{kind=link}

[ad_1]

Within the aftermath of the COVID-19 pandemic, the U.S. financial system skilled a swift restoration accompanied by a pointy rise in inflation. Inflation has been progressively declining since 2022 and not using a notable slowdown within the labor market. Nonetheless, inflation stays above the Federal Reserve’s 2 p.c goal and the trail of the so-called ultimate mile stays unsure, as emphasised by Chair Powell throughout his press convention in January. On this submit, we look at the unemployment-inflation trade-off over the previous few years by the lens of a New Keynesian Phillips curve, primarily based on our latest paper. We additionally present model-based forecasts for 2024 and 2025 beneath varied labor market situations.

Our Mannequin

In our framework (primarily based on earlier work), inflation is pushed by transient provide elements, inflation expectations, and labor market situations. Whereas there are alternative routes to measure labor market situations, we use the unemployment hole because the constructing block for characterizing labor market situations. The unemployment hole is outlined as:

the place ![]() is the realized unemployment charge and

is the realized unemployment charge and ![]() is the pure charge of unemployment outlined in Milton Friedman’s 1968 Presidential Deal with to the American Financial Affiliation. The pure charge of unemployment is a time-varying unobserved variable that displays, amongst different issues, secular tendencies (the getting older of the newborn boomers, for instance), modifications within the mismatch between vacant jobs and obtainable employees, or shifts in willingness to work (maybe as a consequence of altering attitudes about work-life stability).

is the pure charge of unemployment outlined in Milton Friedman’s 1968 Presidential Deal with to the American Financial Affiliation. The pure charge of unemployment is a time-varying unobserved variable that displays, amongst different issues, secular tendencies (the getting older of the newborn boomers, for instance), modifications within the mismatch between vacant jobs and obtainable employees, or shifts in willingness to work (maybe as a consequence of altering attitudes about work-life stability).

The New Keynesian Phillips curve relates inflation to the present unemployment hole ( ) and to expectations about future unemployment gaps (

) and to expectations about future unemployment gaps ( and so forth) and offers us a helpful means of decomposing present inflation,

and so forth) and offers us a helpful means of decomposing present inflation,  , as:

, as:

the place ![]() is the slope of the Phillips curve and

is the slope of the Phillips curve and  is the long-run pattern in inflation. Be aware that each the present and anticipated future unemployment gaps have an effect on inflation by

is the long-run pattern in inflation. Be aware that each the present and anticipated future unemployment gaps have an effect on inflation by ![]() , a defining characteristic of the New Keynesian Phillips curve. This equation tells us that inflation is comprised of a elementary part (“underlying inflation”) and a part reflecting provide shocks (akin to international supply-chain disruptions).

, a defining characteristic of the New Keynesian Phillips curve. This equation tells us that inflation is comprised of a elementary part (“underlying inflation”) and a part reflecting provide shocks (akin to international supply-chain disruptions).

As a result of the pure charge of unemployment isn’t noticed, we have now to estimate it. In our paper, we use a wealth of labor market and inflation knowledge to deduce the evolution of ![]() and of financial brokers’ expectations in regards to the future path of the unemployment hole. We discover a notable improve in

and of financial brokers’ expectations in regards to the future path of the unemployment hole. We discover a notable improve in ![]() from round 5 p.c earlier than the pandemic to six.6 p.c on the finish of 2023. We relate this rise to a declining willingness to work, a record-high quits charge (sometimes called the Nice Resignation), rising reservation wages, and difficulties in filling vacant jobs, all of which have solely just lately began to reasonable.

from round 5 p.c earlier than the pandemic to six.6 p.c on the finish of 2023. We relate this rise to a declining willingness to work, a record-high quits charge (sometimes called the Nice Resignation), rising reservation wages, and difficulties in filling vacant jobs, all of which have solely just lately began to reasonable.

Analyzing Latest Disinflation

This excessive stage of the pure charge relative to the a lot decrease unemployment charge (which has remained beneath 4 p.c because the finish of 2021) would have urged upward inflationary pressures.

So why has inflation been on a declining pattern since 2022 amid such a decent labor market? There are two causes: First, international provide chain disruptions, which had put upward stress on inflation beginning in 2021, have abated; second, what issues for inflation is much less in regards to the present unemployment hole and extra in regards to the anticipated path of future gaps going ahead.

To confront the info with the mannequin, we will return to the second quarter of 2022 (roughly when inflation peaked) and see what the mannequin anticipated. Importantly, once we carry out this train we don’t give the mannequin any info past what was obtainable at the moment.

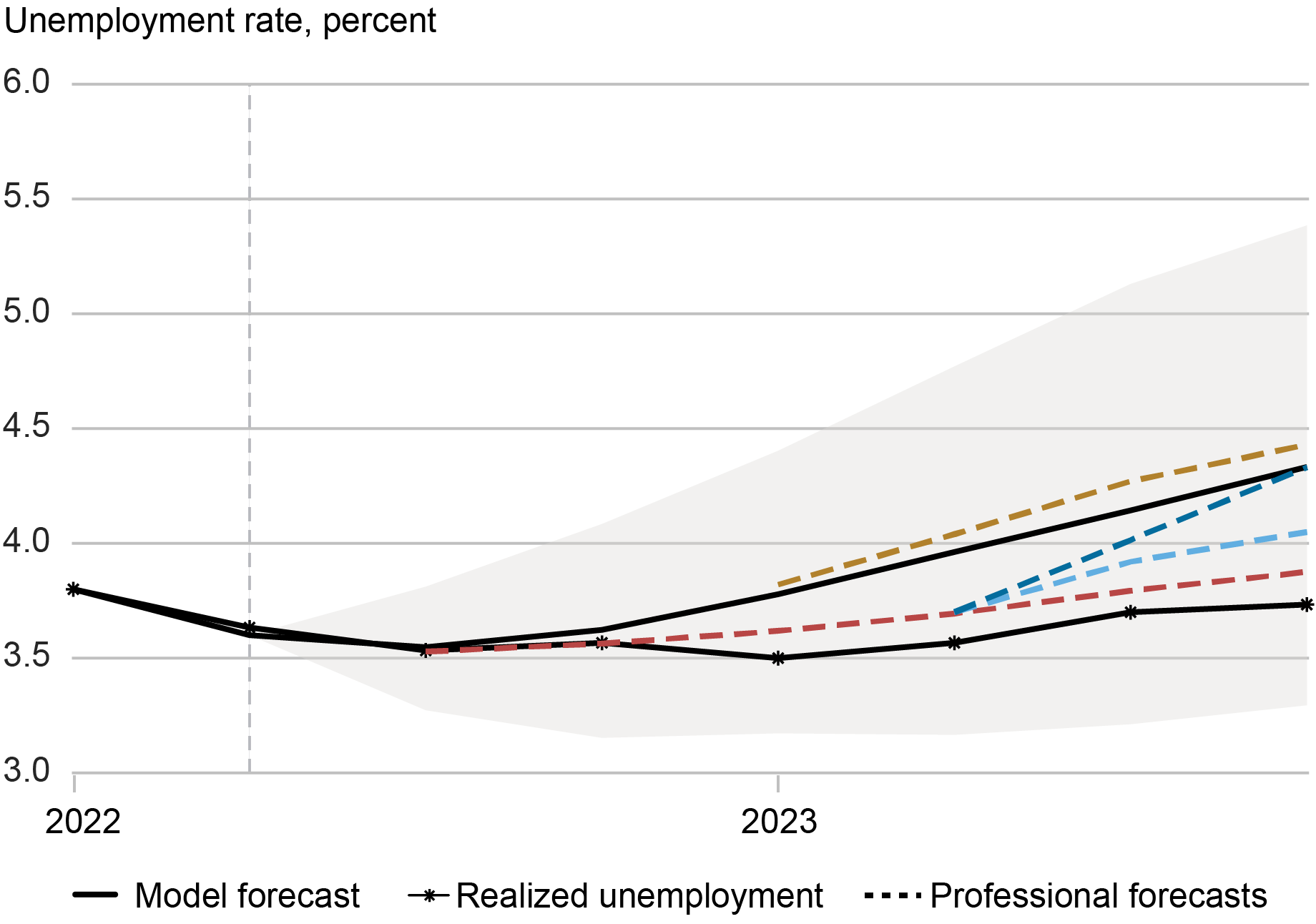

The Mannequin’s Unemployment Forecast Aligns with Skilled Forecasts

Notes: This chart exhibits the mannequin forecast path for the unemployment charge (black line) as of 2022:Q2 (delineated by dashed vertical line), together with the realized unemployment charge (line with asterisks). Dashed traces denote forecast paths from the Survey of Skilled Forecasters and the Blue Chip Financial Indicators Survey at completely different instances. Gray shaded areas denote 68 p.c posterior protection intervals.

The chart above exhibits the unemployment charge forecast generated by our mannequin as of the second quarter of 2022, together with the realized unemployment charge. Clearly, the mannequin forecast was larger than the precise unemployment charge over this era—however that projection aligns with the expectations {of professional} forecasters on the time, additionally plotted above. This expectation of a gradual improve within the unemployment charge then drives the gradual decline in underlying inflation, which is proven within the chart beneath.

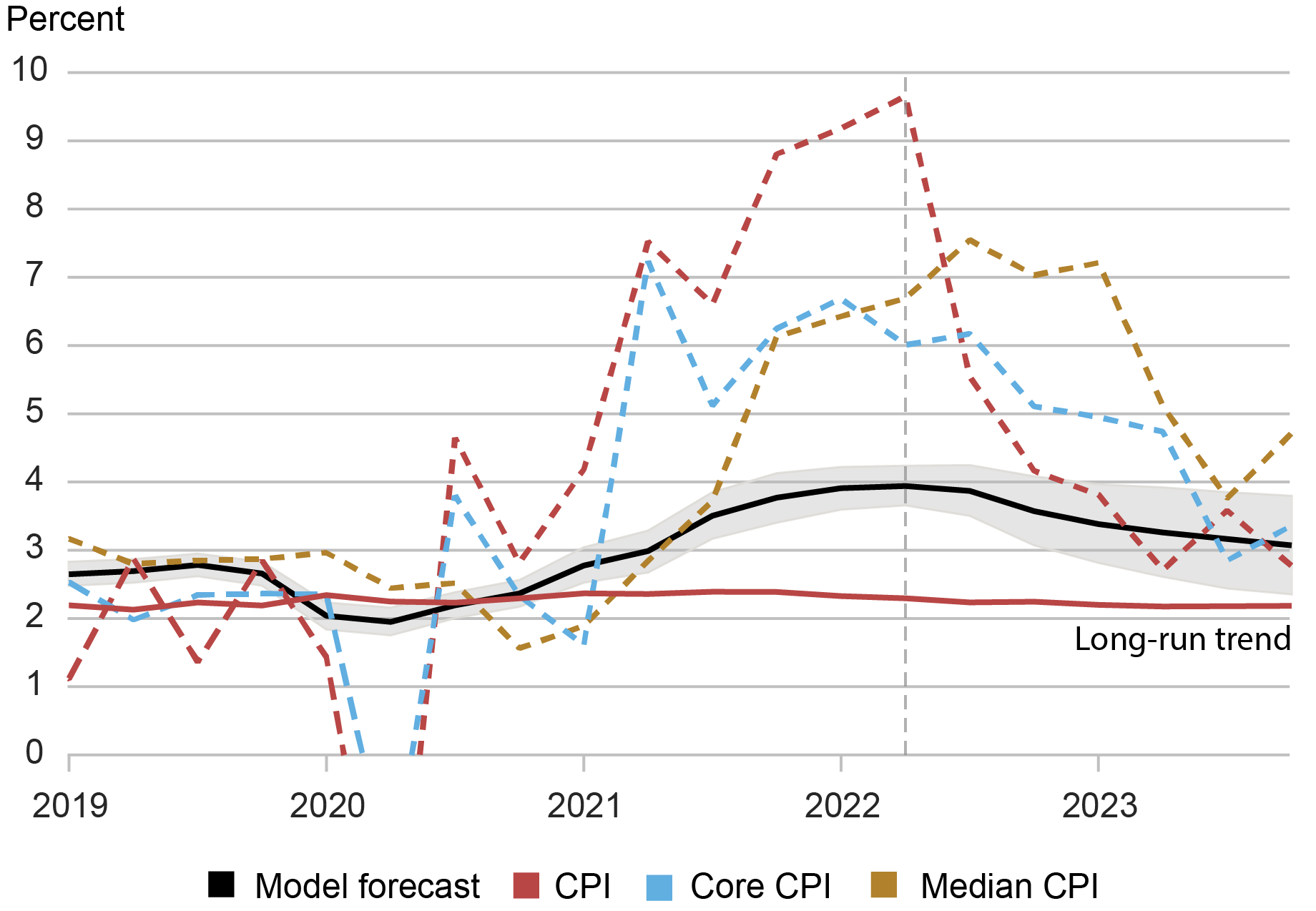

Realized Inflation Converged to the Mannequin Forecast for Underlying Inflation

Notes: This chart exhibits the mannequin forecast path for underlying inflation (black line) as of 2022:Q2 (delineated by the vertical line). Dashed traces denote realized CPI inflation, core CPI inflation, and median CPI inflation from the Federal Reserve Financial institution of Cleveland. Gray shaded areas denote 68 p.c posterior protection intervals.

We are able to see that all the realized inflation measures converged to nearly the very same place: the mannequin forecast for underlying inflation. This tells us two issues. First, it exhibits that underlying inflation is a vital object for higher understanding the medium-term habits of inflation. Second, it provides us confidence in our mannequin’s forecasting means.

The disinflation that occurred from 2022 to 2023 thus exhibits how the habits of inflation relies upon critically on expectations of modifications in labor market situations and, subsequently, on expectations of macroeconomic coverage.

Present Inflation Outlook In accordance with Our Mannequin

So what’s the mannequin’s present forecast for 2024 and past? Within the chart beneath, we present the forecast for underlying inflation utilizing info as much as the fourth quarter of 2023. First, since provide shocks have dissipated, reaching the Fed’s 2 p.c inflation goal requires underlying inflation, itself, to achieve that focus on. The mannequin predicts that additional disinflation—the ultimate mile—is prone to be gradual. It bears emphasizing that these are our model-based forecasts and never official projections.

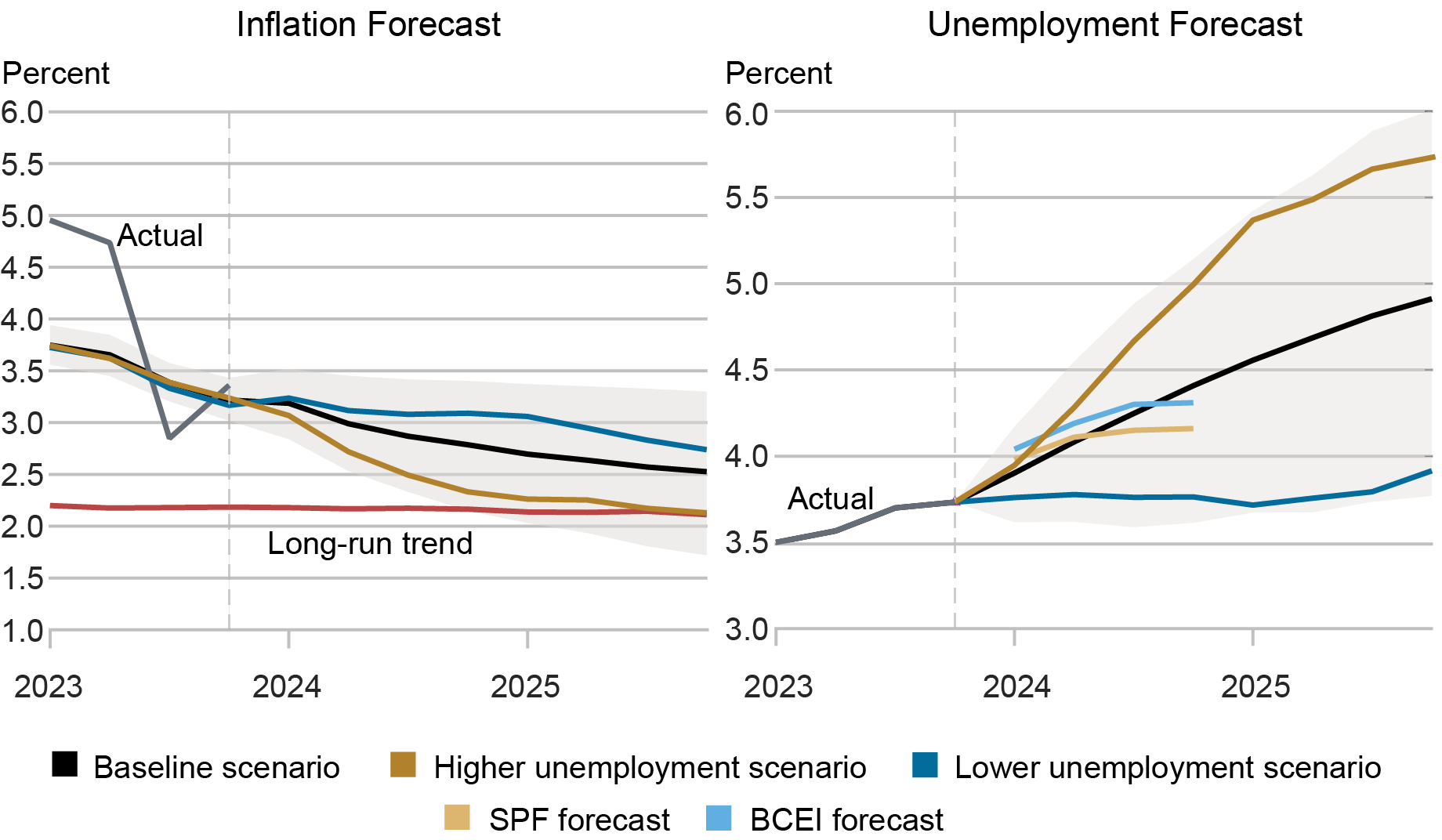

What impacts the velocity of disinflation? Within the chart beneath, the left panel presents three forecast situations for inflation primarily based on attainable future paths of the unemployment charge, proven in the appropriate panel. When the unemployment charge rises sooner than the baseline forecast, then underlying inflation reaches its long-run pattern (crimson line) by the top of 2025 (gold line). Nonetheless, when the unemployment charge strikes sideways, then the tempo of disinflation is slower (blue line).

Labor Market Circumstances Outline the Disinflation Path

Notes: This chart exhibits the mannequin forecast path for underlying inflation (black line, left panel) and the unemployment charge (black line, proper panel) as of 2023:This autumn (delineated by vertical line). The gold line exhibits the inflation forecast primarily based on a steeper improve within the forecasted unemployment charge; the darkish blue line exhibits the inflation forecast primarily based on a shallower improve within the forecasted unemployment charge. The strong crimson line within the left panel denotes the long-run pattern in inflation. Gray shaded areas denote 68 p.c posterior protection intervals. The pair of brief traces in the appropriate panel present unemployment charge forecasts from the Survey of Skilled Forecasters (SPF) and the Blue Chip Financial Indicators (BCEI) Survey as of end-2023.

For comparability, the appropriate panel additionally exhibits the anticipated path of the unemployment charge from the Survey of Skilled Forecasters (SPF) and the Blue Chip Financial Indicators (BCEI) Survey as of the top of final 12 months. These anticipated paths are broadly per the mannequin’s unemployment charge forecasts. Nonetheless, as we realized from the 2022-23 interval, the disinflation course of will rely critically on anticipated macroeconomic situations. Adjustments in these expectations will then have direct implications for the trail for inflation.

Richard Ok. Crump is a monetary analysis advisor in Macrofinance Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Stefano Eusepi is an affiliate professor of economics on the College of Texas at Austin.

Ayşegül Şahin is the Richard J. Gonzalez Regents Chair in Economics on the College of Texas at Austin and an adviser to the Federal Reserve Financial institution of Dallas.

Methods to cite this submit:

Richard Ok. Crump, Stefano Eusepi, and Ayşegül Şahin, “Expectations and the Ultimate Mile of Disinflation,” Federal Reserve Financial institution of New York Liberty Road Economics, March 5, 2024, https://libertystreeteconomics.newyorkfed.org/2024/03/expectations-and-the-final-mile-of-disinflation/.

Disclaimer

The views expressed on this submit are these of the creator(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the creator(s).

[ad_2]