{kind=link}

[ad_1]

By Sabrina Corlette and Rachel Schwab

January 16, 2024 Replace: H.R. 824 was superior by the U.S. Home of Representatives’ Committee on Schooling & the Workforce in June 2023. Extra not too long ago, advocates for the measure are pushing to connect the proposal to an upcoming appropriations invoice as a “coverage rider.”

On Tuesday, June 6, the U.S. Home of Representatives’ Schooling & Workforce Committee will think about a invoice, H.R. 824, that will encourage the proliferation of telehealth protection as a standalone worker profit. Proponents of this laws—a lot of whom stand to revenue from the sale of those merchandise—argue that it might give employers and staff extra inexpensive choices. Nonetheless, underneath the proposed laws, standalone telehealth merchandise could be nearly completely exempt from regulatory oversight, posing vital dangers to shoppers who may face misleading advertising and marketing of those preparations as an alternative to complete protection.

Background

The supply of well being care companies through telehealth modalities expanded dramatically in the course of the COVID-19 pandemic. Though charges of telehealth use have moderated considerably for the reason that peak of the general public well being emergency (PHE), they continue to be properly above pre-pandemic ranges.

Federal and state policymakers inspired the usage of telehealth via a number of PHE-related coverage adjustments. For instance, early within the pandemic many staff had been staying residence and going through reductions in work hours, typically rendering them ineligible for medical insurance via their employer. The Biden administration sought to assist fill gaps in entry to well being companies by issuing steerage quickly suspending the applying of group well being plan guidelines to standalone telehealth advantages when provided to staff ineligible for the employer’s group well being plan. This coverage was solely relevant in the course of the PHE.

Ordinarily, any employer-sponsored plan protecting medical companies for workers and dependents is topic to Inexpensive Care Act (ACA) and different federal requirements for group well being plans. Thus, absent the PHE-related suspension of the principles, a standalone telehealth profit would wish to adjust to, for instance, mandates to cowl preventive companies with out cost-sharing, the ban on annual greenback limits on advantages, psychological well being parity necessities, and the annual cap on enrollees’ out-of-pocket spending. Nonetheless, H.R. 824 would prolong and develop on the COVID-era coverage by permitting employers to supply telehealth as an “excepted profit” to all staff—not simply these ineligible for the employer’s main medical plan.

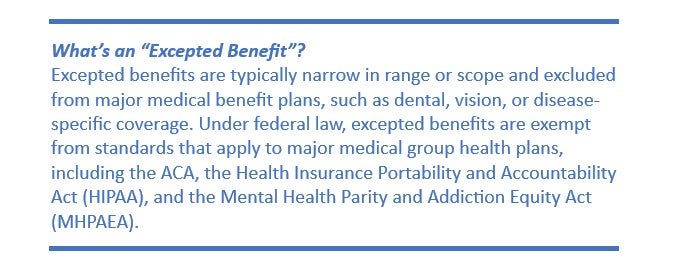

Excepted advantages may be enticing to employers as a result of they don’t seem to be topic to most federal requirements that apply to group medical insurance, together with shopper protections underneath the ACA, HIPAA, and MHPAEA. Dental and imaginative and prescient insurance coverage are among the many most typical kinds of excepted advantages, and lots of distributors notoriously present inadequate protection. Fastened indemnity insurance coverage, one other excepted profit, is usually marketed to shoppers as complete insurance coverage protection regardless of protecting solely a fraction of enrollees’ precise incurred prices.

Telehealth as an Excepted Profit Would Scale back, Not Improve, High quality Protection

Nothing underneath federal legislation prevents employers from protecting telehealth for workers, both by reimbursing brick-and-mortar suppliers for providing video and audio consultations or by contracting with telehealth distributors similar to Teladoc. In reality, the overwhelming majority of huge corporations (96%) and small corporations (87%) presently cowl some type of telehealth companies. Designating telehealth protection as an excepted profit is thus unlikely to develop staff’ entry to those companies. As a substitute, the proposal poses a number of issues for staff and their households.

First, separating telehealth companies from staff’ well being advantages fractures care supply and frustrates the coordination of take care of sufferers, who will possible need to see a distinct supplier than their typical supply of care to entry coated telehealth advantages. It may additionally topic enrollees to sudden extra value sharing, similar to two deductibles, and trigger confusion about what companies are coated and by whom.

Second, designating telehealth protection as an excepted profit places shoppers in danger by encouraging the advertising and marketing of merchandise which are exempt from important federal protections. A telehealth insurer may cost the next premium to somebody with a pre-existing situation and refuse to cowl sure therapies, or alternatively, the insurer may deny them protection altogether. Excepted advantages are additionally exempt from psychological well being parity guidelines, can place annual or lifetime caps on advantages, and may impose value sharing for preventive companies, which can deter enrollees from getting the care that they want.

Third, excepted advantages have a troubled historical past, with distributors typically deceptively advertising and marketing these merchandise as a substitute for complete medical insurance. Brokers typically bundle excepted profit merchandise collectively, in order that they seem on the floor like a complete coverage, with out clearly speaking that these preparations don’t adjust to key shopper protections and go away enrollees at vital monetary threat.

Fourth, a standalone telehealth profit that an worker can select in lieu of a significant medical plan may disproportionately hurt decrease revenue staff. These staff could also be inspired to enroll within the telehealth profit, probably packaged with one other excepted profit similar to a set indemnity coverage, as an inexpensive various to their employer’s main medical plan. However staff could not notice that these merchandise should not topic to the identical shopper protections as the excellent group plan and don’t present actual monetary safety in the event that they get sick or injured.

Conclusion

Expanded entry to telehealth companies has been a boon for sufferers, significantly these residing in rural areas and people who lack transportation choices or flexibility at work. Employers, to their credit score, embraced telehealth in the course of the pandemic and haven’t seemed again. A whopping 76% of employers with 50 or extra staff predict that the usage of telehealth of their well being plans will both keep the identical or enhance, and a considerable majority of each massive and small corporations consider that telehealth can be very or considerably vital to offering enrollees with entry to a variety of well being care companies, significantly for behavioral well being.

Thus, whereas H.R. 824 is touted as increasing telehealth protection, its predominant impact would as an alternative be to silo medical companies delivered via video and audio modalities from the remainder of the care supply system, enhance the potential for scams and misleading advertising and marketing, and expose staff and their dependents to well being and monetary threat by rolling again important shopper protections.

[ad_2]