{kind=link}

[ad_1]

Because the frequency and severity of pure disasters enhance with local weather change, insurance coverage—the primary instrument for households and companies to hedge pure catastrophe dangers—turns into more and more essential. Can the insurance coverage sector stand up to the stress of local weather change? To reply this query, it’s essential to first perceive insurers’ publicity to bodily local weather danger, that’s, dangers coming from bodily manifestations of local weather change, equivalent to pure disasters. On this submit, primarily based on our current employees report, we assemble a novel issue to measure the combination bodily local weather danger within the monetary market and focus on its purposes, together with the evaluation of insurers’ publicity to local weather danger and the anticipated capital shortfall of insurers below local weather stress situations.

Bodily Local weather Threat Issue

The first problem in learning insurers’ publicity to local weather danger lies in precisely measuring this danger, notably bodily local weather danger since future local weather situations and influence projections are inherently unsure and depend on varied modeling assumptions. Though historic knowledge can function a proxy for bodily danger, perceptions of such dangers can evolve with new hazards rising and current dangers intensifying. Even when we will measure bodily dangers exactly, one other problem is to measure insurers’ publicity to such dangers, as it may well additionally fluctuate as a consequence of operational adjustments, equivalent to shifts in coverage, gross sales places and reinsurance protection.

In our current employees report, we use a novel method to deal with the challenges of assessing insurers’ publicity to local weather danger. By utilizing a market-based method, and relying solely on publicly accessible knowledge, together with inventory market knowledge, we circumvent the shortage of sufficient knowledge. Particularly, we assemble a number of portfolios which can be designed to fall in worth as bodily danger escalates. One such portfolio contains the shares of public property and casualty (P&C) insurers, with every insurer’s weight decided by its premium publicity to states with a historical past of great pure catastrophe damages. We discuss with the return on this portfolio as a bodily danger issue. This issue can function a forward-looking measure by capturing adjustments in monetary market’s expectations on future bodily local weather change danger.

Why would this issue fall as bodily danger escalates? As future bodily dangers escalate, states which can be extra inclined to pure disasters are prone to expertise larger incidence of such occasions. Consequently, insurers with higher publicity to those states by way of their operations are prone to expertise decrease inventory returns. Nonetheless, there might be counterarguments. First, one may argue that insurers might increase premiums to compensate for the elevated dangers in these states. Nonetheless, regulatory constraints typically hinder insurers from absolutely adjusting premiums to replicate such dangers, notably in high-risk states (see, for instance, Oh, Sen, and Tenekedjieva 2022). Furthermore, larger premiums could deter coverage uptake, thereby lowering insurers’ general income even when insurers can keep per-policy profitability.

Second, one may recommend that insurers might withdraw from dangerous states as bodily local weather dangers intensify. Nonetheless, whereas some insurers could decide to exit unprofitable markets, heightened bodily local weather danger can nonetheless erode the whole income of uncovered insurers.

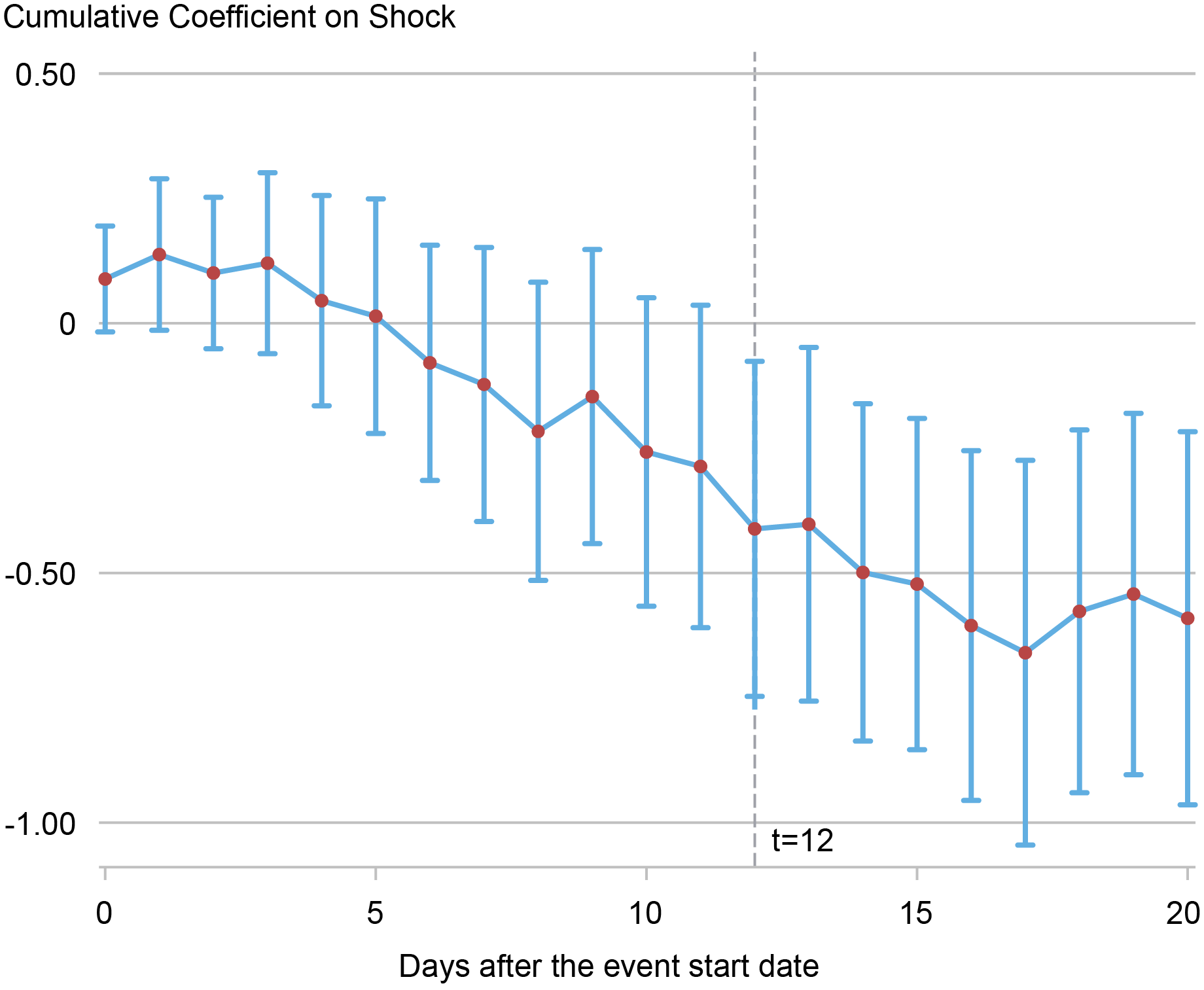

Does the issue work as supposed? If the constructed issue works as supposed, it ought to decline following surprising spikes in bodily local weather danger. Nonetheless, that is troublesome to watch. A possible validation train is to check whether or not the issue drops after extreme climate-related pure disasters happen. The chart under illustrates that the issue usually declines following massive pure disasters, indicating that insurers with substantial publicity in high-risk states expertise a lower in inventory returns after massive pure disasters. Subsequently, when inventory market traders anticipate extra frequent and/or extreme disasters as a consequence of local weather change, we anticipate the issue to say no in worth, as supposed.

Bodily Threat Issue Response round Pure Catastrophe Occasions

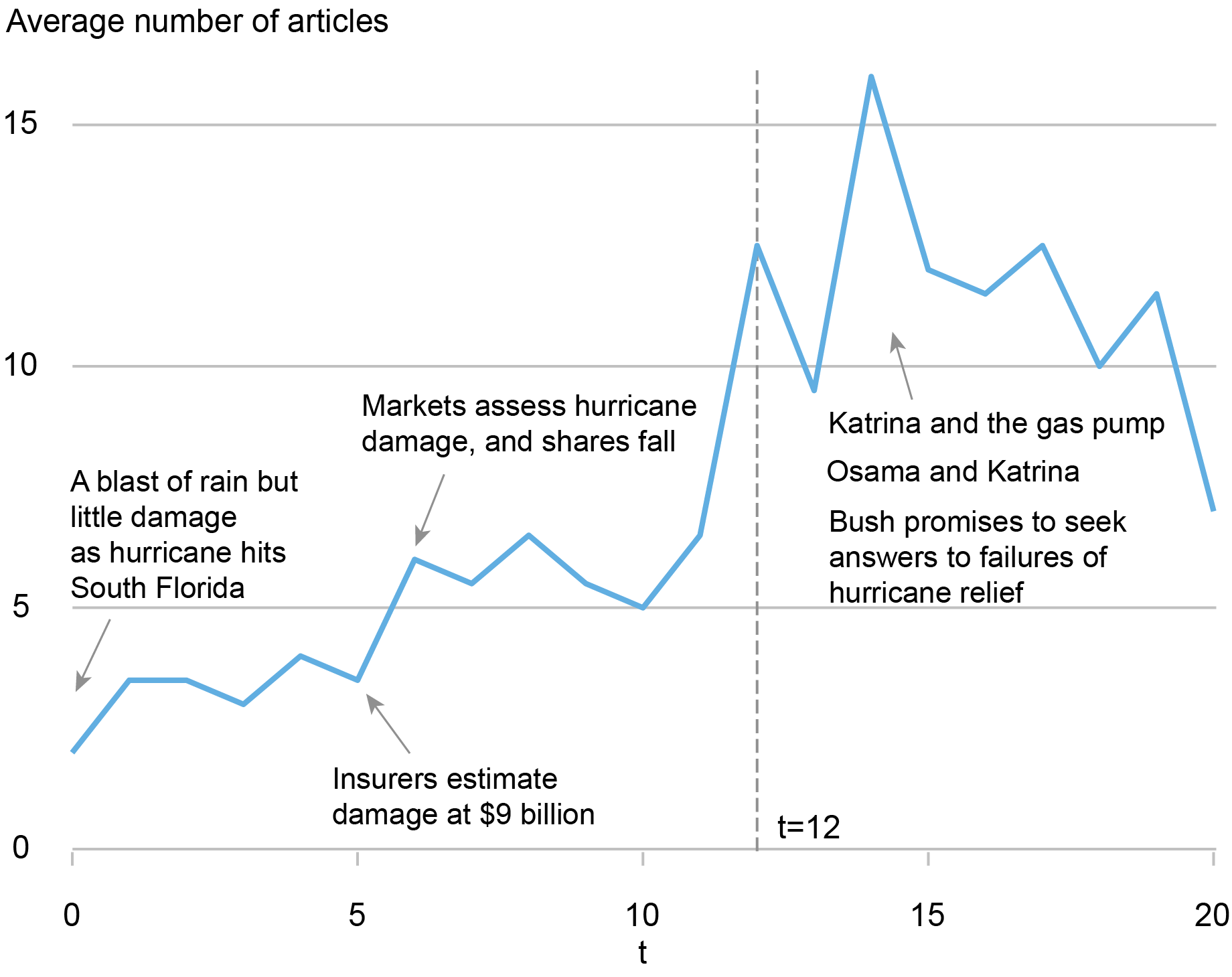

The above chart additionally reveals that the bodily danger issue takes greater than 5 days to reply, seemingly because of the delayed readability concerning the disasters’ influence, equivalent to its severity and period. As an example, throughout hurricane Katrina, preliminary media studies steered little harm in South Florida. It wasn’t till six days later that the monetary market’s response was talked about. Moreover, our evaluation means that the eye to pure catastrophe occasions usually peaks between ten and fifteen days after the occasion’s onset. By monitoring the frequency of occasion mentions in New York Occasions articles that target main hurricanes, we doc a gradual enhance within the variety of articles mentioning hurricanes after the occasion’s begin date, with a pointy rise after twelve days, as illustrated within the chart under. These findings make clear why the issue doesn’t decline instantly after disasters.

The Common Variety of New York Occasions Articles round Pure Disasters

Notes: This chart shows the frequency of mentions of “hurricane” in NYT articles following a hurricane. The beginning date of the occasion is represented as t=0. The typical variety of mentions is calculated throughout probably the most vital hurricanes (ninety fifth percentile of all hurricanes generated loss). We concentrate on these massive hurricanes as a consequence of their heightened public consideration and assumed higher influence available on the market.

The Bodily Local weather Beta

Our issue has a variety of purposes. As an example, by estimating monetary establishments’ inventory return sensitivity to the bodily danger issue, one can estimate the anticipated extent of capital shortfall skilled by establishments throughout extreme declines within the bodily danger issue. We current leads to the paper demonstrating this software, specializing in insurance coverage firms. Particularly, we calculate insurers’ time-varying inventory return sensitivity to the bodily danger issue whereas controlling for market components, that we name the “bodily local weather beta”.

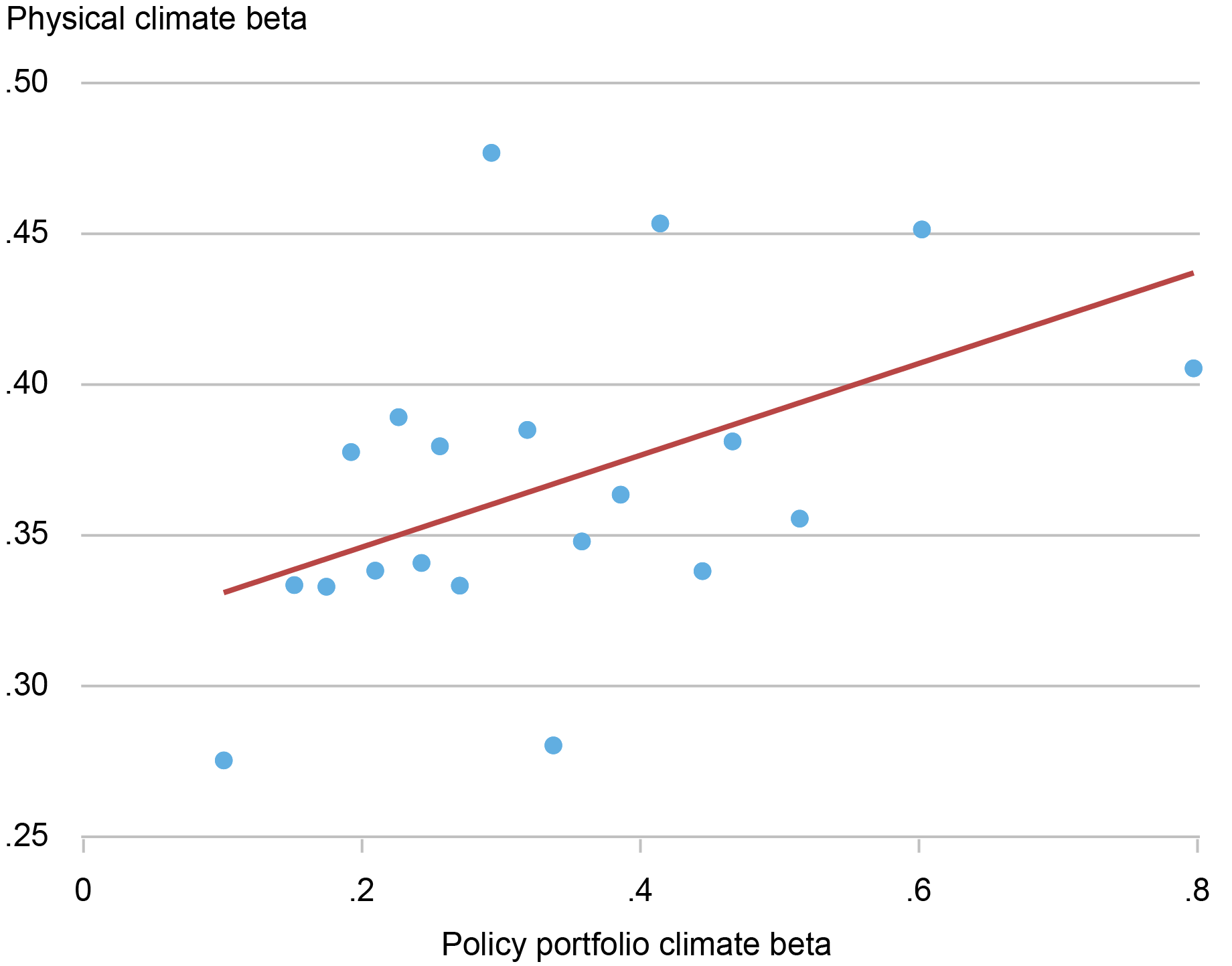

To validate that this “beta” is reflective of dangers in insurers’ operations, we evaluate this “bodily local weather beta” (which is predicated on insurers’ inventory returns) with insurers’ “coverage portfolio local weather beta.” We estimate the latter because the weighted common riskiness of states in insurers’ coverage portfolios utilizing detailed knowledge on the place insurers underwrite insurance coverage insurance policies. Every state’s danger degree is assessed by analyzing municipal bond returns, since prior analysis reveals that these returns replicate bodily danger. We calculate how delicate county-level municipal bond returns are to bodily danger components and combination the sensitivity measure to the state degree.

The chart under means that the stock-based measure (denoted “bodily local weather beta”) aligns with the “riskiness” of insurers’ coverage portfolios, as measured by their “coverage portfolio local weather beta.” Within the cross part, smaller insurers have bigger bodily local weather danger exposures. The alignment between the 2 betas can function a foundation for assessing the bodily danger publicity of unlisted insurance coverage firms that don’t have publicly listed shares however disclose operational publicity throughout states.

Correlation between Bodily Local weather Beta and Coverage Portfolio Beta

Notes: This chart demonstrates binned scatter plot of insurer bodily local weather beta and coverage portfolio local weather beta, primarily based on annual knowledge from 2005 to 2019 for listed P&C insurers within the U.S.

Remaining Phrases

Because the frequency and severity of pure disasters escalate, households and companies flip to insurance coverage to mitigate local weather danger. Can the insurance coverage sector climate the challenges posed by local weather change? To handle this essential query, we introduce a novel bodily local weather danger issue that has all kinds of purposes such because the quantification of particular person insurance coverage firm’s publicity to bodily dangers and assessing the vulnerability of economic system to local weather change danger. Along with bodily danger, the paper additionally assesses insurers’ publicity to transition local weather dangers, the dangers coming from regulatory adjustments, utilizing the framework developed by Jung, Engle, and Berner (2021).

Hyeyoon Jung is a monetary analysis economist in Local weather Threat Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Robert Engle is a professor emeritus of finance on the New York College Stern Faculty of Enterprise.

Shan Ge is an assistant professor of finance on the New York College Stern Faculty of Enterprise.

Xuran Zeng is a Ph.D. scholar in finance on the New York College Stern Faculty of Enterprise.

How you can cite this submit:

Hyeyoon Jung, Robert Engle, Shan Ge, and Xuran Zeng, “Bodily Local weather Threat and Insurers,” Federal Reserve Financial institution of New York Liberty Avenue Economics, April 3, 2024, https://libertystreeteconomics.newyorkfed.org/2024/04/physical-climate-risk-and-insurers/.

Disclaimer

The views expressed on this submit are these of the writer(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).

[ad_2]