{kind=link}

[ad_1]

What’s going to 2024 carry? It may be enjoyable to make predictions about what’s to come back (The Bear besting fan favourite Ted Lasso for excellent comedy sequence? A Tremendous Bowl with out the Kansas Metropolis Chiefs & Taylor Swift?), however the considered an unsure future can even carry anxiousness. Elections and the adjustments they could carry, together with ongoing geopolitical tensions and questions concerning the Fed’s rate of interest coverage and its influence on the economic system are sufficient to invoke nerves in even probably the most assured buyers heading in to 2024.

The excellent news is that our monetary success over the long run doesn’t should be decided by these externalities. Whether or not you might be accumulating wealth for objectives like retirement or making a legacy, having fun with the life-style that your wealth allows, otherwise you simply need to be financially unbreakable, constant conduct and a concentrate on what’s in our management is vital. Learn on for some issues to contemplate as the brand new yr unfolds.

1. Save & Make investments No Matter the Atmosphere

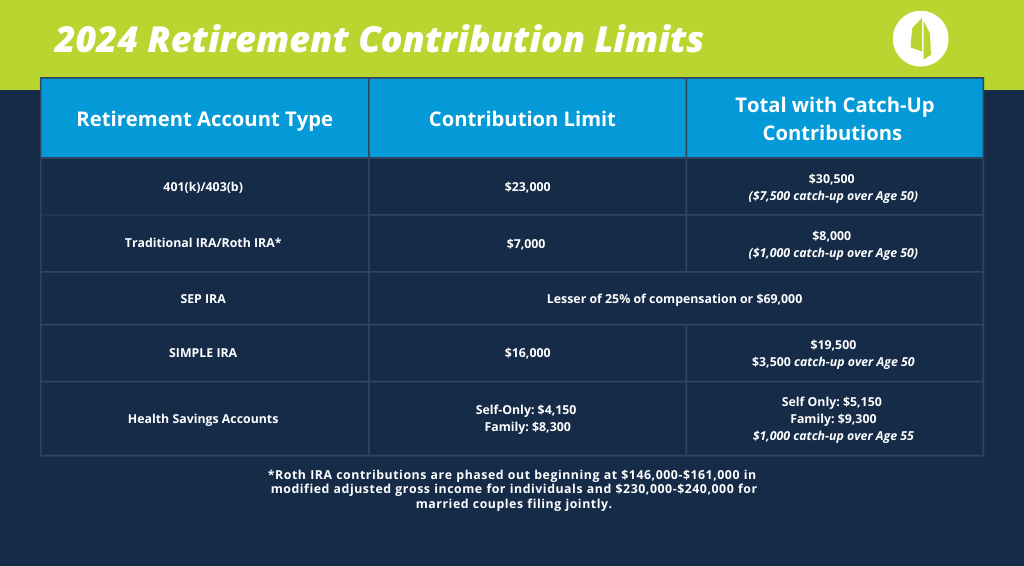

The beginning of the yr is a good time to overview present contribution limits for tax-deferred accounts like retirement accounts and Well being Financial savings Accounts. Ensure you are set to effortlessly maximize these as you’re able. Establishing common automated contributions to retirement and even taxable funding accounts makes it extra doubtless that you’ll proceed investing and never get derailed when issues get robust available in the market. Automated doesn’t imply “set it and overlook it” although. Contribution limits change yearly, and numerous provisions of the Safe Act 2.0 kick in over a variety of years, altering the retirement financial savings panorama.

2024 Contribution Limits:

Just a few issues to know from the Safe Act 2.0 in 2024 and past:

- Employers can begin making Roth matching contributions to an worker’s 401(ok). Beforehand, employers may solely make matching contributions on a pre-tax foundation. Not all employer plans have a Roth choice – however this will compel extra companies to incorporate this of their plan design.

- Excessive revenue earners over 50 have a number of extra years earlier than catch-up contributions to a 401(ok) are required to be Roth vs. pre-tax. This provision was supposed to start in 2024, limiting a chance for these whose wages exceeded $145,000 in 2023 to cut back their taxable revenue with pre-tax contributions past the usual 401(ok) deferral restrict.

- Catch-up contributions for IRAs and Roth IRAs will enhance with inflation in $100 increments somewhat than remaining a flat $1,000/yr beginning in 2024.

- By 2025, catch-up contributions to office retirement accounts will enhance much more for these between 60-63, permitting you to save lots of extra in what could also be your highest-earning years. The improved catch-up would be the better of $10,000 or 150% of the catch-up contribution quantity from the earlier yr. Remember that the Roth catch up guidelines will apply to these with wages above a specific amount (doubtless $145,000 adjusted for inflation).

2. Get a Deal with on Spending & What’s Regular Past Inflation

It’s been simple in charge increased spending on inflation the previous few years. Nonetheless, inflation doesn’t inform the complete story. Life-style creep occurs very simply, particularly as salaries enhance every year. As you begin to make more cash, you doubtless start spending more cash with out actually feeling like issues have modified. One of many largest drivers we see relating to long-term success of a wealth design is spending, which is one thing all of us have management over to some extent. In case your revenue has elevated through the years however your saving hasn’t, it could be time to take a step again and get a deal with on the place the cash goes, ensuring that it’s consistent with your reply to the query “What’s the cash for?” not solely in the present day however sooner or later. Larger spending isn’t essentially a foul factor (and a latte right here and there isn’t going to derail the high-income earner’s monetary success it doesn’t matter what fashionable media personalities let you know) – it’s simply one thing to pay attention to and perceive the way it impacts your potential to fulfill your objectives over a lifetime.

3. Maximize the Advantages of a Traditionally Excessive Exemption for Present & Property Taxes

As of now, elevated lifetime present and property exemption quantities ($13.61M/individual in 2024) are set to run out on the finish of 2025 if Congress doesn’t act to increase them. I gained’t opine on the probability of Congress passing something to increase them, as it could really be anybody’s guess. For those who’ve collected important wealth over your lifetime and also you need to see that wealth profit the subsequent era with minimal tax influence, 2024 will be the yr to take motion or not less than begin creating a plan so that you simply perceive how a lot your property could develop over time and what choices can be found to you to cut back it in a manner that means that you can stability your priorities.

- Annual gifting to family members when you are residing might be a good way to cut back your property over time whereas additionally seeing their enjoyment of the present. In 2024, you can provide as much as $18,000 to anyone particular person ($36,000 for married {couples}) with out submitting a present tax return.

- If offering funds for training for the subsequent era is essential, 529 contributions might be a good way to earmark funds for that objective and likewise make a large present (5 years’ price of the exclusion quantity) suddenly.

- Irrevocable trusts, reminiscent of Spousal Lifetime Entry Trusts (SLATs), can also be an choice for these whose property exceed the exemption quantity who even have ample property to fulfill their private spending objectives while not having any property transferred to a belief. These trusts might be advanced and require deep thought relating to deciding the way you need the funds to profit your family members – getting began now will enhance the probability that you simply and your lawyer can execute a belief and fund it with time to spare earlier than the tip of 2025.

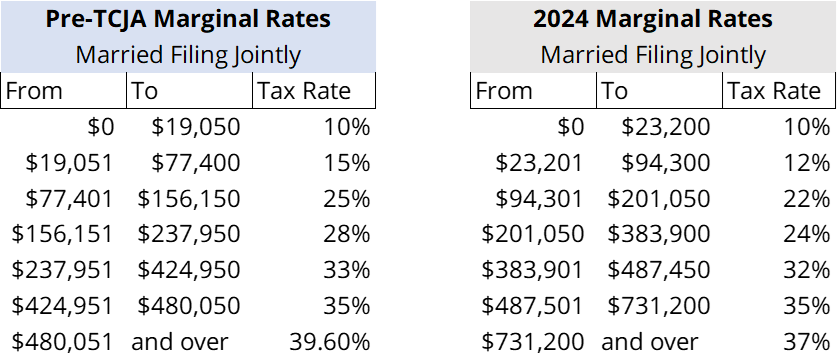

4. Begin Planning for Larger Taxes

Much like the upper exemption quantities, our present tax brackets are reflective of the Tax Cuts and Jobs Act handed in 2017 and are set to sundown on the finish of 2025. Whereas the pre-2017 brackets can be adjusted for inflation, it’s doubtless that extra of your revenue can be topic to increased tax charges than they’re in the present day by 2026. Somebody within the 24% bracket in the present day may simply see a very good quantity of their revenue taxed at 33% after we revert again to pre-2017 brackets, decreasing the disposable revenue they’ve grown accustomed to with decrease tax charges and impacting the quantity of portfolio property which can be really obtainable for spending sooner or later vs. being a tax legal responsibility.

Pre-TCJA Brackets vs. 2024 Brackets:

- Larger charges aren’t the one piece of the puzzle – increased deductions can also be allowed after 2026 for individuals who have been restricted to $10,000 in deductions for state and native taxes and property taxes (SALT), bringing total taxable revenue down.

- Those that are comfortably within the 24% bracket now could need to take into account changing pre-tax retirement cash (Conventional IRAs and 401(ok)s) to Roth, paying taxes at in the present day’s charges on distributions vs. unsure future tax charges. It gained’t take a lot in retirement revenue to drive increased tax charges sooner or later if there isn’t an extension of present charges or some future tax reform.

- For these over the age of 70 ½ who don’t count on to wish all of their IRA cash for his or her private spending, Certified Charitable Distributions as much as $105,000 could also be made. This might help meet a charitable intent and likewise cut back the quantity of taxable revenue that have to be distributed from pre-tax retirement accounts.

- There’s no higher time than the current to take a look at your funding portfolio and the way it’s managed to make sure tax effectivity if you’re a high-income earner.

5. Evaluate Dangers Past the Market

Many individuals solely take into consideration inventory market returns as a supply of danger relating to assembly their monetary objectives. The fact is that on a regular basis life presents dangers that may change the monetary image in a single day in the event that they aren’t deliberate for and managed. Whereas we are able to’t management what’s going to occur to us, we are able to management how we shield ourselves in opposition to danger. For those who haven’t checked out your insurance coverage portfolio shortly (life, property, legal responsibility, incapacity, and so forth.) now could be a very good time to brush off these coverage paperwork and overview them with knowledgeable who has your greatest curiosity in thoughts.

- Inflation has pushed up development prices, and many individuals took on dwelling enchancment tasks from 2020-2021 whereas rates of interest had been low. It’s doable that the substitute value in your property insurance coverage is inadequate and must be adjusted.

- Life occurs quick and we don’t all the time take the time to step again and reassess our wants. For those who’ve added kids to your loved ones, taken on liabilities, or skilled a big enhance in revenue that your loved ones depends on, you could want to ascertain or enhance your life insurance coverage protection.

Comply with Your Personal Plan & Path, Not Somebody Else’s Predictions

Your imaginative and prescient and plans for the longer term are uniquely yours, however it may be tempting to behave on the predictions which can be little doubt flooding your inbox and assaulting your ears this time of yr. Sticking to a wealth plan and specializing in the issues which can be in your management isn’t all the time enjoyable or glamorous, however it is going to have a excessive chance of success for serving to you get to the place you most need to go, no matter what’s happening on the earth round you. Partnering with a wealth advisor who understands your huge image and the aim of your wealth can go a good distance in serving to you achieve the readability to focus on the controllable elements of your monetary journey, paving the way in which for extra favorable outcomes. I hope that 2024 brings pleasure, prosperity, and wellness. If something right here resonated with you, make 2024 the yr that you simply prioritize actions that provide help to understand your wealth’s objective.

[ad_2]