{kind=link}

[ad_1]

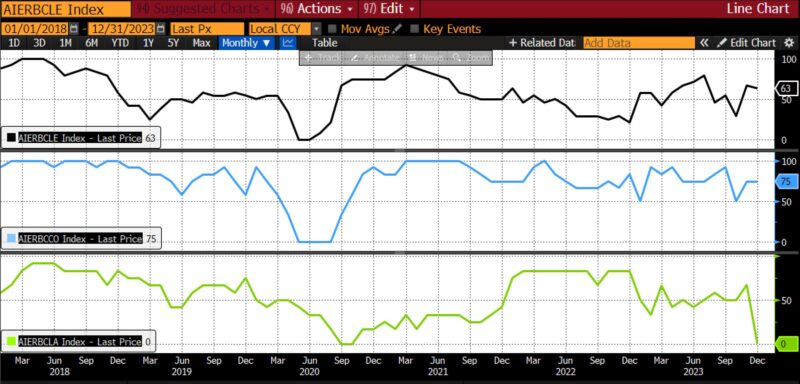

In December 2023, the AIER Enterprise Situations Month-to-month indices once more emphasised the unpredictable nature of financial knowledge within the post-COVID-19 interval. The Main Indicator fell barely from November 2023’s 67 to 63, whereas the Roughly Coincident Indicator remained at 75 from the earlier month. The Lagging Indicator, nonetheless, plummeted to zero for the primary time since late 2020.

Main Indicators (63)

From November 2023 to December 2023, seven of the twelve main indicators rose, 4 declined, and one was impartial.

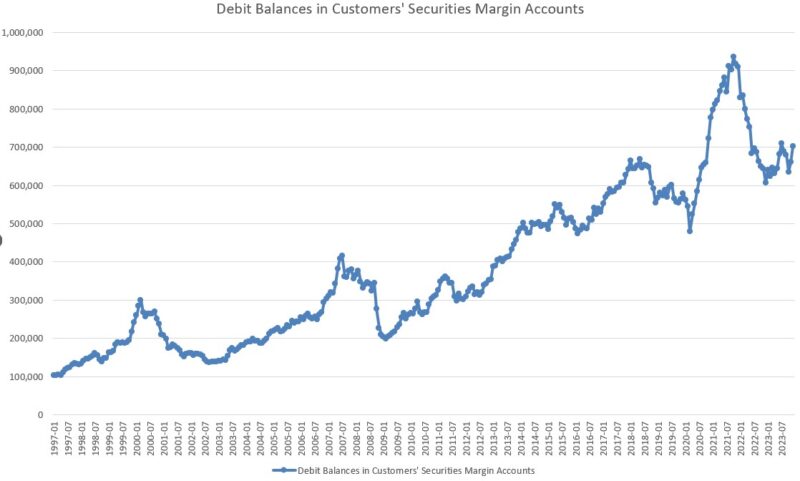

Rising had been College of Michigan Client Expectations Index (18.7 %), FINRA’s Debt Balances in Clients’ Securities Margin Accounts (6.0 %), US Preliminary Jobless Claims (5.6 %), Convention Board US Main Index Inventory Costs 500 Widespread Shares (5.0 %), Adjusted Retail and Meals Providers Gross sales Whole (0.6 %), Convention Board US Main Index Manufacturing New Orders Client Items and Supplies (0.1 %), Convention Board US Producers New Orders Nondefense Capital Good Ex Plane (0.1 %). The Stock/Gross sales Ratio: Whole Enterprise was unchanged from November to December. The US Common Weekly Hours All Staff Manufacturing (-0.3 %), US New Privately Owned Housing Models Began by Construction Whole (-4.3 %), United States Heavy Vehicles Gross sales (-4.6 %), and 1-to-10 12 months US Treasury unfold (-11.7 %) declined.

Roughly Coincident (75) and Lagging Indicators (0)

Throughout the Roughly Coincident Indicator, 4 constituents rose, one declined, and one was impartial. From November to December the three Convention Board metrics, Client Confidence Current State of affairs (7.8 %), Private Revenue Much less Switch Funds (0.2 %), and Coincident Manufacturing and Commerce Gross sales (0.2 %), in addition to US Staff on Nonfarm Payrolls Whole (0.2 %), expanded. US Industrial Manufacturing was unchanged and the US Labor Drive Participation Price fell by 0.5 %.

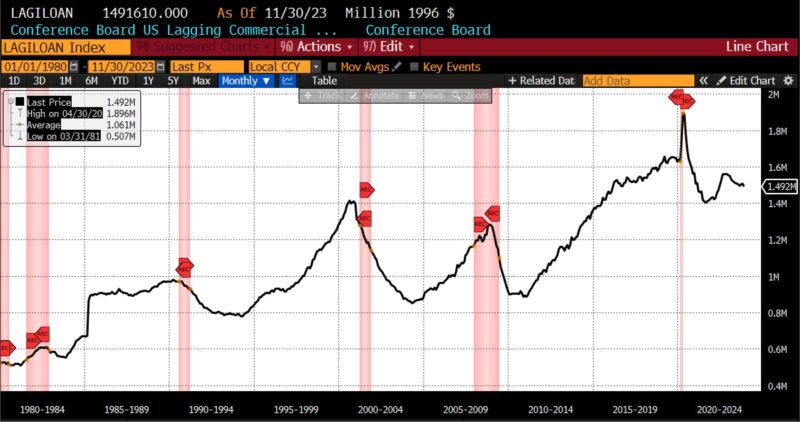

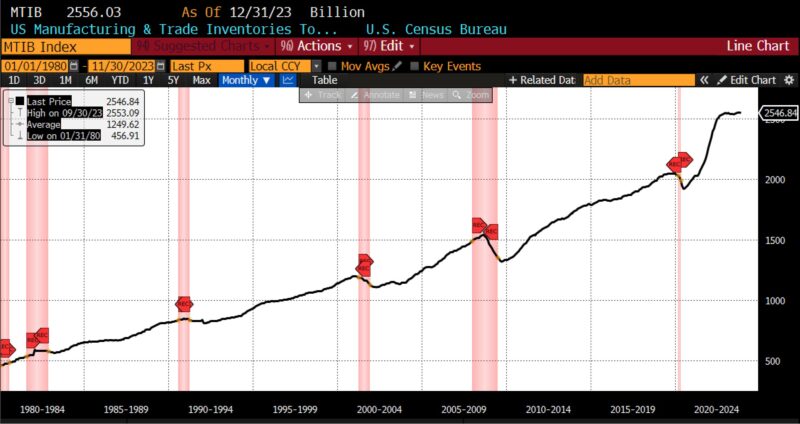

All six of the lagging indicators declined for the primary time since November 2020 between November and December 2023. The ISM Manufacturing Report on Enterprise Inventories (-0.1 %), Census Bureau US Non-public Constructions Spending Nonresidential (-0.2 %), US Business Paper Positioned High 30 Day Yield (-0.9 %), Convention Board US Lagging Business and Industrial Loans (-0.9 %), US CPI City Customers Much less Meals and Vitality 12 months over 12 months (-2.5 %), and the Convention Board US Lagging Common Period of Unemployment (-14.4 %) contracted within the final month of the 12 months.

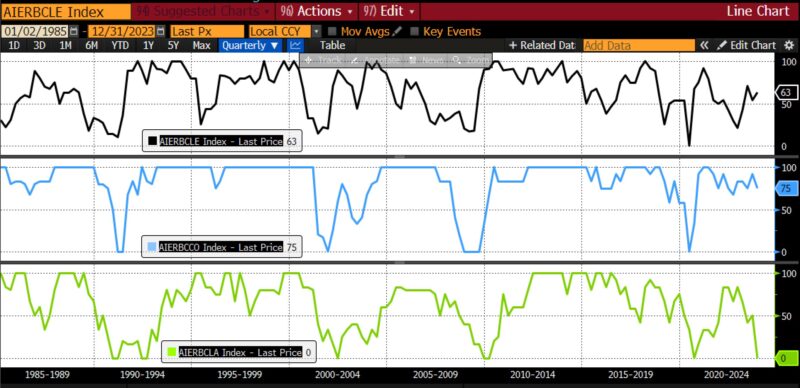

The unprecedented volatility noticed within the three Enterprise Situations Month-to-month indicators over current months exemplifies the distortions prevalent in financial knowledge broadly within the post-pandemic period. The sharp swings witnessed from one month to the subsequent spotlight the challenges in precisely capturing and assessing the underlying developments and dynamics of the present US economic system. Whereas such fluctuations elevate cheap considerations in regards to the reliability of financial knowledge, it’s important to acknowledge that they’re occurring inside a singular context formed by coverage responses to the pandemic and their subsequent results upon shopper conduct, manufacturing, commerce, enterprise funding, and past.

The financial situation depicted within the December 2024 Enterprise Situations Month-to-month is, as soon as once more, certainly one of contradictory indications. A considerably sturdy main indicator suggests future financial progress, indicating potential enchancment or enlargement within the close to future, pushed by elements like rising consumption, shopper confidence, and manufacturing orders. The sturdy coincident indicator portrays present financial situations as sturdy and steady, suggesting that, regardless of current slowdowns in sure areas, the US economic system is mostly performing effectively. All of that is at odds with the plummeting lagging indicator, which suggests current contraction owing to rising unemployment durations, falling inventories, declining personal nonresidential development, and different indicators of weak spot.

It might be untimely to formally reevaluate the connection inside the Enterprise Situations Month-to-month indicators and macroeconomic aggregates. Over time, nonetheless, it could change into essential to reassess our analytical frameworks and methodologies in an effort to make sure the accuracy and relevance of the financial knowledge utilized in capturing the progress of the US economic system.

Dialogue

Client spending, a stalwart contributor to financial enlargement, exhibited a blended trajectory within the fourth quarter, with progress in items consumption moderating whereas spending on companies accelerated. Mounting indicators of labor-market softening, nonetheless, characterised by bigger applicant swimming pools and easing wage pressures, solid doubt on the sustainability of shopper spending developments. Enterprise funding, notably in gear, remained lackluster, which suggests subdued company confidence in future progress prospects. The interaction of commerce dynamics and stock fluctuations add additional complexity to the financial narrative, with the trajectory of commerce companies and the unpredictability of stock changes posing extra forecasting challenges.

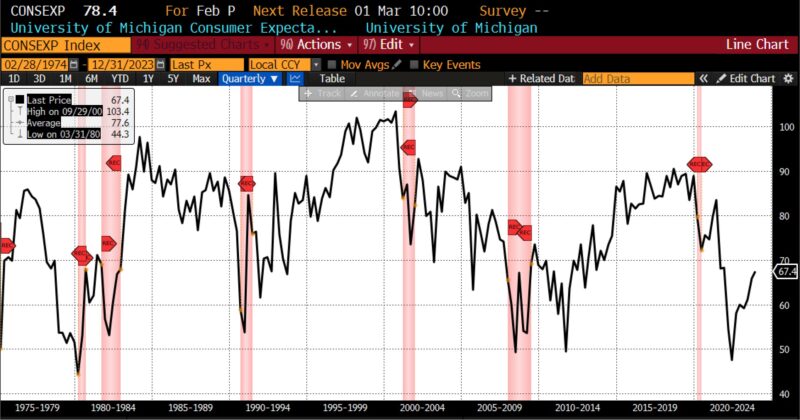

The financial panorama in early 2024 is equally characterised by a combination of constructive and regarding indicators. On one hand, shopper confidence rose in January, reflecting optimism fueled by expectations for decrease inflation and rate of interest cuts. The Convention Board’s shopper confidence index improved, pushed by bettering views on present financial situations and labor markets. There was, nonetheless, a notable drop in shopping for plans for houses, automobiles, and main home equipment, indicating a hesitancy amongst customers to spend following the vacation season. Moreover, current scorching inflation prints have tempered the development in sentiment, with rising inflation expectations doubtlessly overshadowing constructive financial information.

Retail gross sales in January skilled a larger-than-expected decline, signaling a pullback in shopper spending after a powerful spherical of vacation procuring in December. Whereas technical elements and opposed climate situations might have contributed to the weak spot, the general development suggests a less-vigorous begin to the 12 months for customers. Regardless of this, sturdy fundamentals, such because the strong January jobs report, have supplied some help to investor sentiment. However downward revisions to gross sales figures for December and November point out that shopper spending won’t have been as sturdy as beforehand reported, resulting in a extra cautious outlook for financial progress within the first quarter.

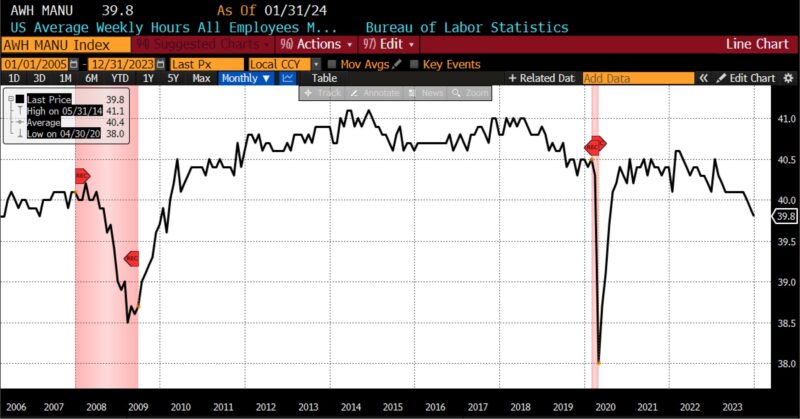

The January jobs report revealed surprisingly sturdy job positive factors, considerably decreasing the chance of a Fed fee lower in March. Revised benchmark knowledge confirmed that the labor market was weaker than beforehand thought from late 2022 via early 2023, however ran hotter than realized within the second half of 2023. Nonfarm payrolls elevated by 353,000 in January, increased than expectations, with a web upward revision of 126,000 for December and January mixed. Whereas common hourly earnings elevated and the U-3 unemployment fee held regular within the 3.7 % vary, common weekly hours labored declined, tempering the general constructive image.

Favorable information on the job market continued in early February 2024, boosting shopper sentiment in flip and reflecting the constructive affect of January’s blockbuster payroll positive factors. Considerations about escalating inflation, nonetheless, notably in gentle of current value will increase for fuel and different items, might dampen the development in sentiment. Inflation expectations have edged increased, elevating considerations in regards to the erosion of buying energy and dwelling requirements. As inflation stays a key challenge, notably within the lead-up to the November presidential elections, policymakers and market contributors will carefully monitor future financial knowledge releases to gauge the trajectory of inflation and its implications for the broader economic system.

The labor market image is cloudier than typically acknowledged at current. Three elements solid some doubt on the remarkably sturdy labor market knowledge of late.

First, abnormally low survey response charges in 2023 and January 2024 elevate questions in regards to the reliability of the information. Second, there are causes for questioning the accuracy of the birth-death mannequin and the potential undercounting of enterprise closures therein. Revisions to the Bureau of Labor Statistics’ Enterprise Beginning-Loss of life Mannequin contributed considerably to non-seasonally adjusted payroll figures, with increased contributions from Could to November. Up to date inhabitants controls have moreover decreased the estimated dimension of the civilian noninstitutional inhabitants, affecting the reported labor drive dimension. Third, the decline in common weekly hours labored, notably in cyclical industries, offset increased wages. That results in a relentless degree of weekly earnings from December to January, however adjusting for the decline in hours labored payrolls, would have declined by the equal of 485,000 full-time jobs in January 2024. So considerations about knowledge reliability and potential financial implications stay, heightening uncertainty surrounding future Fed coverage choices.

World financial headwinds, together with the outbreak of recessions within the United Kingdom and Japan alongside notable financial slowdowns in each China and Germany, solid an extra shadow over the outlook. The predictive energy of shopper sentiment has degraded over time, and rising inflation, bank card delinquencies, and a larger-than-expected drop in retail gross sales recommend underlying weaknesses.

Within the aftermath of the primary run of the fourth-quarter 2023 GDP report, which surpassed expectations, an air of cautious optimism has pervaded financial discourse within the media. Regardless of that consequence, considerations persist concerning potential downward revisions to GDP figures in gentle of tepid survey knowledge, a facet more and more acknowledged by officers. The GDP progress of three.3 % for the fourth quarter, outperforming estimates and led primarily by sturdy shopper spending, underscores a semblance of resilience within the economic system, albeit shadowed by apprehensions stemming from sluggish enterprise funding and unsure commerce dynamics.

Readings from regional Fed surveys, in the meantime, recommend that GDP prints might ultimately be revised downward. Regardless of the constructive GDP determine, which isn’t closely weighted by the Federal Reserve or the Nationwide Bureau of Financial Analysis, it stays potential {that a} recession is presently underway.

The NBER locations comparatively low weight on GDP in figuring out previous enterprise cycles, contemplating a spread of indicators and specializing in month-to-month chronology. Opposite to common perception, a recession doesn’t essentially require two consecutive quarters of GDP contraction, with equal weight positioned on Gross Home Revenue (GDI), which contracted within the 12 months via 3Q23. The NBER emphasizes economy-wide measures of financial exercise, giving comparatively little weight to actual GDP resulting from its quarterly measurement and susceptibility to revisions. Every financial downturn is exclusive, with some marked by important GDP contractions and others not, such because the delicate recession in 2001.

Traditionally, preliminary prints of actual GDP had been usually revised down later, suggesting potential downward revisions to current GDP prints, regardless of current power in arduous knowledge. Smooth knowledge point out room for warning, emphasizing the necessity to contemplate each arduous and gentle knowledge collectively. Whereas GDP progress in 4Q suggests resilience, a holistic view suggests warning and the opportunity of a gentle recession just like that seen in 2001.

The anticipated Fed fee cuts, if realized, are prone to happen a lot later within the 12 months resulting from nagging inflationary pressures and glimpses of financial resilience that the Federal Reserve can’t disregard. Amidst the prevailing financial panorama, characterised by a confluence of divergent alerts throughout numerous indicators, prudence dictates our vigilant and goal monitoring of forthcoming coverage deliberations and statistical releases. Given the intricacies inherent in current (and maybe distorted) assessments of the US labor market, shopper sentiment, and analogous datasets ostensibly portraying favorable contours, all of which juxtaposed in opposition to the contemporaneous downturns afflicting a number of main world economies, a forecast of financial contraction continues to pervades our outlook for 2024.

LEADING INDICATORS

ROUGHLY COINCIDENT INDICATORS

LAGGING INDICATORS

CAPITAL MARKET PERFORMANCE

Peter C. Earle

Peter C. Earle, Ph.D, is a Senior Analysis Fellow who joined AIER in 2018. He holds a Ph.D in Economics from l’Universite d’Angers, an MA in Utilized Economics from American College, an MBA (Finance), and a BS in Engineering from the USA Army Academy at West Level.

Previous to becoming a member of AIER, Dr. Earle spent over 20 years as a dealer and analyst at quite a lot of securities companies and hedge funds within the New York metropolitan space in addition to partaking in in depth consulting inside the cryptocurrency and gaming sectors. His analysis focuses on monetary markets, financial coverage, macroeconomic forecasting, and issues in financial measurement. He has been quoted by the Wall Avenue Journal, the Monetary Instances, Barron’s, Bloomberg, Reuters, CNBC, Grant’s Curiosity Price Observer, NPR, and in quite a few different media shops and publications.

[ad_2]