{kind=link}

[ad_1]

That is the story of how I filed my 14-year-old daughter’s taxes, after which opened, funded, and invested a Roth IRA for her, for tax yr 2023. Piecing this course of collectively for the primary time was a bit irritating (even for a monetary planner!) so I hope you’ll be able to observe together with a bit extra ease.

It’s best to be aware that I’m not a tax skilled. I did my greatest to ask tax professionals for the correct approach to do that. (You wouldn’t consider how argumentative these of us might be! At the least, on Twitter 😉.) Seems, taxes aren’t only a bunch of goal guidelines. A number of subjectivity concerned!

I’m going to faux, for the sake of simplicity, that my daughter Alice has an Adjusted Gross Revenue (a line close to the underside of the primary web page of the 1040 tax return) of $1000 for 2023, which suggests she will be able to contribute $1000 to her Roth IRA for 2023. That’s not the identical as making $1000…however shut.

Why Would You Even Do That?*

Perhaps it’s apparent to you, however simply in case you’re all “However she’s fourteen. Regular individuals don’t do that,” let me clarify my causes for doing this.

The “Roth” Means No Revenue Taxes. Ever.

In case your little one earned below $13,850 (the usual deduction for a single tax filer in 2023), they’ll owe no federal revenue taxes. (They will owe FICA, i.e., Social Safety and Medicaid taxes. And also you’d need to examine your personal state’s guidelines, although I’m guessing your child received’t owe revenue taxes on low quantities of revenue.)

Alice earned far lower than $13,850 in 2023 and so doesn’t owe any revenue taxes. She does owe roughly $150 in FICA taxes (half as an worker, half as an make use ofer, as she was, technically talking, self-employed).

Often the cash you contribute to a Roth IRA is cash you’ve already paid taxes on. However as a result of all of her revenue is just not topic to (federal) revenue tax:

- The cash can go in income-tax free (a minimum of on the federal degree, and probably on the state degree).

- After we make investments it, it could develop tax-free.

- Ultimately if might be withdrawn tax-free.

That’s why Roth accounts are so nice for teenagers.

* Each time I write that sentence, I can’t assist however chortle. Final college yr, my husband was driving my daughter and her good friend house from center college. The women had attended intercourse ed that day, through which they’d discovered about totally different, ahhh, acts that consenting adults can have interaction in. The good friend introduced up one of many less-vanilla acts and exclaimed, in outrage, disgust, and disbelief, “Why would you even do that?!” This has grow to be, naturally, a catchphrase in my house.

Compounding over That Many Years Is Loopy Highly effective.

Maybe you’ve heard about how it’s best to make investments early as a result of the sooner you make investments, the better it’ll be to construct wealth. Compound development for the win! Properly, 14 is fairly rattling early.

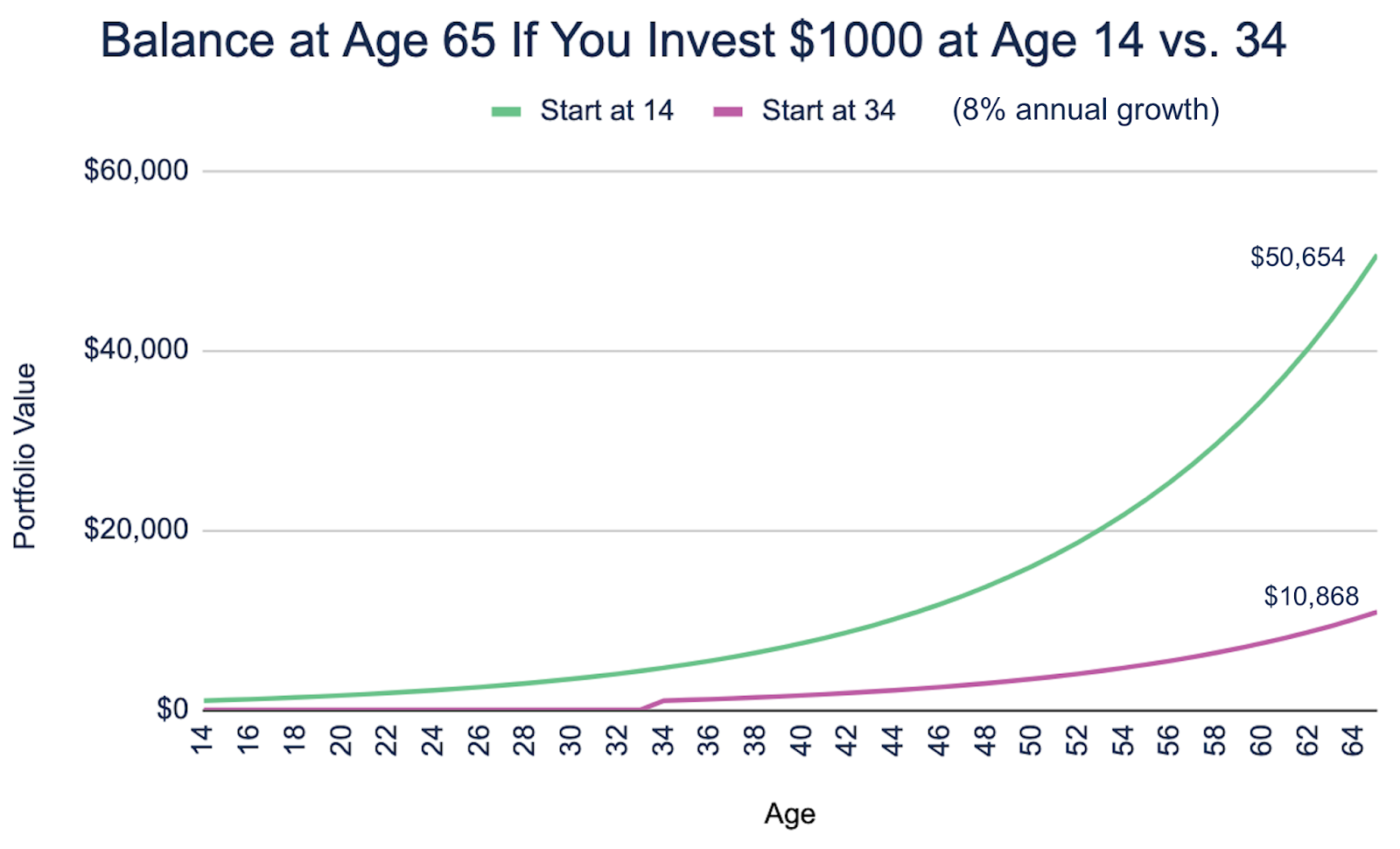

Right here’s a easy illustration of the affect. My daughter invests $1000 in her Roth IRA at age 14. In an alternate universe, she doesn’t begin investing that $1000 till she is 34 (twenty years later, however nonetheless fairly early by many individuals’s requirements for retirement financial savings!).

By age 65 (the stereotypical retirement age), you’ll be able to see how far more that $1000 has grown (assuming 8% common annual development), given 20 extra years of compounding: $50,654 vs $10,868.

You Begin Displaying Your Child at a Actually Younger Age The way to Do “All This.”

Whereas that ending worth (“Fifty Thousand {Dollars}!”) is enjoyable and all—extra so for my daughter than me (“Do you know how a lot retirement can price?!”)—I don’t care as a lot about that.

What I care extra about is that I’m beginning to present my daughter the way to take part on this financial system, and that I’m serving to her to create the behavior of saving and investing for the long-term.

I’m very a lot hoping that which means that, when she “launches” (my little lady! How are you going to be leaving the home in simply over 4 years!), a minimum of this a part of grownup life will come fairly naturally to her.

Oh taxes? Yep, that’s a factor I simply do. I keep in mind how maaaaaad mother used to get at how arduous it was to navigate that system. Ahhh, good occasions.

Oh, revenue? Yeah, I save an excellent portion of that.

Oh, financial savings? Yeah, I’ve a Roth IRA already for that, and I’ll simply preserve placing the cash into shares by way of a low-cost fund.

Does Your Child Have to Have a “Job” Job? Or Might They Simply Earn Cash Babysitting?

Your child can simply earn babysitting cash! Or lawn-mowing cash! Or, as my daughter did as soon as, spider-sitting cash! (Sure, actually.)

The bottom line is documenting the revenue.

In case your child has a “job” job, it’s apparent. Your child bought paychecks from the employer. If it was a W-2 job, revenue taxes and FICA taxes will have already got been withheld. Your child will obtain the W-2 tax kind from the employer after the top of the yr. Very like occurs for you and your job.

If it wasn’t a W-2 job, then you definitely’re in self-employment territory. The important thing right here is to doc your child’s revenue. In case your child labored for a corporation and acquired a 1099 from them, nice! There’s your documentation.

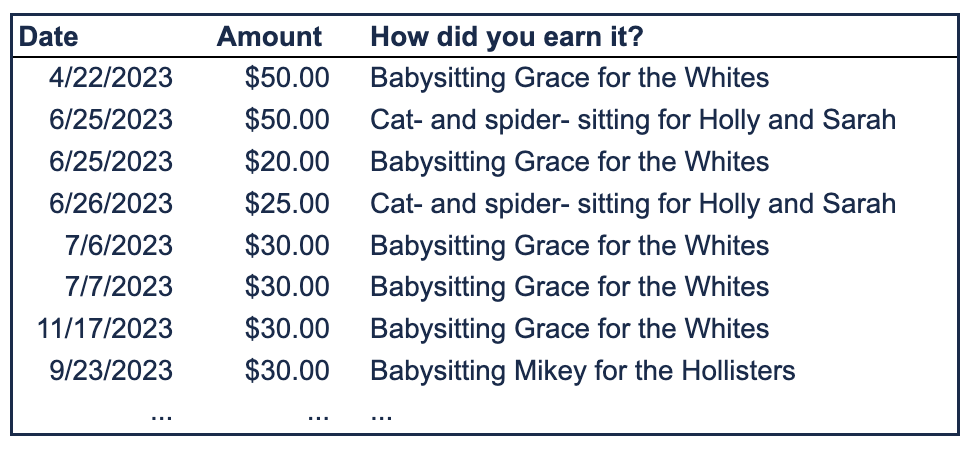

If it’s simply from babysitting and spider-sitting for varied households, then you must preserve monitor of the revenue your self. This was the case for us. Right here’s how we selected to do it.

I’ve a spreadsheet in my Google Drive entitled “Alice’s Earned Revenue,” with a tab for every year. After which each time she earns cash, I document the date, the quantity earned, and what the work was and for whom:

You Should File Their Taxes.

Loads of tax professionals on Twitter requested “Why would you file taxes for her?” However others reaffirmed my understanding that, if my daughter needs to make an IRA contribution, I’ve to doc her revenue by way of a tax return.

After a number of false begins (and skyrocketing stress ranges), I efficiently and principally fortunately adopted the suggestion to make use of freetaxusa.com, which lets you put together your federal tax return totally free. State returns price cash. (However ha ha! I foxed them! We stay in Washington, which doesn’t have a state revenue tax!)

As a result of this was my daughter’s first time submitting a tax return, and in addition as a result of she was below 16, we needed to print and mail the tax return, together with a paper verify. That was irritating however not too onerous. Hopefully subsequent yr we will do a minimum of the fee digitally as a result of she’ll be within the IRS system?

Should you work with a tax skilled, you would contemplate asking them to do it. I do work with an excellent CPA agency, however I wished to do that myself in order to contain my daughter.

The Greatest Tax Gotcha…for Mother and father!

One factor most tax professionals warned me about is that

you have to point on the child’s tax return that they’re a dependent of another person.

(You, it seems.) Should you don’t do that, your tax return might be rejected (or no matter the correct time period is), since you’re claiming your child as a dependent…and but they’re saying they’re not a dependent. This, not surprisingly, creates a stupidly giant headache for you and/or your tax preparer.

Additionally, in case you have a tax skilled put together your taxes, you’ll want to inform them what you’re doing.

Open, Fund, and Make investments the Roth IRA.

I opened a “custodial” Roth IRA for my daughter. She’s not 18 but and subsequently can’t personal her personal accounts.

I opened it at Constancy. Though most of my investments are at Vanguard, they continue to be there solely due to inertia and worry of what administrative disaster I’ll deliver on myself if I attempt to transfer them. (Vanguard’s buyer expertise has been atrocious for years.) I’ve been a monetary planner lengthy sufficient to know that monetary forms is punishing.

I discover Constancy’s buyer expertise to be about one of the best there’s on the market for shoppers, of the established gamers. (I solely use monetary organizations which were round for some time and are steady. Why? I bought burned by attempting to make use of a start-up-y fintech device just a few years in the past. Behold that candy UX! It was simple! And free! Then they madly pivoted pivoted pivoted…pivoted straight away from the rationale I used to be utilizing them.)

I moved the cash in, and, together with her blessing, invested it in VTI (Vanguard’s Complete US Inventory Market Index fund). (Don’t contemplate this a suggestion that you simply put money into VTI.)

You Can “Match” Their Contributions.

To place the non-public finance-nerd icing on the non-public finance-nerd cake, the ultimate factor you are able to do is match your little one’s Roth IRA contributions. Of the $1000 Alice places into her Roth IRA, we, her loving mother and father, will contribute $500 of that. Cash is, as she likes to say, fungible, in spite of everything. All that $1000 doesn’t must be her cash.

I’ve an in depth household good friend (hello, Taylor!) who does the matching for his granddaughter. So, perhaps that is one thing {that a} finance-nerd grandparent or different liked considered one of yours can get in on.

In closing, my daughter was happy to know that she was being featured in a weblog publish, however insisted that there’s a value to make use of her identify and story. So, right here goes: Sure, Alice, I do love you greater than your sister.

Do you need to assist your little one construct good monetary habits and a strong monetary basis as an grownup? Attain out and schedule a free session or ship us an e mail.

Join Movement’s twice-monthly weblog e mail to remain on prime of our weblog posts and movies.

Disclaimer: This text is offered for academic, normal info, and illustration functions solely. Nothing contained within the materials constitutes tax recommendation, a suggestion for buy or sale of any safety, or funding advisory companies. We encourage you to seek the advice of a monetary planner, accountant, and/or authorized counsel for recommendation particular to your scenario. Replica of this materials is prohibited with out written permission from Movement Monetary Planning, LLC, and all rights are reserved. Learn the complete Disclaimer.

[ad_2]