{kind=link}

[ad_1]

I prefer to entertain severely views I disagree with, nevertheless it’s onerous to explain a brand new speculation on the left about the USA’ financial dynamism relative to Europe’s as something aside from “cockamamie.” The declare from Rogé Karma in The Atlantic is that “the US financial system is doing spectacularly effectively,” and the rationale for this efficiency is that America is “stealing from Europe’s big-government, welfare-state playbook.” By spending $5 trillion on pandemic reduction, however letting folks lose their jobs, so the argument goes, the US shuffled the labor market and bought folks into higher, extra productive jobs:

This labor-market reshuffling, argues Adam Posen, the president of the Peterson Institute for Worldwide Economics, is probably the most believable rationalization for why American employees skilled a sudden spike in productiveness within the second half of 2023 — one which didn’t happen in Europe. ‘The pandemic response satisfied folks that authorities finally had their again,’ Posen advised me. ‘And that allowed folks to take greater dangers than regular.’

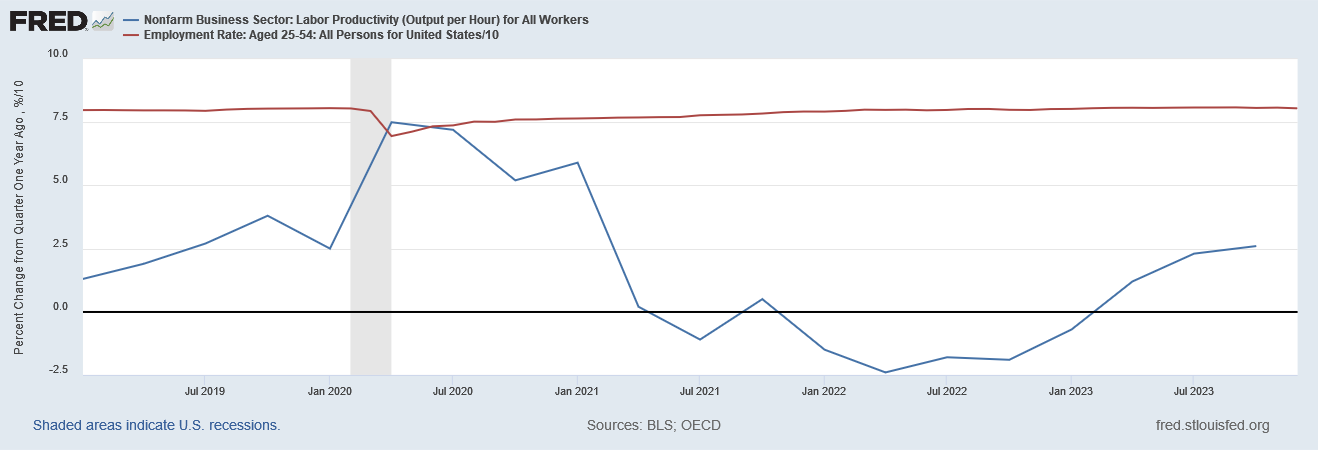

Let’s take a look at the proof. If this principle is true, then productiveness ought to have spiked simply after Individuals returned to work. The determine under plots p.c change over the earlier 12 months in actual output per hour, from the primary quarter of 2019 to the fourth quarter of 2023, alongside the prime-age employment fee. We do certainly see productiveness rising within the latter half of 2023.

However what’s occurring with the employment fee? It has recovered nearly all of its pandemic losses by March 2022. Complete quits additionally peaked in April 2022, implying that the job market reshuffling began slowing down then. It’s fairly arbitrary to attribute the productiveness development in 2023 to job reshuffling, when the latter course of was greater than 90 p.c full a 12 months and a half earlier than. Extra seemingly, falling inflation is the dominant motive productiveness grew in late 2023.

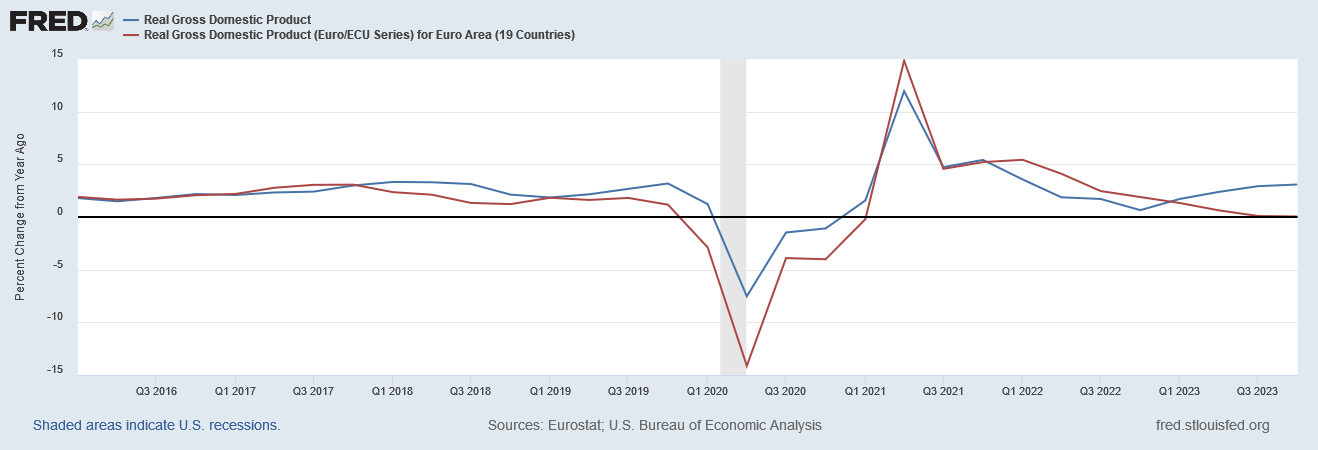

The opposite piece of proof that matches poorly with Karma’s declare is the truth that the US has been extra dynamic than Europe for a very long time. The determine under plots actual GDP development (proportion change from a 12 months in the past) for each the US and the Eurozone.

How can anybody take a look at these numbers and say that pandemic spending is what triggered the US to outpace Europe? From This autumn 2017 via Q1 2021 — 14 consecutive quarters — US development beat the Eurozone’s. Then, from Q2 2021 via This autumn 2022, with the only exception of two quarters, the Eurozone outpaced the US. Solely within the 4 quarters of 2023 has the US once more taken a lead on the Eurozone. A extra pure studying is that the US usually has greater development than the Eurozone, however one thing occurred in 2021 and 2022 to disrupt that normal sample. One might as simply make the case that giant federal deficits and inflation harm the US relative to Europe.

Taking a step again, it’s onerous for me to reconcile this new “social democratic” interpretation of the pandemic with the best way that social democrats have interpreted, effectively, nearly all the things else. They wish to say that mass unemployment was good this time as a result of it allowed folks to rapidly discover new jobs the place they have been extra productive. That sounds quite a bit just like the “liquidationist” perspective that influenced the Fed within the late Nineteen Twenties because it crushed the inventory market increase. Do Karma and Posen suppose that the Fed ought to be celebrated for having responded too late to the Nice Recession that hit in 2008? That we must always welcome an enormous monetary disaster from time to time? Was the Fed justified in letting the US slip into despair within the early Thirties?

Now, presumably, they might reply that mass unemployment is simply good if folks can get rehired rapidly, which wasn’t the case in the course of the Nice Melancholy, nor the Nice Recession. Nonetheless, the logic means that the employees could be higher off if authorities periodically inspired employers to fireside lots of their employees to assist “reshuffle” the labor market.

On theoretical grounds, the speculation makes little sense both. Do companies actually maintain round employees who’re making quite a bit lower than their marginal product for a very long time? Do folks actually quit on rising of their profession as soon as they’ve a job?

The brand new “reshuffling” thesis of American restoration doesn’t make a lot sense on the proof or financial principle. It serves a handy political objective in serving to to justify large federal stimulus that in any other case seems like a expensive waste, forward of an election, however that’s about all that may be mentioned for it.

For sources of American financial restoration, let’s look as an alternative on the belated restoration of macroeconomic stability, which has allowed America’s pure dynamism to come back via.

Jason Sorens

Jason Sorens, Ph.D., is Senior Analysis Fellow at AIER. He’s additionally Principal Investigator on the New Hampshire Zoning Atlas. Jason was previously the director of the Middle for Ethics in Society at Saint Anselm School. He has researched and written greater than 20 peer‐reviewed journal articles, a guide for McGill‐Queens College Press titled Secessionism, and a biennially revised guide for the Cato Institute, Freedom within the 50 States (with William Ruger).

His analysis is concentrated on housing coverage and land-use regulation, U.S. state politics, fiscal federalism, and actions for regional autonomy and independence around the globe. He has taught at Yale, Dartmouth, and the College at Buffalo and twice received awards for greatest instructing in his division. He lives in Amherst, New Hampshire.

[ad_2]