{kind=link}

[ad_1]

As Girls’s Historical past Month attracts to a detailed, a brand new Goldman Sachs report discovered one-third of girls are saving lower than $50,000 for retirement.

“Assuming a 4% withdrawal fee, $50,000 in retirement financial savings supplies $2,000 of revenue per yr,” famous the report’s authors. “At these ranges, Social Safety advantages are a vital a part of retirement revenue technique. Nevertheless, in response to the Social Safety Administration, ladies on common obtain 22% much less in Social Safety advantages pushed partly by pay gaps and part-time work.”

In a complement to its 2023 Retirement Survey & Insights Report referred to as Challenges Girls Face Saving for Retirement, Goldman Sachs Asset Administration checked out knowledge from 5,261 survey respondents throughout gender, age and job standing. Roughly 30% had retired on the time of the survey in July.

Along with shedding out on extra Social Safety revenue attributable to elements usually related to caregiving, ladies additionally are likely to retire sooner than deliberate and for extra sudden causes. Mixed with persisting revenue disparities, ladies are retiring with wherever from 24% (in response to Goldman) to 30% (in response to Tina Sanchez, head of nationwide retirement accounts for BlackRock) much less financial savings than the opposite 49.49% of the U.S. inhabitants.

“The latest market setting has been onerous on everybody, however it will be significant that we acknowledge that ladies, and particularly ladies of colour, have been hit the toughest,” Sanchez mentioned throughout a latest webinar, hosted by Vestwell, discussing ladies and retirement.

“We confer with it because the triple whammy,” she mentioned. “It’s the pay hole: on common, ladies nonetheless make lower than males; it’s about 83 cents on the greenback now. It’s the gaps in employment: ladies are disproportionately usually the caregivers spending outing of the workforce to look after family members. And it’s longevity: we all know ladies reside, on common, 5 years longer than males.”

Regardless of these challenges, the Goldman report discovered enhancements within the retirement outlook of working ladies, together with diminished stress in managing financial savings, elevated confidence and extra financial savings over the earlier yr.

The examine additionally delved into how gender-based variations might have an effect on funding priorities, preferences and market reactions.

Working ladies are nonetheless extra more likely to really feel they’re not saving sufficient for retirement; 43% really feel like they’re not on time, whereas a bit greater than a fifth suppose they’re forward. By comparability, 37% of working males really feel like they’re forward and three in ten need to catch up.

Nevertheless, ladies reported feeling extra comfy with their financial savings than they have been a yr earlier. Simply half mentioned managing retirement financial savings is tense, down from 63% the earlier yr and in contrast with 42% of their male counterparts.

“In fact, whereas it is very important see the optimistic improvement, it’s nonetheless vital that half of surveyed ladies report feeling stress managing their financial savings,” famous the report’s authors.

Girls additionally reported that the battle to steadiness a number of monetary objectives, dubbed the “monetary vortex” by GSAM, was having much less affect on their retirement plan in 2023 than within the earlier yr. Together with issues like bank card debt, saving for faculty, supporting members of the family, excessive month-to-month bills and sudden prices, ladies have been feeling higher throughout the board—a development that was reversed among the many males.

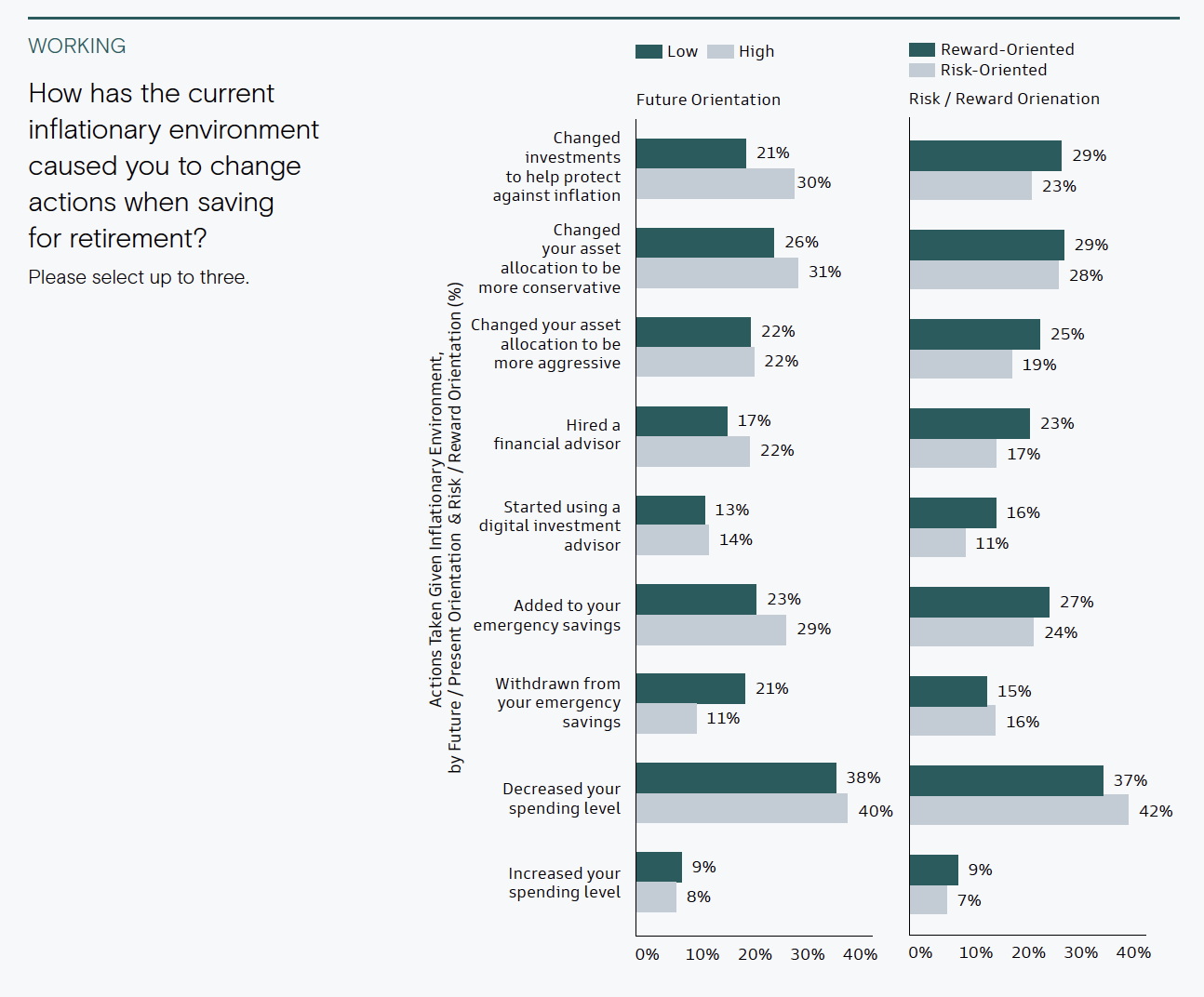

Based on the evaluation, this means ladies could also be extra oriented to the current and risk-averse whereas males are extra rewards-driven and targeted on the long run, traits that may have a major affect on funding decisions in several market environments.

Click on to enlarge

“This highlights the deeply private nature of economic objectives, and the usefulness of periodically accessing calculators and instruments to judge retirement readiness and improve confidence,” in response to GSAM Senior Retirement Strategist Chris Ceder. “Planning assumptions ought to be evaluated together with every particular person’s imaginative and prescient for retirement.”

Throughout the dialog with Vestwell, BlackRock’s Sanchez and Bonnie Treichel, founding father of Endeavor Retirement, highlighted the necessity for broader entry to schooling and monetary assets to assist ladies retire with extra safety. Sanchez advisable a mix of lively funding administration methods and goal date funds to assist overcome the behavioral problem by probably incomes higher returns.

“If ladies really feel like they’re under-saving, they need to undoubtedly be contemplating lively administration methods to assist make up for the financial savings shortfall by offering extra alpha,” Sanchez mentioned. “And with goal date funds, ladies’s investing conduct is tremendous encouraging. We see ladies make investments for the long run.”

Treichel and Tali Vaughn, regional VP of gross sales and consulting for retirement plan administrator EGPS, each steered personalized planning might assist handle a number of the distinctive challenges ladies face attributable to residing longer and bearing the brunt of household caregiving. They famous that proactive recommendation across the Safe 2.0 provisions pertaining to part-time, freelance and gig economic system employees, emergency financial savings packages and pupil mortgage debt could possibly be particularly helpful to ladies.

Finally, the GSAM analysis discovered roughly three-quarters of retired ladies and two-thirds of retired males reside on lower than 70% of their working revenue. A few third of girls are dissatisfied with this, in comparison with a fifth of males.

“We do want to speak about our funds extra and to vocalize our priorities,” mentioned Vestwell’s Kim Andranovich, citing a latest Forbes article by Jamie Hopkins. “The steadiness of wealth is shifting and because of residing longer, ladies would be the main wealth holders in all probability throughout the subsequent decade.

“So, it’s completely essential.”

[ad_2]