{kind=link}

[ad_1]

As we go to press, the S&P 500 is at its highest degree in historical past: 5137. It set a file by passing 5000 for the primary time on February 12, then one other file excessive of 5100 two weeks later.

In actuality, after all, the S&P just isn’t rocketing upward. The S&P 7-to-10 is, with the opposite 490-493 shares as an afterthought. The highest 10 shares contributed 93% of the index’s 2023 features. Goldman Sachs declares that the “S&P 500 index is extra concentrated than it has ever been,” whereas Amundi, Europe’s largest asset supervisor and one of many world’s high six, claims it’s merely “at its highest degree in over 30 years.” People making an attempt to ease anxiousness about that time to the truth that the market has been extra concentrated earlier than: within the mid-60s, the highest 10 accounted for 40% of the market (which then … uhh, crashed), and on the finish of the 90s they hit 25% of the market (which then … uhh, crashed).

Torsten Sløk, chief economist at Apollo International Administration, a US non-public fairness agency with over $500 billion in property beneath administration, appears to suppose that’s a foul signal. “The highest 10 firms within the S&P 500 immediately are extra overvalued than the highest 10 firms have been throughout the tech bubble within the mid-Nineties” (Every day Spark, 2/25/2024). The Shiller CAPE ratio, which seems on the value of shares relative to long-term earnings, sits at its third-highest degree in 150 years.

For the previous 15 years or so, that hasn’t been trigger for alarm. The interval we describe as The Nice Distortion noticed shares routinely achieve traditionally unprecedented valuations and undergo a collection of comparatively cold crashes: the market would crash by a 3rd, then bounce promptly again. The Covid Crash took the market down 34% … and lasted simply over one month. These fast recoveries have been pushed by TINA: with nominal rates of interest close to zero, actual rates of interest beneath zero, and an infinitely ingenious Federal Reserve prepared with ever extra revolutionary rescue schemes, money was trash, bonds have been losers, and There Is No Different to the inventory market.

The Callan Desk of Periodic Funding Returns affords one solution to seize the impact of The Nice Distortion. Listed below are the top-performing asset lessons every year previous to The Nice Distortion.

And the most effective asset lessons within the years since. (Callan has completed some relabeling, so index names within the previous chart are changed by asset class names within the new one.)

Earlier than The Nice Distortion, US massive caps gained as soon as in 12 years (an 8% win fee, 1998-2009). Afterward, they gained 4 instances (a 29% win fee, 2010-present). US equities gained 3 times (twice, small worth) in 13 years (23% win fee, with two wins by small worth) versus eight instances in 14 years (a 57% win fee). Regardless of frequent crashes, US equities have been two to 4 instances likelier to “win” than beforehand.

Many argue (possible, hope) that The Nice Distortion is ending. Rates of interest are within the neighborhood of their 100-year common, and the Fed appears disinclined to reward the markets with untimely reductions in them. That implies that money affords an actual return (one-month Treasuries are providing a 5.5% yield in early March 2024), and bonds have the potential to problem shares for buyers’ consideration.

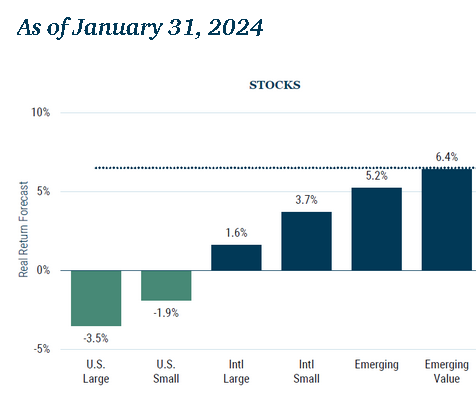

Should you consider that the markets are normalizing, then you definitely may attend to the implications of GMO’s latest asset class forecasts.

GMO, a Boston-based institutional funding agency based by Jeremy Grantham, has launched its newest “if solely the world have been regular” projections for five–7-year asset class efficiency. It’s a month-to-month train, maybe a public service, that garners some small discover within the investing neighborhood. The latest forecast, like most of its quick predecessors, is profoundly destructive towards US fairness investments and comparatively optimistic towards investments in rising markets.

The projections, they aver, are “based mostly upon the cheap beliefs of GMO” and embody a projected inflation fee of two.3%. That implies that the “actual” returns projected above are projected asset class returns minus 2.3%.

Two notes:

-

Earlier than The Nice Distortion, when the US Fed discovered an almost-infinite array of how to prop up the market, GMO’s forecasts have been “stunningly correct.” The correlation between GMO and actuality was 0.94%, with GMO tending to be only a bit optimistic of their predictions. Mr. Grantham’s 10-year projection, from the start of the century by way of 2009, was “nearly precisely proper.”

That “precisely rightness” is mirrored within the efficiency of GMO’s methods within the years earlier than the Fed rushed to the rescue. Utilizing the fund screener at MFO Premium, I pulled the relative return rankings for all GMO methods. MFO Premium, MFO’s accomplice web site, affords probably the most complete set of danger and efficiency knowledge accessible to retail buyers and smaller RIAs. On this case, we requested, “What number of of GMO’s methods had high 20% returns every year within the early 2000s?” With eight methods, on common, 1.6 of them would land within the high tier. GMO crushed that threshold nearly yearly. For the sake of brevity, we’ll present solely the even-numbered years:

-

- 2000: 4 of 8 funds had high 20% returns

- 2002: 6 of 8 did

- 2004: 4 of 9 (they added a brand new EM debt fund)

- 2006: 1 of12 did (most have been common to above-average that 12 months)

- 2008: 6 of 13 did

On the whole, GMO was very proper, fairly often.

-

-

Since The Nice Distortion, “the precise efficiency of the foremost asset lessons over the previous decade has been nearly completely inverse to GMO’s predictions” (“The Perils of Lengthy-Time period Forecasting – GMO Version,” Monetary Instances, 8/17/2023). US large-cap shares, the property most benefited by the Fed’s largesse, “smashed every part.”

As soon as the Fed blew up the connection between danger and reward, GMO’s projections turned contrarian indicators: every part that was low cost acquired cheaper, and every part that was costly acquired extra so.

It occurs. Talking with Pensions & Investments, GMO’s founder Jeremy Grantham defined:

My estimate is one thing like 85% of the time the market is roughly cheap, roughly environment friendly. Shut sufficient. After which 15% of the time, it’s not. That divides one thing like 11% or 12% loopy optimism and three% or 4% loopy pessimism. And that appears to be the mannequin. (“Jeremy Grantham’s funding bubble features prolong to his enterprise capital part,” PIOonline, 10/31/2023)

Different main buyers – not the Krypto Children, definitely, however of us who’ve managed by way of a number of storms, appear to level in the identical common route as GMO.

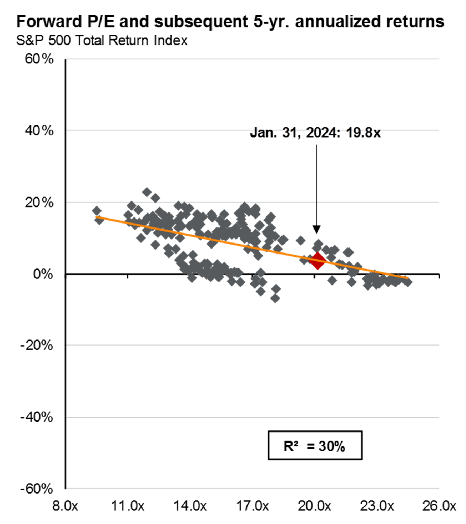

J.P. Morgan is just barely extra optimistic concerning the subsequent 5 years. They’ve plotted the five-year returns of the S&P based mostly on how excessive valuations have been firstly of the interval.

I might learn that as “5% earlier than inflation” as their expectation (Information to the Markets, Q1/2024).

The fascinating Asset Allocation Interactive instrument, printed by Analysis Associates, affords two projections for the 10-year returns on the US inventory market. If valuations matter, they count on actual returns of 1.5% per 12 months for a decade with volatility of 15.5%. If, nevertheless, valuations should not factored in, and we glance solely at dividends and progress, then returns soar… to 4% per 12 months. In distinction, returns on EM fairness are projected at 7.5% (valuations matter) or 6.8% (solely yield and progress issues).

The Implication

The top of The Nice Distortion doesn’t imply that shares are about to crash. It would imply that the securities that benefited probably the most and the longest from the period of free cash and assured Fed safety, US mega-cap progress shares, have misplaced their grip. Different property, not deeply undervalued relative to US massive caps, is perhaps anticipated to outperform with some consistency.

What to do about it?

There aren’t any ensures, which is the argument for diversification. As a result of 15 years is an eternity in investing, it’s an idea little-valued by many.

Take into account an equal-weight S&P 500 index. These funds place an equal quantity in every of the index’s 500 shares. The flagship is Invesco S&P 500 Equal Weight ETF (RSP), which expenses 0.20% and has outperformed the S&P 500.

Take into account a fundamental-weight S&P 500 index. These are funds that weight the S&P 500 shares based mostly on the efficiency traits of the underlying company, not their shares’ recognition. The 2 Nice Owl funds there are Schwab Basic US Giant Firm Index (SFLNX) and Invesco S&P 500 Income ETF (RWL).

Take into account an actively managed multi-cap fund. These are funds whose managers make investments throughout the dimensions spectrum, generally tilting towards bigger shares and generally towards smaller ones. Two Nice Owl funds to think about are Prospector Capital Appreciation (PCAFX) and Smead Worth (SMVLX).

Take into account a versatile portfolio fund. These are funds whose managers have the liberty to maneuver towards what they understand because the market’s most tasty choices at any given level. In contrast to the funds above, they’re usually extra risk-conscious and oriented towards absolute returns (that’s, avoiding destructive years). Two Nice Owl funds to think about are FPA Crescent (FPACX, the most important single holding in Snowball’s portfolio) and Buffalo Versatile Revenue (previously Buffalo Balanced, BUFBX).

Take into account including small worldwide shares. No funds on this realm earn a Nice Owl designation. Instead of that, we recognized funds with a mix of the best Sharpe ratios – the usual measure of risk-adjusted returns – and Martin ratios – a measure that strongly weighs draw back efficiency. Three distinguished funds by these measures are Constancy Worldwide Small Cap (FISMX), Driehaus Worldwide Small Cap Progress (DRIOX), and Pear Tree Polaris Overseas Worth Small Cap.

Take into account including rising markets shares. Lots of our most well-liked EM funds, Seafarer Abroad Progress & Revenue and Seafarer Abroad Worth as examples, don’t but have 15-year data. The 2 most distinguished funds which have crossed that threshold are each passive funds: SPDR S&P Rising Markets Small Cap ETF (EWX) and PIMCO RAE PLUS EMG (PEFFX). The PIMCO fund makes use of a Analysis Associates index which has a definite worth tilt.

Efficiency comparability, 15 years (by way of 01/2024)

| APR | Return vs friends | Sharpe ratio | US massive cap publicity | Nice Owl? | Morningstar | |

| Invesco S&P 500 Equal Weight | 16.0 | +2.7 | 0.89 | 35 | Sure | 5 stars |

| Schwab Basic US Giant Co Index | 16.4 | +3.2 | 0.95 | 68 | Sure | 5 stars |

| Invesco S&P 500 Income ETF | 115.8 | +2.6 | 0.95 | 67 | Sure | 5 stars |

| Prospector Capital App | 11.0 | -2.2 | 0.81 | 38 | Sure | 5 stars |

| Smead Worth | 16.6 | +3.4 | 0.92 | 46 | Sure | 5 stars |

| FPA Crescent | 10.2 | +1.7 | 0.83 | 31 | Sure | 4 stars, Gold |

| Buffalo Versatile Revenue | 10.9 | +2.3 | 0.81 | 72 | Sure | Three stars, Gold |

| Constancy Worldwide Small Cap | 11.7 | +1.6 | 0.65 | – | No | 5 stars, Impartial |

| Driehaus Worldwide Small Progress | 12.2 | +1.7 | 0.66 | – | No | 5 stars, Bronze |

| Pear Tree Polaris Overseas Worth Small Cap | 12.0 | +0.9 | 0.93 | – | No | 4 stars, Bronze |

| SPDR S&P Rising Markets Small Cap ETF | 9.5 | +1.8 | 0.44 | – | Sure | 5 stars, Bronze |

| PIMCO RAE PLUS EMG | 11.5 | +3.8% | 0.47 | – | Sure | 4 stars, Bronze |

| US Whole Inventory Market Index | 15.7 | 0.96 | 71 | No |

Supply: MFO Premium knowledge screener. Observe: Lipper peer teams differ from fund to fund, so the annual return in comparison with friends might sound inconsistent from one row to the subsequent. That’s merely completely different peer teams throughout the identical broad theme (worldwide smaller firms or multi-cap funds).

The Backside Line

Should you consider that The Nice Distortion has ended, that inflation is actual, and that rates of interest won’t return to the zero-to-negative vary they occupied since 2008, then you may additionally wish to take GMO’s projection extra critically.

That means relying much less on methods that depend upon Fed largesse and market mania and extra on methods which have labored nicely even whereas out of favor. We shut with Mr. Grantham:

I might say that monetary markets are very inefficient, and able to extremes of being utterly dysfunctional. (Stephanie Dahle, “Get Briefed: Jeremy Grantham,” Forbes.com, 1/26/2009)

[ad_2]