{kind=link}

[ad_1]

America is in a bizarre place demographically-speaking.

On the one hand, now we have 70 million child boomers reaching retirement age. They management many of the wealth. They management many of the housing market. And so they nonetheless management the thermostat whenever you go to their homes.

Then again, now we have 73 million millennials who’re of their prime family formation years. They don’t management practically as a lot wealth (however they’ll sometime). They don’t personal many of the homes (however they’ll sometime).

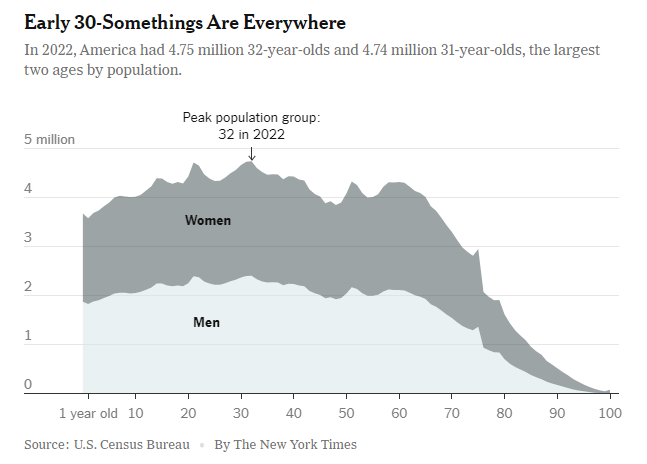

The 2 largest ages in america proper now are 31 and 32-year-olds (by way of The New York Occasions):

Millennials aren’t youngsters anymore. They’ve jobs. They stay within the suburbs. They’re shopping for homes (or wish to). They’ve youngsters.

And what do you do in your family formation years? You spend cash. Transferring is pricey. Housing is pricey. Children are costly. Filling your own home with stuff is pricey.

In America we like to eat and the most important demographic is coming into their prime consumption years. That is going to supply a ground below the economic system for years to return.

The millennial homeownership charge is roughly 50%. Gen X is greater than 70%, and child boomers are nearer to 80%. Loads of millennials will likely be trying to purchase houses within the years forward to fill that hole.

In a supply-constrained market the place we merely aren’t constructing sufficient houses, the hope is the newborn boomers will present that offer as they retire, downsize, use their dwelling fairness to fund retirement or ultimately die off.

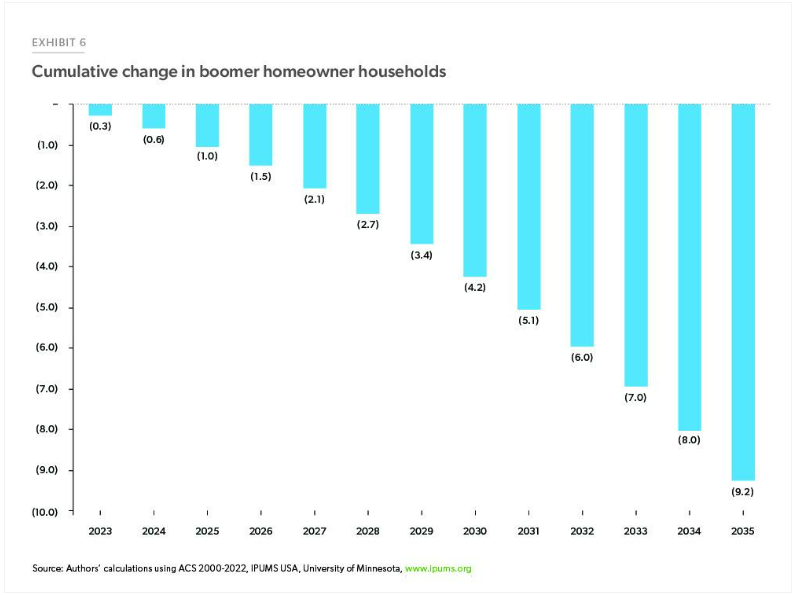

In line with Freddie Mac, don’t rely on a wave of child boomer homes hitting the market. They estimate the whole variety of child boomer households will go from 32 million now to round 23 million by 2035 because the oldest boomers flip 90.

Over the following 5 years that’s roughly 2.7 million houses that can change arms:

That’s extra like a small breeze on the seashore than a tsunami.

However perhaps younger individuals will get fortunate. Demographic developments don’t at all times comply with the script.

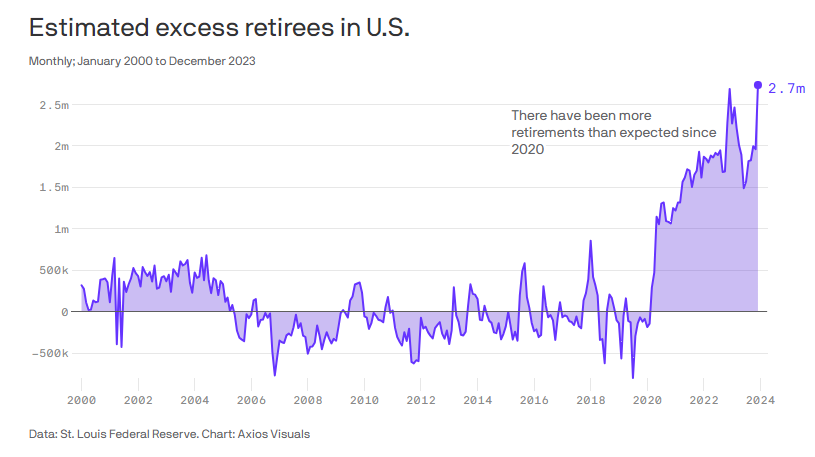

Simply have a look at the variety of child boomers who retired early following the pandemic (by way of Axios):

A rising inventory market, increased housing costs, and a few existential stuff from Covid gave us 2.7 million extra retirees than anticipated.

My preliminary thought right here is this might really assist the economic system. Youthful individuals can step into the roles boomers are vacating. The newly retired will likely be spending a few of the cash they’ve been hoarding. Good luck discovering a deal on a cruise ship for the following 20 years.

Early retirees aren’t the one ones who ought to really feel higher about their web value.

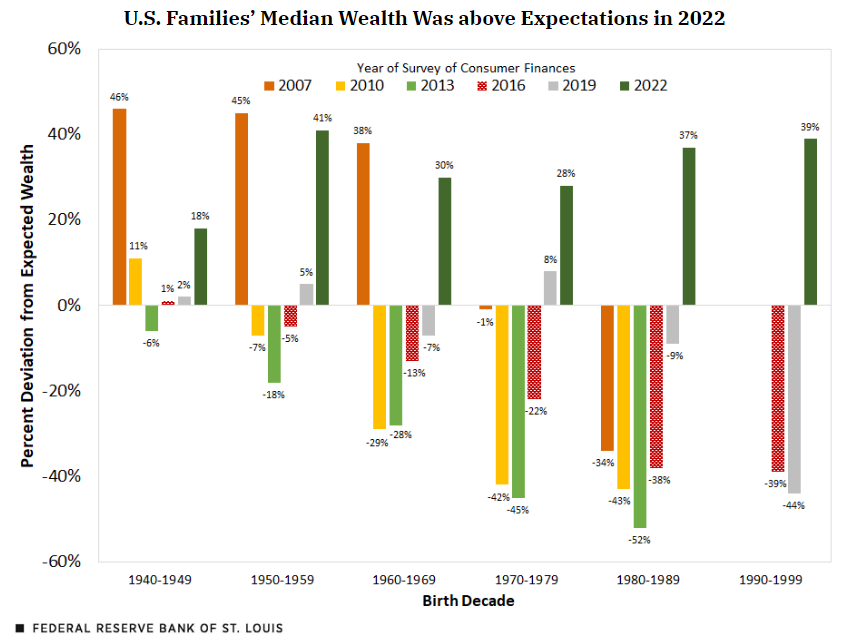

Again in 2019, I wrote a chunk about how younger individuals have been 34% under their predicted wealth ranges based mostly on the expertise of earlier generations on the identical age. The Nice Monetary Disaster did a quantity on millennials.

The pandemic reversed that development after which some. These are the up to date numbers from the St. Louis Fed:

They clarify:

We discovered that the median wealth of older millennials (these born between 1980 and 1989) was 37% above expectations. The wealth of youthful millennials and older Gen Zers (these born between 1990 and 1999) was an identical 39% above expectations.

So, in simply three years, we went from a state of affairs the place older millennials have been 34% under expectations to 37% above expectations–a 71% level swing!

Clearly, increased housing costs helped however for sure we’ve by no means seen something like this earlier than.

No matter their present place in life, millennials would be the richest technology in historical past. Knight Frank laid it out of their annual wealth report:

The change will see $90tn of property transfer between generations within the US alone, “making prosperous millennials the richest technology in historical past”, Knight Frank mentioned in its 18th annual wealth report.

That’s some huge cash that will likely be altering arms from child boomers to millennials within the many years forward.

Then there’s the forgotten technology — Gex X.1

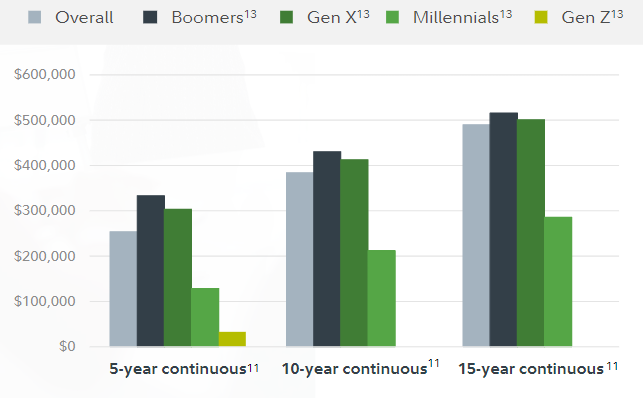

Right here’s an awesome stat about Gen X from the newest annual Constancy 401k replace:

The typical steadiness for Gen X staff who’ve been of their 401(okay) plan for 15 years straight topped half 1,000,000 {dollars} ($501,000) on the finish of 2023.

A very long time horizon wins once more!

It’s weird to assume a illness that unfold across the globe and utterly upended our lives in quite a few methods has by some means made generations of individuals wealthier than they’d have been if it by no means occurred.

Michael and I talked about all issues demographics and far more on this week’s Animal Spirits video:

Subscribe to The Compound so that you by no means miss an episode.

Additional Studying:

How Demographics Are Shaping the Housing Market

Now right here’s what I’ve been studying this week:

Books:

1If I’m being sincere I’m most likely extra Gen X than millennials. I used to be born in 1981 so I’ve a foot in each camps.

[ad_2]