[ad_1]

Immediately we’ll give a high-level take a look at half one in all Jonathon Sine’s The Rise and Fall of LGFVs. Sine’s article may be very detailed, but written with a watch to holding reader curiosity. Right here Sine succeeds by going via the historical past of how these autos, which have are the mechanism for blowing China’s actual property bubble so huge and creating severe financial/funding distortions.

I hope to restrict how a lot I recap the evolution of the LGFVs and as an alternative give attention to how they’ve created large leverage in these constructions, together with (in lots of circumstances) a lot complexity that they’d be troublesome to unwind even when somebody have been so daring as to try that.

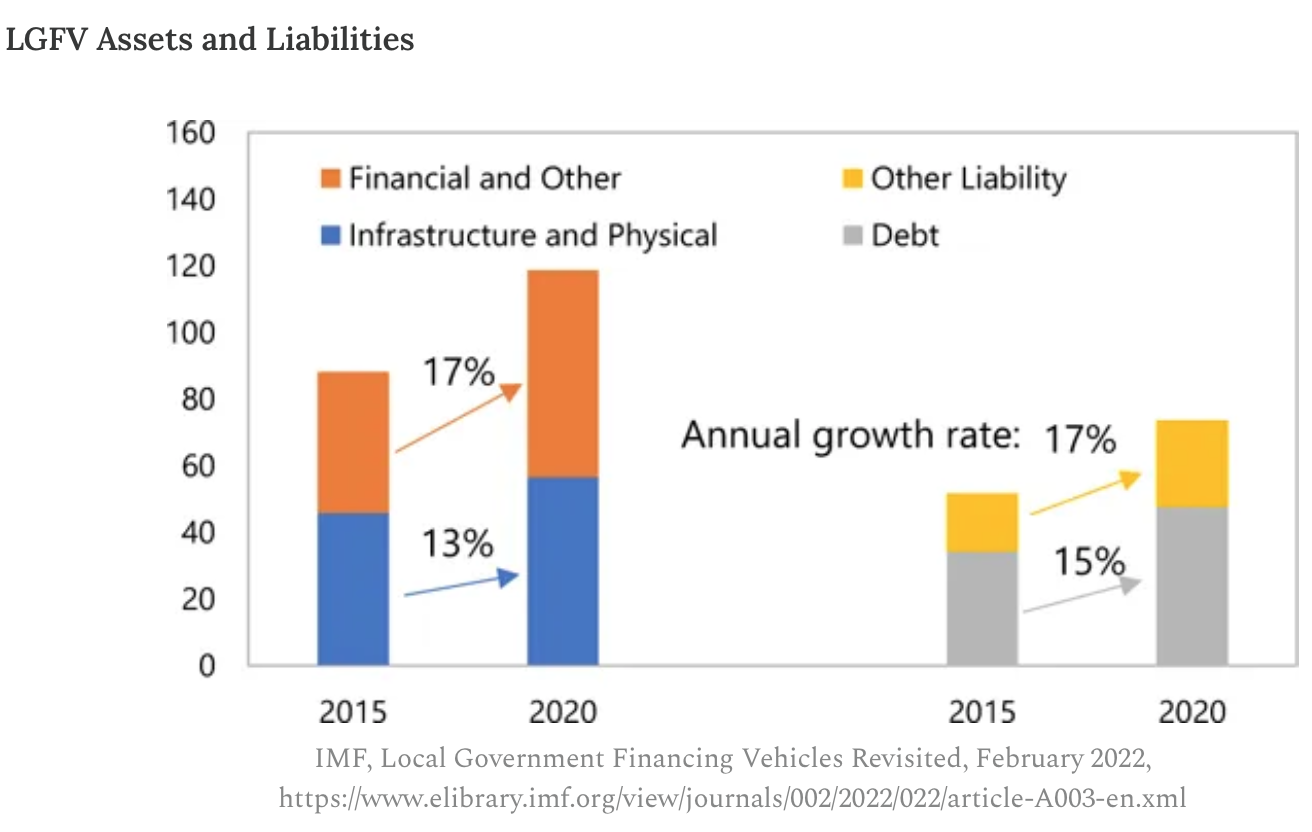

What leaps out of Sine’s account are three main damaging options of the International Monetary Disaster: Hyman Minsky-esque Ponzi finance, leverage on leverage, and complexity. This resemblance turns into extra disconcerting in mild of the dimensions of the LGFVs: their whole property are roughly 120% of Chinese language GDP and their liabilities, 75%.

As disconcerting is that they’ve been rising at a markedly larger price than general financial development, even at their present giant dimension. LGFVs will eat the economic system! Wellie not however they positive are attempting:

Allow us to return to the primary huge alarm bell, the truth that the LGFVs are almost all an train in Ponzi financing. For these of you who missed the dialogue through the monetary disaster years, here’s a abstract of economist Hyman Minsky’s concept and terminology, from a 2007 submit:

Hyman Minsky, an economist who studied speculative conduct within the wake of the 1929 crash, noticed that collectors change into extra lax about lending requirements throughout occasions of stability. He divided debtors into three sorts: the upstanding kind that may pay principal and curiosity; speculative debtors (or “models”), who will pay curiosity however should maintain rolling the principal into new loans; and “Ponzi models” which may’t even cowl the curiosity, however maintain issues going by promoting property and/or borrowing extra and utilizing the proceeds to pay the preliminary lender. Minsky’s remark:

Over a protracted interval of fine occasions, capitalist economies have a tendency to maneuver to a monetary construction in which there’s a big weight of models engaged in speculative and Ponzi finance.

What occurs? As development continues, central banks change into extra involved about inflation and begin to tighten financial coverage,

….speculative models will change into Ponzi models and the online value of beforehand Ponzi models will shortly evaporate. Consequently models with money stream shortfalls might be compelled to attempt to make positions by promoting out positions. That’s more likely to result in a collapse of asset values.

Once more, remember the important thing function of Ponzi finance being unable to pay curiosity in full, and having to depend on asset gross sales or but extra borrowing to satisfy obligation. From Sine:

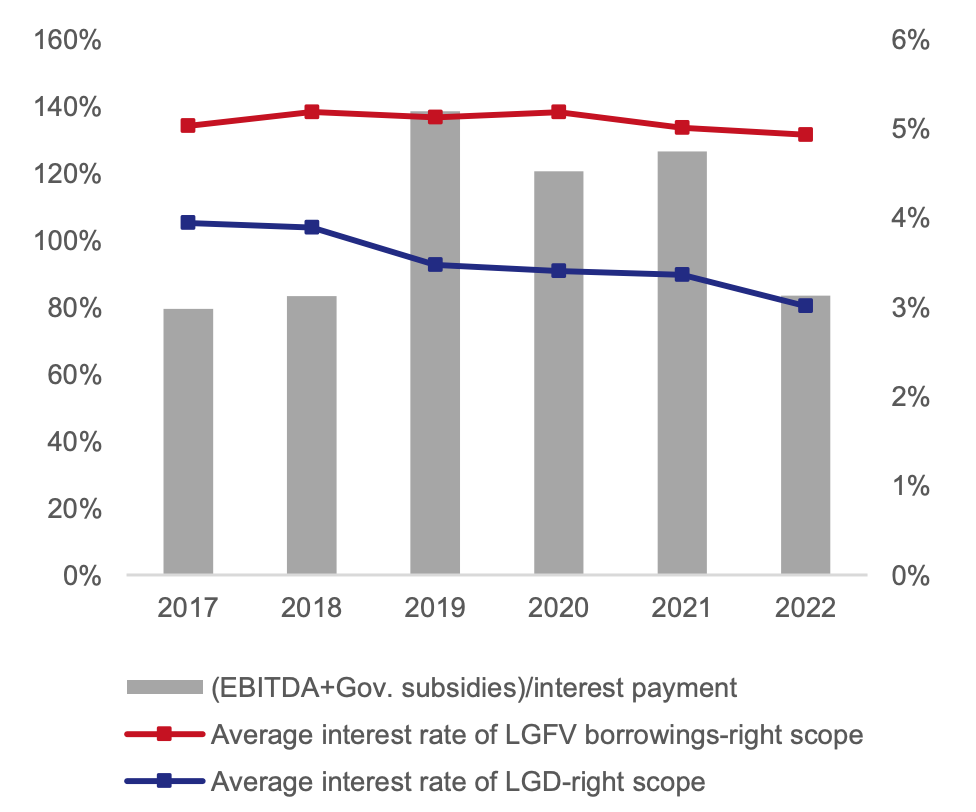

LGFV’s monetary scenario is, to place it frankly, very unhealthy. In mixture, earnings (earlier than curiosity, taxes, and depreciation, i.e., EBITDA) don’t cowl even their curiosity funds. Together with authorities subsidies solely often pushes the curiosity protection ratio above one. Furthermore, the common borrowing value for LGFVs, 5% or so, far outpaces their 1% return on property, posing apparent sustainability issues.

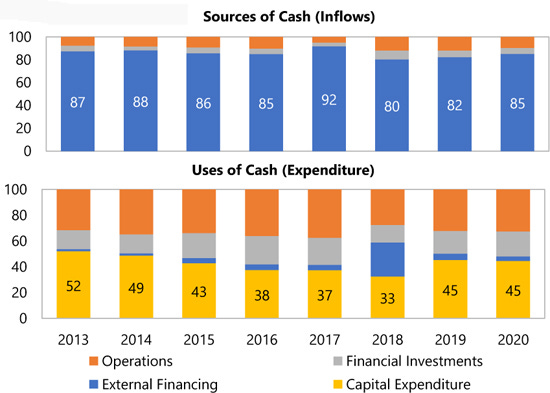

Money flows paint an equally troubling portrait. Yearly 80 to 90 p.c of LGFV spending is funded by new debt. On the entire, LGFVs working inflows don’t come near masking working bills. New debt is routinely added merely to make up the hole and maintain present operations.

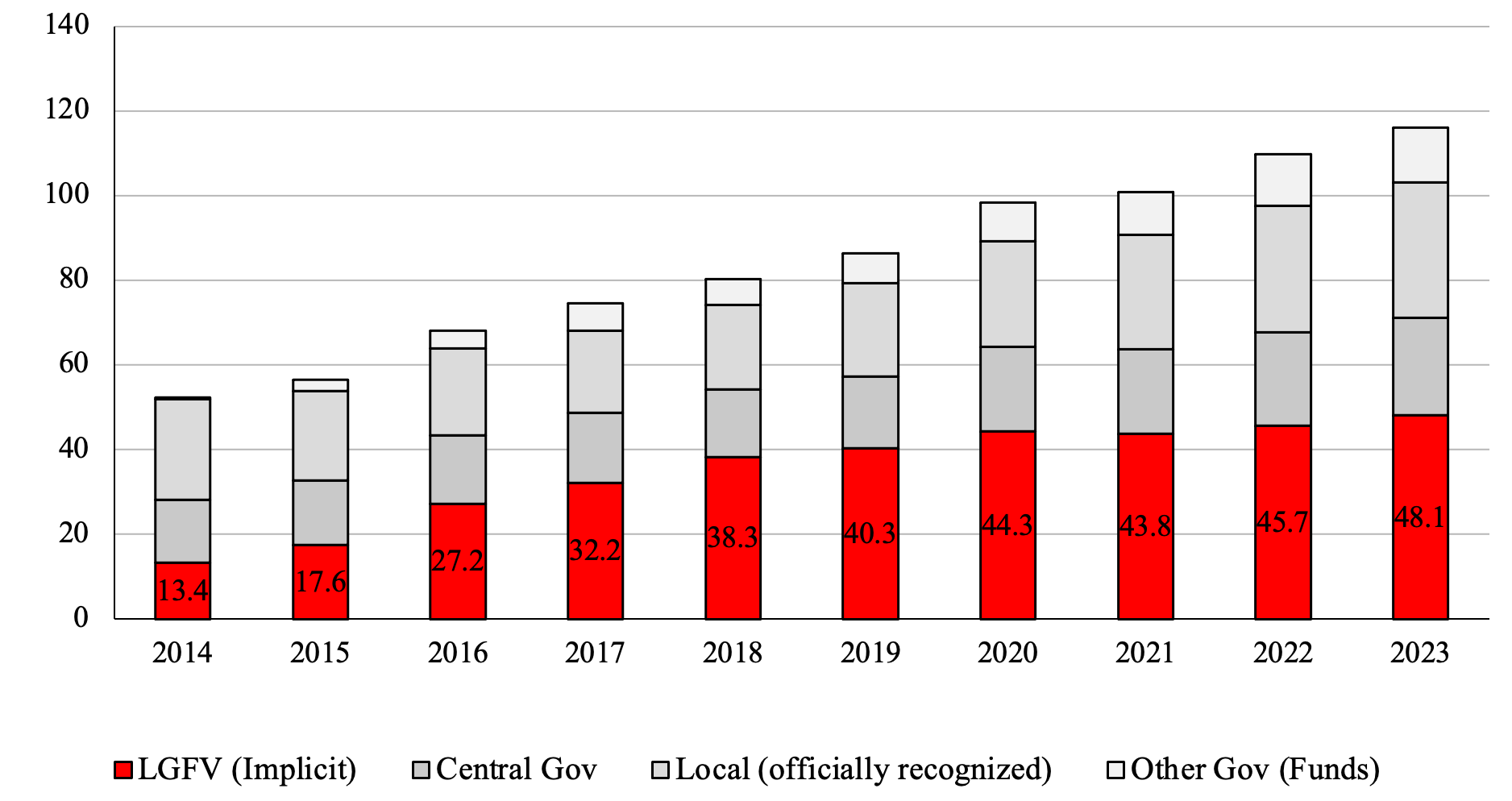

As is predictable from the above financials, the inventory of interest-bearing LGFV debt has nearly unceasingly expanded.4 In line with statistics from the IMF, LGFV’s interest-bearing debt has grown from 13% of GDP, or RMB 8.7 trillion, in 2014 to 48% of GDP, or RMB 60.4 trillion, in 2023.

LGFV interest-bearing debt is even bigger than the IMF knowledge above suggests. An unavoidable limitation of assessing LGFVs by way of backside up knowledge, as the entire above sources do, is that it solely captures the 2-3,000 LGFVs which have issued bonds and printed related financials. One other 9-10,000 smaller LGFVs have by no means accessed the bond market and are due to this fact merely lacking from the information.6 A easy means of making an attempt to estimate the remainder of the interest-bearing LGFV debt is to imagine LGFVs comply with a Pareto distribution.7 Doing so suggests IMF estimates most likely understate debt by 25%. A extra affordable, if nonetheless seemingly conservative, estimate of curiosity bearing LGFV debt might be 60% of GDP, or RMB 75 trillion, in 2023.

We’ll skip over the primary a part of Sine’s in-depth historical past of how the LGTVs got here to be. A brief and extremely simplified model is that Chinese language authorities was exceptionally decentralized, which within the post-Mao, pro-market period grew to become an issue because the function of state-owned enterprises and tax revenues shrank. Beijing, to revive its energy, applied a system within the early Nineteen Nineties very a lot akin to Richard Nixon’s income sharing, however extra so: the central authorities collected tax receipts and distributed them to native entities to spend, with the funds typically going via advanced channels. Items and providers taxes account for about 60% of the full, with solely about 6.5% from earnings taxes.

So the native governments acquired across the central authorities income constraints by creating off-budget liabilities. And the LGTV was devised by specialists on the China Improvement Financial institution.

Skipping over the mechanisms the native governments used, the funding got here from banks….which more and more have been newly-created, domestically managed banks. Not laborious to see the place that is going…

To quick ahead to the worldwide monetary disaster, recall that China engaged in very giant scale stimulus whereas the remainder of the world underspent. As Sine notes:

When the middle boldly introduced its RMB 4 trillion stimulus plan to push back recession, it didn’t intend to fund the stimulus immediately however as an alternative turned to native governments, now replete with financial institution licenses and financing car. To today we don’t know precisely how a lot China truly spent on its stimulus, although its clear the overwhelming majority got here off-budget by way of LGFVs….

Predictably, Beijing shortly misplaced what little management it had of the LGFV growth course of. Not solely was the credit score growth a lot higher than Beijing meant, however LGFVs institutional function expanded and embedded deeper into the sinews of China’s economic system.

The central authorities grew to become sad with how the LGFVs had gotten too huge for his or her britches, first working intrusive audits, then creating lists of shaky-looking LGFVs and urgent banks to not lend to them.

So the LGFVs discovered new cash sources: municipal company bonds, which by 2018 had change into 1/3 of all company bonds, and shadow banking.

One other echo of the disaster comes within the half-pregnant standing of the company municipal bonds. Once more from Sine:

…..most “bond patrons most popular LGFV bonds as a result of they provided larger yields than company debt, however have been thought of authorities assured, despite the fact that they funded tasks that sometimes had no capability to repay the debt.”

Keep in mind how Fannie and Freddie debt have been thought of to be authorities assured, till Freddie wanting inexperienced on the gills compelled the popularity that they weren’t, legally? After which Treasury put each Fannie and Freddie into conservatorship to comprise market upset?

Sine factors out that each the company municipal bonds and the shadow banking, which consists primarily of so-called wealth administration merchandise, truly do wind up again at banks, in ways in which circumvent rules:

Wealth Administration Merchandise (WMPs), or particular funds set as much as skirt rules on deposit charges, are an important shadow banking product. WMPs invested closely in municipal company bonds. Chen and He et al calculate that 62% of all MCB proceeds got here from WMPs. And it was banks that created these WMPs, after all with cash that finally belongs to family depositors/lenders.

There are further flavors of LGFV-financing regulatory arbitrage, comparable to entrusted loans and belief firms.

Allow us to now flip to a second concern, leverage on leverage. That was what arrange the Roaring Twenties increase to finish within the Nice Crash (with trusts of trusts of trusts and CDO-like construction) and the Monetary Disaster (during which, as we confirmed in ECONNED, CDOs created spectacular leverage). Sine offers an instance:

Zunyi is comparatively unremarkable, a metropolis of middling inhabitants and financial improvement, firmly within the third tier of China’s unofficial metropolis rating system. One current improvement, nevertheless, has as soon as once more introduced consideration to the town: the more and more pressing Get together-state effort to take care of LGFV debt. Zunyi Highway and Bridge Development (遵义道桥建设) is the star of the present. A snapshot of Zunyi’s company construction presents hints at a number of the poblems.61

Zunyi Highway and Bridge, like most LGFVs, is fully-owned by the native, on this case city-level, State Asset Supervision and Administrative Fee (SASAC).62 Established in 1993 and with registered capital of RMB3.6 billion, it’s the second largest of of Zunyi SASAC’s 40+ holdings, a lot of which additionally seem like LGFVs. Zunyi Highway and Bridge is itself a holding firm with no less than 10 firms beneath its umbrella. Many of those corporations are additionally LGFVs. Its largest holdings embody: Zunyi Daoqiao Agricultural Expo Park Co., Ltd., Zunyi Daoqiao Resort Administration Co., Ltd., Zunyi New District Development Funding Group Co., Ltd., and Zheng’an County City and Rural Development Funding Co., Ltd.

Zunyi Highway and Bridge Holdings

Zunyi Highway and Bridge holding construction, 遵义道桥建设(集团)有限公司, 股权穿透图, by way of 爱企查 https://aiqicha.baidu.com/company_detail_69261055076241

Highway and Bridge’s subsidiaries even have subsidiaries. Take for instance, its largest subsidiary: Zunyi Metropolis Baozhou District City Development and Funding (遵义市播州区城市建设投资经营), with registered capital of RMB 1.6 billion. Baozhou City Development itself fully-owns a various array of 10+ companies, starting from a funeral service firm, to a monetary leasing firm seemingly centered on industrial gear, to a water providers administration firm, in addition to a 49% stake in a property administration firm and a 5% stake in one other diversified LGFV holding firm.Holdings of Highway and Bridge Largest Subsidiary, Baozhou City Development

Zunyi Metropolis Baozhou District City Development Funding Administration (Group) Co. (遵义市播州区城市建设投资经营(集团)有限公司), 股权穿透图, by way of 爱企查 https://aiqicha.baidu.com/company_detail_62311309937102

The financing practices to associate with such an online of holdings have been equally convoluted. One firm could purchase loans or go to the bond market solely to on-lend to its affiliated entities. There are lots of, maybe 1000’s, of LGFVs like Zunyi Highway and Bridge and just like the one in Dashan County talked about earlier. These conglomerate LGFVs undertake what economist David Daokui Li describes as a “nested layering method” to leverage. Corporations at one degree borrow funds, use that borrowed capital to safe further loans on the subsequent subsidiary degree, and amplify debt layer by layer. All of the whereas transferring into increasingly more strains of enterprise.

{kind=link}

Evidently, multi-entity enterprises, all lashed along with cross-ownership and debt, are well-nigh unimaginable to research precisely, not to mention unwind. AIG had an identical chicken’s nest of exposures in its property and casualty subsidiaries, with cross-ownership, cross-guarantees, and totally different fiscal 12 months finish dates too. Recall that when AIG was successfully nationalized, the plan was to promote its numerous entities. That by no means occurred. The cross-exposures have been a giant purpose why.

To maintain the submit to a manageable size, and never over-hoist from Sine, we’re giving comparatively quick shrift to the third worrisome signal, complexity. You may simply see the organizational and monetary complexity of the Zunyi Highway and Bridge entities. We’ve left out the complexity of the companies that the LGFVs get into. An extract from an extended dialogue:

As they expanded, LGFVs moved out properly past their preliminary infrastructural and land improvement remit. One analogy is that LGFVs have change into akin to 12 thousand little Huarongs. Huarong, the nation’s largest asset administration firm, was established only a 12 months after the primary LGFV in 1999. Colloquially known as a “unhealthy financial institution” as a result of it was set as much as take non-performing loans off the Industrial and Industrial Financial institution of China’s stability sheet. Initially an asset restoration agency, Huarong metastasized into an enormous conglomerate with dozens of subsidiaries concerned as many alternative industries. The crazed growth acquired so crazed beneath former Chairman Lai Xiaomin that the CPC determined to execute him.

See this instance:

Now this whole mess would appear primed for a really unhealthy finish. But many commentators have been predicting unhealthy ends for China’s actual property bubble and its myriad financing mechanisms for a while, and no disaster has occurred.

Nevertheless, one other final result from a giant debt overhang is zombification: an excessive amount of cash going to refinancing what would in any other case be unhealthy debt, on the expense of higher makes use of.

Herbert Stein famously mentioned, “That which may’t proceed, gained’t.” However he was silent on when “gained’t” would possibly come to move.

[ad_2]