{kind=link}

[ad_1]

The latest period of worldwide commerce enlargement is over. Confronted with elevated geopolitical threat, fragile overseas provide chains, and uncertainties within the worldwide commerce surroundings, companies are suspending entry into overseas markets and pulling again from overseas actions (IMF 2023). Apart from its direct results on actual exercise, the latest rise in commerce uncertainty has probably essential implications for the monetary sector. This publish describes how the lending actions of U.S. banks have been affected by the rise in commerce uncertainty throughout the 2018-19 “commerce struggle.” Particularly, banks that have been extra uncovered to commerce uncertainty contracted lending to all of their home nonfinancial enterprise debtors, no matter whether or not these debtors have been dealing with excessive or low uncertainty themselves. Moreover, banks’ lending methods exhibited the kind of “wait-and-see” conduct normally present in company companies dealing with funding choices beneath uncertainty, and the lending contraction was bigger for these banks that have been extra financially constrained.

The 2018-19 Commerce Conflict and Banks’ Response to the Rise in Uncertainty

In a latest research, we study how commerce uncertainty impacts banks’ provide of credit score to their nonfinancial enterprise debtors. We deal with the rise in commerce uncertainty throughout the 2018-19 interval, colloquially known as the commerce struggle, which was marked by the renegotiation of commerce agreements between america and different international locations, in addition to modifications in tariffs, particularly for merchandise traded between america and China. Because the chart under exhibits, commerce uncertainty rose sharply initially of 2018.

The Rise in Commerce Uncertainty round U.S.–China Commerce Tensions

Supply: “Commerce Coverage Uncertainty Index” from Caldara et al. (2020).

Notes: The Commerce Coverage Uncertainty Index is derived from the variety of joint occurrences of “commerce coverage” and “uncertainty” in information articles of main world newspapers. The vertical line in 2018:Q1 marks the start of the “commerce struggle” interval of sustained excessive commerce uncertainty and enactment of a number of waves of tariffs.

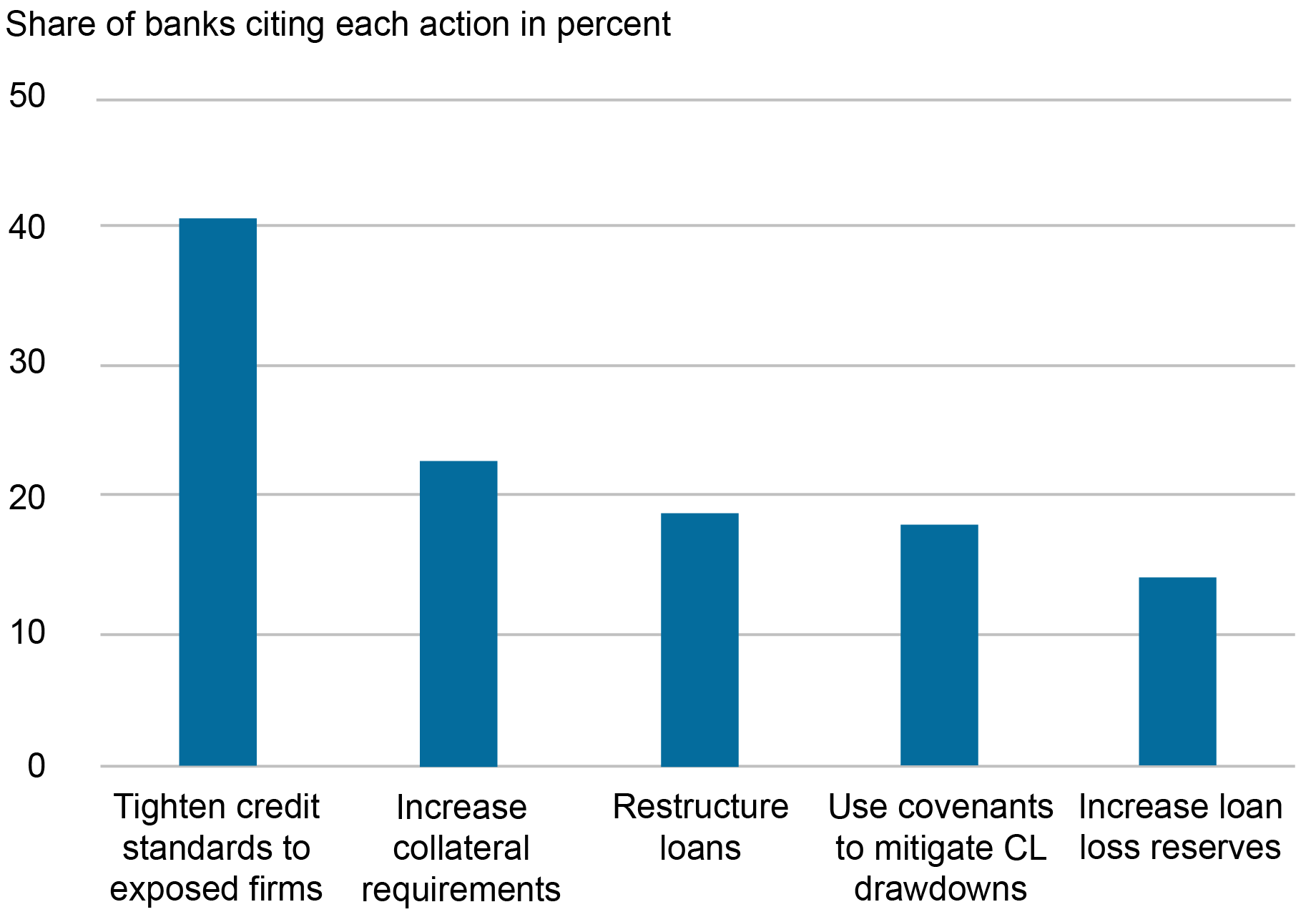

This episode didn’t go unnoticed by the banking sector. A survey of economic mortgage officers (the Senior Mortgage Officer Opinion Survey, or “SLOOS”) carried out by the Federal Reserve in April 2019 included questions aimed toward gauging the affect of commerce uncertainty on banks’ lending operations. Mortgage officers at about seventy banks have been requested what mitigating actions the banks had taken in response to hostile developments within the worldwide surroundings. The responses to those survey questions, tabulated within the chart under, recommend that the uncertainty prompted some banks to tighten lending requirements and enhance mortgage loss reserves. Some banks famous a notion that future mortgage losses would possibly enhance, with potential penalties for banks’ skill to intermediate credit score.

Financial institution Actions to Mitigate Commerce Dangers

Supply: Federal Reserve Senior Mortgage Officer Opinion Survey (SLOOS), April 2019.

How would possibly banks react to an increase in commerce uncertainty? They could reduce their publicity to companies affected by uncertainty—as they sometimes do when a few of their debtors are hit by adverse shocks—and supply further lending to different, much less affected, debtors. Alternatively, they could change into extra cautious total and, equally to nonfinancial companies, postpone investing in new tasks. Particularly, banks could postpone new lending or tighten their phrases—as an illustration, they could cut back approval charges on new loans, enhance mortgage spreads, shorten mortgage maturities, or require extra collateral on present loans.

How Did U.S. Banks Uncovered to Commerce Uncertainty Change Their Lending Conduct throughout the Commerce Conflict?

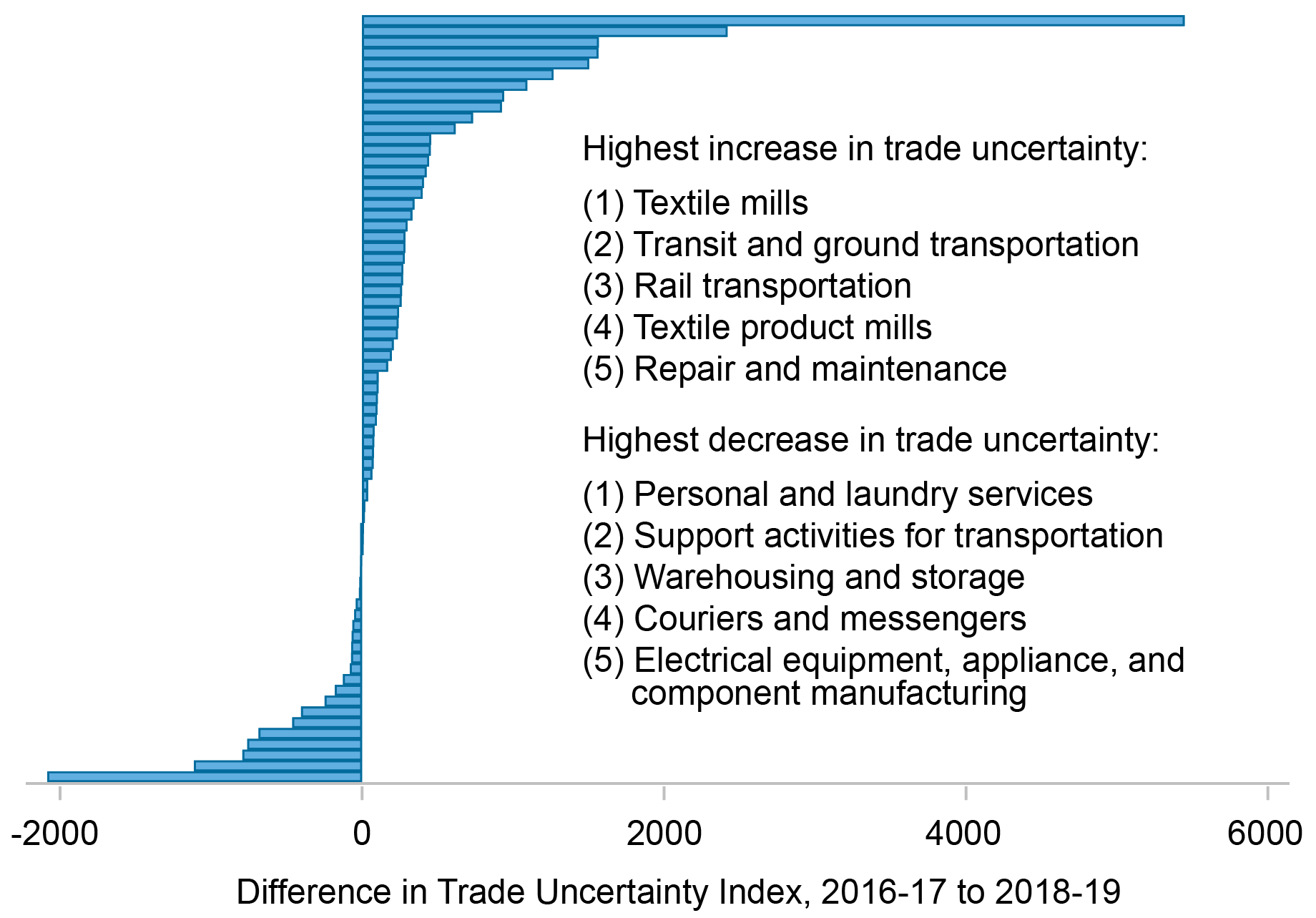

To estimate the affect of commerce uncertainty on financial institution lending, we assemble a novel measure of financial institution publicity to commerce uncertainty by combining firm-level info on commerce uncertainty with detailed knowledge on U.S. banks’ mortgage exposures to home debtors previous to the commerce struggle (sourced from the U.S. Y-14Q “credit score register” knowledge, which primarily comprise knowledge on giant banks). The measure captures a financial institution’s ex ante publicity to the realized rise in commerce uncertainty throughout the 2018-19 interval. As the following chart exhibits, the commerce struggle generated variations in commerce uncertainty throughout sectors of the U.S. financial system, with a number of manufacturing and transportation-related sectors experiencing the most important will increase in uncertainty. Due to this fact, banks with bigger ex ante publicity to debtors that function in excessive commerce uncertainty sectors had bigger exposures to commerce uncertainty of their total mortgage portfolio.

Change in Sectoral Commerce Uncertainty between 2016-17 and 2018-19

Supply: Authors’ calculations based mostly on knowledge from Hassan et al. (2019).

Notes: Non-financial sectors are listed in descending order of uncertainty. Values are calculated by averaging Hassan et al. (2019)’s firm-level commerce uncertainty knowledge, based mostly on textual evaluation of earnings name transcripts, throughout companies inside three-digit NAICS sectors.

Combining the bank-level publicity to commerce uncertainty with quarterly mortgage development charges on the financial institution–agency stage, we estimate panel regressions over 2016-19 and present that banks uncovered to commerce uncertainty contracted lending throughout the commerce struggle interval (2018-19) relative to the previous interval (2016-17). Banks extra uncovered to commerce uncertainty additionally elevated rates of interest on new loans. Importantly, these outcomes maintain for all debtors and for debtors in sectors not as immediately affected by commerce uncertainty. Thus, banks uncovered to commerce uncertainty don’t seem to distinguish throughout debtors of their lending conduct. As a substitute, banks dealing with an increase in uncertainty undertake a wait-and-see strategy by contracting credit score for all debtors.

The impact of commerce uncertainty on financial institution lending that we determine is economically significant. A one normal deviation enhance in financial institution publicity to commerce uncertainty is related to a 2.6 proportion level decline in mortgage development on the financial institution–agency pair stage (in comparison with 0 p.c median mortgage development for the pattern) and a rise in rates of interest of 6.5 foundation factors (in comparison with a 185 foundation level median mortgage unfold for the pattern).

The mechanisms underlying banks’ reactions to elevated commerce uncertainty are in keeping with real-options idea, which predicts that companies postpone funding within the face of uncertainty. Extra-exposed banks cut back the maturity of loans and shift towards forms of loans that may be known as in early (so-called demandable loans). Furthermore, on condition that they anticipate a wider dispersion in mortgage returns and will have difficulties forecasting revenues and capital wants, uncovered banks downgrade the perceived creditworthiness of companies, as mirrored within the greater chances of default that they assess for these companies. Uncovered banks additionally contract their lending extra strongly to companies which might be perceived as prone to be adversely affected by the commerce struggle and therefore riskier ex ante—specifically these companies in manufacturing sectors that obtain low import safety and people companies in sectors with excessive import dependence.

One other rationalization for banks’ pullback from risk-taking amid greater uncertainty is a “monetary constraints” channel that emphasizes the position of capital constraints confronted by banks. Uncovered banks with decrease ranges of capital ought to be much less capable of stand up to mortgage losses, could expertise a rise in funding prices, and will thus contract their lending by greater than different banks. Certainly, banks with decrease ranges of regulatory capital on the time of the commerce struggle or beneath hostile stress-test eventualities in the reduction of the provision of loans—to all debtors—greater than different banks. Per each mechanisms, uncovered banks have decrease tolerance for risk-taking as they rebalance portfolios away from industrial loans and into safer belongings, notably securities.

What Are the Implications for Financial Exercise?

The contraction in financial institution credit score provide arising from commerce uncertainty could affect exercise in the actual sector, particularly for bank-dependent companies. We use lending relationships earlier than the commerce struggle to assemble a measure of companies’ publicity to commerce uncertainty by way of their relationship with uncovered banks. We then relate this measure to companies’ future funding and leverage. Extra-exposed companies are discovered to be unable to substitute for decreased financial institution lending via different sources of finance and exhibit comparatively decrease complete debt development and funding charges. A one normal deviation enhance in companies’ publicity to commerce uncertainty is related to an economically significant lower within the development fee of the companies’ complete debt and of their funding fee in 2018–19 by 2.4 and a pair of.7 proportion factors, respectively. These outcomes are in keeping with credit score provide contraction having a fabric hostile impact on uncovered companies’ actual outcomes. Furthermore, personal companies—which usually tend to rely upon financial institution financing—and companies with a better share of financial institution debt expertise comparatively worse actual outcomes.

Total, our research confirms that banks are a conduit for amplifying the results of commerce uncertainty. This monetary channel is contractionary for a broad spectrum of companies, not completely these in sectors immediately uncovered to the commerce struggle.

Ricardo Correa is a senior adviser within the Division of Worldwide Finance on the Federal Reserve Board.

Julian di Giovanni is the pinnacle of Local weather Threat Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Linda S. Goldberg is a monetary analysis advisor for Monetary Intermediation Coverage Analysis within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Camelia Minoiu is a analysis economist and adviser on the monetary markets staff within the Federal Reserve Financial institution of Atlanta’s Analysis Division.

Easy methods to cite this publish:

Ricardo Correa, Julian di Giovanni, Linda S. Goldberg, and Camelia Minoiu, “Does Commerce Uncertainty Have an effect on Financial institution Lending?,” Federal Reserve Financial institution of New York Liberty Avenue Economics, December 20, 2023, https://libertystreeteconomics.newyorkfed.org/2023/12/does-trade-uncertainty-affect-bank-lending/.

Disclaimer

The views expressed on this publish are these of the creator(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the creator(s).

[ad_2]