{kind=link}

[ad_1]

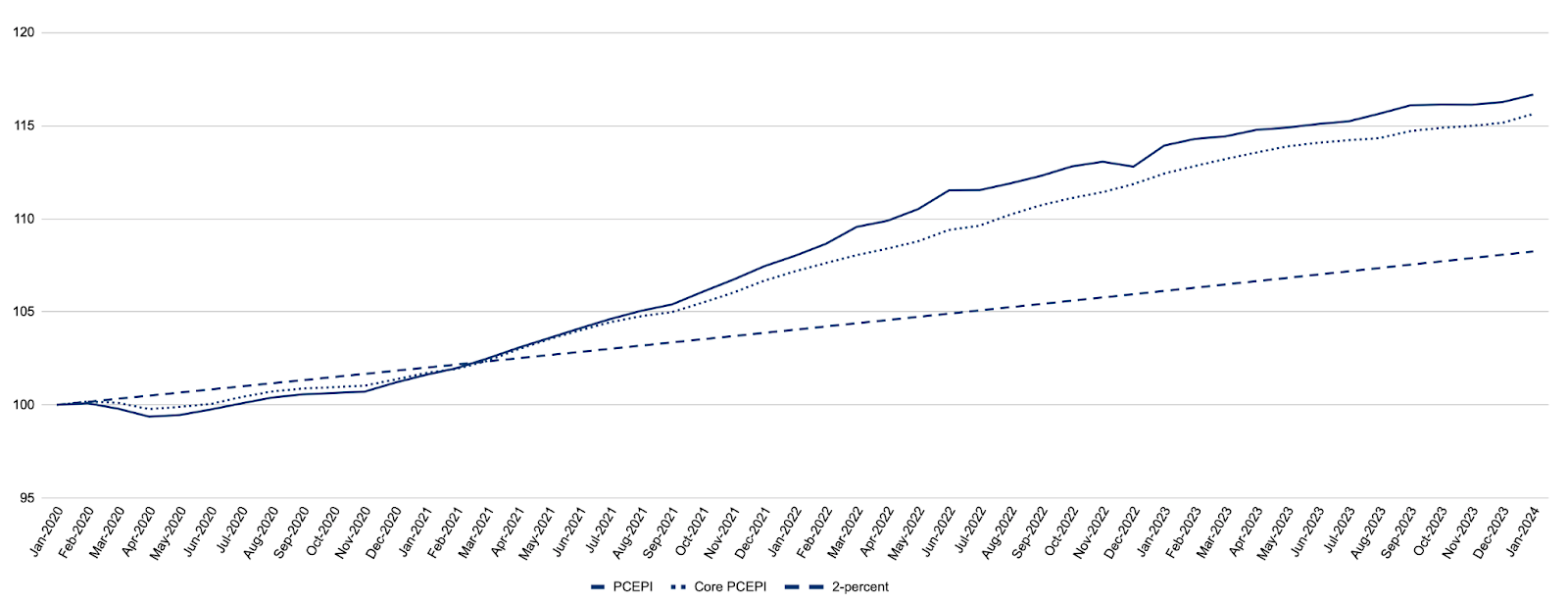

Inflation picked up in January, based on the newest information from the Bureau of Financial Evaluation (BEA). The Private Consumption Expenditures Worth Index (PCEPI), which is the Federal Reserve’s most popular measure of inflation, grew at a constantly compounding annual charge of 4.1 p.c within the first month of the 12 months. The PCEPI has grown at an annualized charge of 1.8 p.c over the past three months and a couple of.5 p.c over the past six months. Costs at this time are 8.4 proportion factors larger than they’d have been had they grown at an annualized charge of two.0 p.c since January 2020.

Determine 1. Headline and Core Private Consumption Expenditures Worth Index with 2-percent Development, January 2020 – January 2024

Core inflation, which excludes risky meals and vitality costs, additionally elevated. Core PCEPI grew at a constantly compounding annual charge of 5.0 p.c in January. It has grown at an annualized charge of two.6 p.c over the past three months and a couple of.5 p.c over the past six months.

There isn’t a denying that measured inflation elevated significantly in January. The query is whether or not it means inflation will doubtless be larger than beforehand anticipated within the months forward. There are no less than two causes to suppose the January uptick is only a blip, and will likely be adopted by a lot smaller value will increase within the months forward.

First, the rise in inflation was partly resulting from a surge in imputed costs. Imputed costs are quantified alternative prices. What didn’t occur just isn’t straight noticed and, therefore, should be estimated. Contemplate owner-occupied housing. Whereas the value a renter pays his landlord for housing providers will be measured, the value an proprietor implicitly pays herself to dwell in her personal home can’t. Economists on the BEA should estimate the value of owner-occupied housing with a purpose to estimate the final degree of costs. Equally, some providers offered by monetary and nonprofit establishments serving households are usually not straight observable.

Though economists on the BEA certainly do their finest to precisely estimate imputed costs, there is no such thing as a assure that they get it proper. Correspondingly, a point of skepticism is warranted when imputed costs diverge from market costs, as they did in January. Market-based PCE, which is a supplemental measure provided by the BEA, is predicated on family expenditures for which there are observable costs. It excludes most imputed transactions. The market-based PCE value index grew at a constantly compounding annual charge of three.1 p.c in January. It has grown at an annualized charge of 1.3 p.c over the past three months and a couple of.4 p.c over the past six months. Possibly imputed costs are rising extra quickly than observable costs, as estimates counsel. Or, perhaps, these estimates are overstating the rise in imputed costs.

Second, the same old seasonal adjustment for January could also be inadequate for January 2024. Many costs reset in January, as contracts are renewed in the beginning of the 12 months. To forestall a spike in CPI inflation every January, the BEA adjusts the info to account for the standard January value enhance. This process basically apportions a few of the enhance in January costs to different months, as if the costs had grown step by step from one month to the subsequent as a substitute of out of the blue every January.

Seasonally-adjusting value degree information works fairly properly in regular instances. However, in uncommon circumstances, the seasonal adjustment could over- or under-state precise value modifications. When costs are rising sooner than ordinary, the seasonal adjustment — which accounts for the same old enhance in costs —won’t apportion sufficient of the January value will increase to different months. Consequently, the seasonally adjusted value degree will are inclined to overstate inflation in January (and understate inflation in different months). Robin Brooks not too long ago made this level within the context of the Shopper Worth Index (CPI), however the argument applies to the PCEPI as properly.

Brooks describes the January 2024 uptick in costs as “an echo of final 12 months’s start-of-year value resets that made inflation in early 2023 look a lot worse than it actually was.” In January 2023, the PCEPI grew at a constantly compounding annual charge of 6.7 p.c. It had grown at an annualized charge of three.5 p.c over the prior three months and would develop at an annualized charge of three.0 p.c over the next three months. In hindsight, January 2023 was an outlier. January 2024 seems prone to be an outlier, as properly.

Following the January inflation information, most commentators fall into one in all two classes: these involved as a result of they consider we’re experiencing a resurgence of inflation, and people unconcerned as a result of they consider the January uptick in inflation is only a blip. In distinction, I consider there’s trigger for concern although the January uptick will doubtless turn into only a blip. Why? As a result of it should doubtless lead Fed officers to maintain financial coverage tighter for longer.

In a latest discuss, Fed Governor Christopher Waller mentioned the January inflation information strengthened his “view that we have to confirm that the progress on inflation we noticed within the final half of 2023 will proceed.” He mentioned “there is no such thing as a rush to start slicing rates of interest to normalize financial coverage.”

Waller rightly acknowledges that the January enhance in inflation “could have been pushed by some odd seasonal elements or outsized will increase in housing prices.” However he errs in considering “the power of output and employment progress signifies that there is no such thing as a nice urgency in easing coverage.” The accessible information is historic and financial coverage acts with a lag. To keep away from overcorrecting, and pushing the economic system right into a recession, the Fed should ease financial coverage earlier than the info clearly demonstrates inflation is again all the way down to 2 p.c.

The Fed didn’t tighten coverage swiftly as inflation picked up within the second half of 2021. Consequently, costs rose a lot larger than they need to have. It has equally didn’t ease coverage as inflation returned to its 2-percent goal in 2023. The Fed needs to be wanting forward and adjusting financial coverage in gentle of its forecasts. As a substitute, its eyes are fastened on the rearview mirror. Let’s hope the Fed adjusts its trajectory earlier than it’s too late.

William J. Luther

William J. Luther is the Director of AIER’s Sound Cash Mission and an Affiliate Professor of Economics at Florida Atlantic College. His analysis focuses totally on questions of forex acceptance. He has revealed articles in main scholarly journals, together with Journal of Financial Conduct & Group, Financial Inquiry, Journal of Institutional Economics, Public Selection, and Quarterly Evaluation of Economics and Finance. His common writings have appeared in The Economist, Forbes, and U.S. Information & World Report. His work has been featured by main media retailers, together with NPR, Wall Road Journal, The Guardian, TIME Journal, Nationwide Evaluation, Fox Nation, and VICE Information. Luther earned his M.A. and Ph.D. in Economics at George Mason College and his B.A. in Economics at Capital College. He was an AIER Summer time Fellowship Program participant in 2010 and 2011.

[ad_2]