth is calculated. So, let’s simply deal with the Adjusted Assured Give up Worth.

It is a huge enchancment over what you’ll get in the event you had been to give up an present coverage now.

Whereas I’ve been fairly important of IRDA prior to now, I have to say that is a particularly buyer pleasant proposal from IRDA.

What would be the Threshold Premium?

It’s not but clear how this “Threshold” can be calculated or arrived at.

It might be an absolute quantity or a share of annual premium. Or a combined strategy.

The decrease the edge, the higher for traders.

As I perceive, the insurers can have the discretion to determine the edge quantity.

The IRDAI has set broad guidelines for minimal give up worth. Copying an excerpt from the proposal.

Frankly, tells nothing about how the edge can be arrived at.

I’m additionally undecided whether or not IRDA is referring to “Whole Premiums paid” or the “Whole Relevant Threshold Premium” when it mentions “Whole Premiums”. Whether it is “Whole premiums paid”, then this proposal might not account for a lot. Insurers can merely hold the “Threshold Premium” fairly excessive.

We must wait and see.

Not everybody will like this

As talked about, IRDA has simply floated a proposal and invited feedback.

The insurance coverage firms is not going to like this. The insurance coverage brokers/intermediaries is not going to like this both.

Therefore, anticipate a pushback from the insurance coverage trade.

However why?

If the give up costs are certainly decreased (as proposed), it might be troublesome to maintain the front-loaded nature of commissions in conventional plans. Or the insurance coverage firm must introduce claw again provisions within the conventional plans. Both method, their distribution companions (insurance coverage brokers) gained’t like this. And incentives change every little thing. Will the insurance coverage brokers be as inclined to promote conventional plans if the preliminary commissions usually are not so excessive?

We must see if this proposal sees the sunshine of the day. There shall be pushback from the trade. We must see if IRDA can maintain towards all of the strain with out diluting the provisions of the proposal. As I discussed within the earlier part, a small play on definition/interpretation of “Threshold premium” can render the change ineffective.

Keep in mind LIC can also be affected, and it sells a variety of conventional life insurance coverage.

We are going to quickly discover out.

By the way in which, would this alteration (if accepted) make conventional plans extra engaging to take a position?

No, it doesn’t.

This particular change solely pertains to give up of insurance policies. Nothing adjustments in the event you plan to carry till maturity. Therefore, in the event you should spend money on such product, make investments on benefit.

Further Learn/Hyperlinks

Publicity Draft-Product Laws 2023 dated December 12, 2023

Disclaimer: Registration granted by SEBI, membership of BASL, and certification from NISM under no circumstances assure efficiency of the middleman or present any assurance of returns to traders. Funding in securities market is topic to market dangers. Learn all of the associated paperwork fastidiously earlier than investing.

This put up is for schooling function alone and is NOT funding recommendation. This isn’t a suggestion to take a position or NOT spend money on any product. The securities, devices, or indices quoted are for illustration solely and usually are not recommendatory. My views could also be biased, and I could select to not deal with facets that you simply think about essential. Your monetary targets could also be totally different. You could have a special danger profile. You might be in a special life stage than I’m in. Therefore, you will need to NOT base your funding choices based mostly on my writings. There isn’t a one-size-fits-all resolution in investments. What could also be funding for sure traders might NOT be good for others. And vice versa. Due to this fact, learn and perceive the product phrases and situations and think about your danger profile, necessities, and suitability earlier than investing in any funding product or following an funding strategy.

[ad_2]