{kind=link}

[ad_1]

Keep knowledgeable with free updates

Merely signal as much as the Currencies myFT Digest — delivered on to your inbox.

Ruurd Brouwer is the chief government of TCX, and Barry Eichengreen is professor of economics and political science on the College of California, Berkeley.

The relation between banker and borrower is difficult. They want one another however have opposing pursuits and totally different ranges of experience. As a result of banks are financially extra refined than households, governments undertake consumer-protection legal guidelines to safeguard their pursuits. However not all debtors are protected.

A soon-to-be-published IMF survey of nationwide debt administration workplaces in rising and creating economies reveals that such data asymmetries should not restricted to business banks and home debtors.

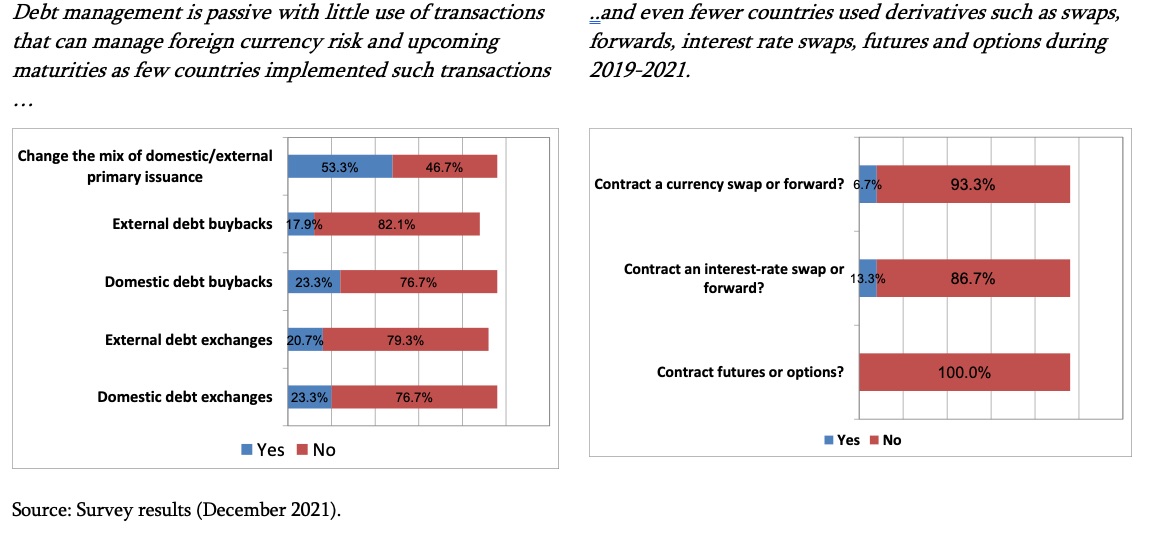

The grim actuality is that in lots of instances DMOs nonetheless lack the coaching and data to grasp even the beautiful primary dangers of borrowing in international, onerous foreign money — the traditional “unique sin” of rising markets.

In accordance with the IMF survey, half of responding DMOs don’t carry out stress exams on the native foreign money worth of the debt inventory, nor on curiosity funds and amortisation funds. Fewer than half had a foreign money threat administration technique, and solely a 3rd had senior workers devoted to the danger administration of the sovereign debt ebook.

In impact, poor nations are driving their “debt cell” at 100mph at midnight with no headlights, and no map. Blindfolded.

The IMF has discovered that this unattended foreign money threat leads on to accidents. A research of 222 debt surges in creating nations over the previous 50 years discovered that foreign money threat alone brought about debt/GDP ratios in low-income nations shoot up 35-50 share factors throughout crises.

That’s like Germany’s debt-to-GDP going from 60 per cent to 110 per cent in a single yr. Such a rise would push a creating nation instantly into excessive threat of default, or straight into default itself. And that’s precisely what’s taking place at present in some nations.

About 90 per cent of respondents to the survey indicated additional that it was necessary to pursue capability growth in areas like threat quantification, using derivates and native capital market growth. This meshes with this yr’s World Financial institution Worldwide Debt Report, which has good recommendation to DMOs in low and center earnings nations:

As soon as a portfolio evaluation is carried out, debt managers can make use of an lively debt administration technique — together with repurchases, swaps, and cancellations. If completed accurately, such a technique can optimize the profile of the general public debt and obtain appreciable monetary beneficial properties.

Sadly, methods that have been rightfully positioned below the heading of modern practices are, in actuality, at a really totally different state of development, in response to the IMF survey . . .

{kind=link}

All this reveals the painful data asymmetry on the debt negotiation desk: on one aspect are debtors with restricted data of foreign money threat administration, whereas on the opposite the World Financial institution and the IMF which are filled with financially-savvy staff (and banks and bond funds have hordes of them).

Defenders of the multilateral growth banks will reply that the World Financial institution and different MDBs — in contrast to business lenders — should not return maximisers. However does this imply that their purchasers are protected against taking up extreme threat?

Effectively . . . no. The event banks are threat minimisers, mandated to guard their AAA score. Offloading foreign money threat is as pure for a growth banker as maximising return is for a business banker.

Perhaps we must always look to classes from central and jap Europe, the place hundreds of thousands of shoppers succumbed to an identical ‘alternate price phantasm’ earlier than the 2008 monetary disaster. Attracted by low rates of interest they selected Swiss franc mortgages, ignoring the danger of foreign money depreciation till it occurred.

At this level, nonetheless, shopper safety provisions kicked in. The European Central Financial institution highlighted the “malign riskiness of international foreign money loans”, and the European Monetary Stability Board warned of the systemic dangers that it entailed, and issued the next suggestion on lending in foreign currency echange to its member nations:

— Require monetary establishments to supply debtors with ample data relating to the dangers concerned in international foreign money lending (…).

— Encourage monetary establishments to supply clients home foreign money loans for a similar functions as international foreign money loans in addition to monetary devices to hedge towards international alternate threat.

The European Union’s Mortgage Credit score Directive formalised the EU’s place that debtors ought to have the correct to transform loans to the foreign money by which the borrower receives their earnings, or that there are different preparations to restrict foreign money threat in place.

On the request of the European parliament’s Committee of Financial and Financial Affairs, the Coverage Division issued recommendation on the mis-selling of international foreign money mortgages — outlined as “practices which are detrimental to clients, with or with out unlawful behaviour”.

There’s a direct analogy right here. The three suggestions to guard purchasers from mis-selling international foreign money loans needs to be equally relevant to at present’s sovereign debt disaster: there needs to be social coverage measures geared toward masking the losses of essentially the most weak clients.

Closely-indebted low-income nations must also be supplied with “accessible and efficient out-of-court dispute decision mechanisms”. Their absence is a painful reminder of the G20’s Frequent Framework’s ineffectiveness. As within the case of international foreign money mortgages, “the prices of mis-selling should be borne by the establishments that brought about it.”

[ad_2]