[ad_1]

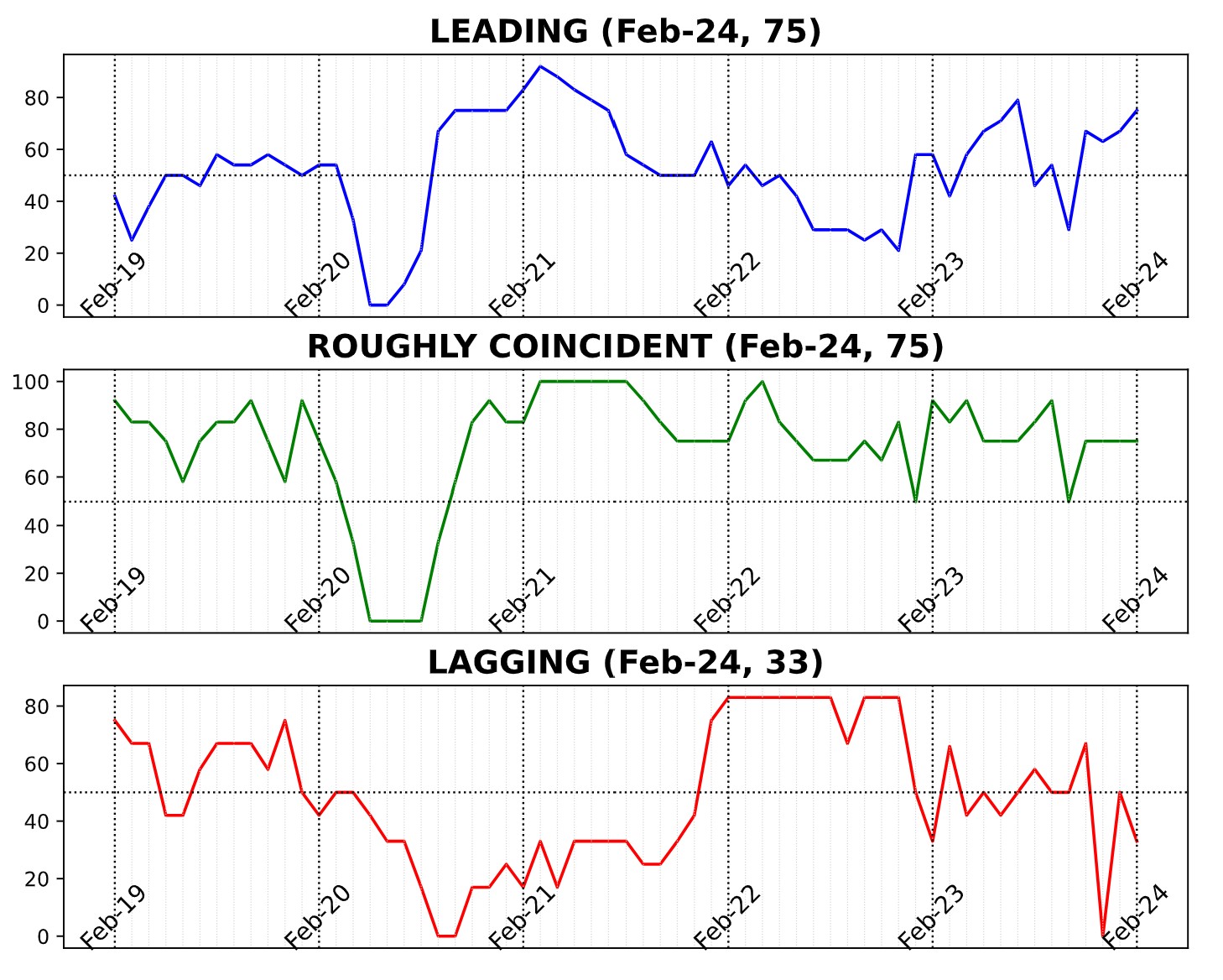

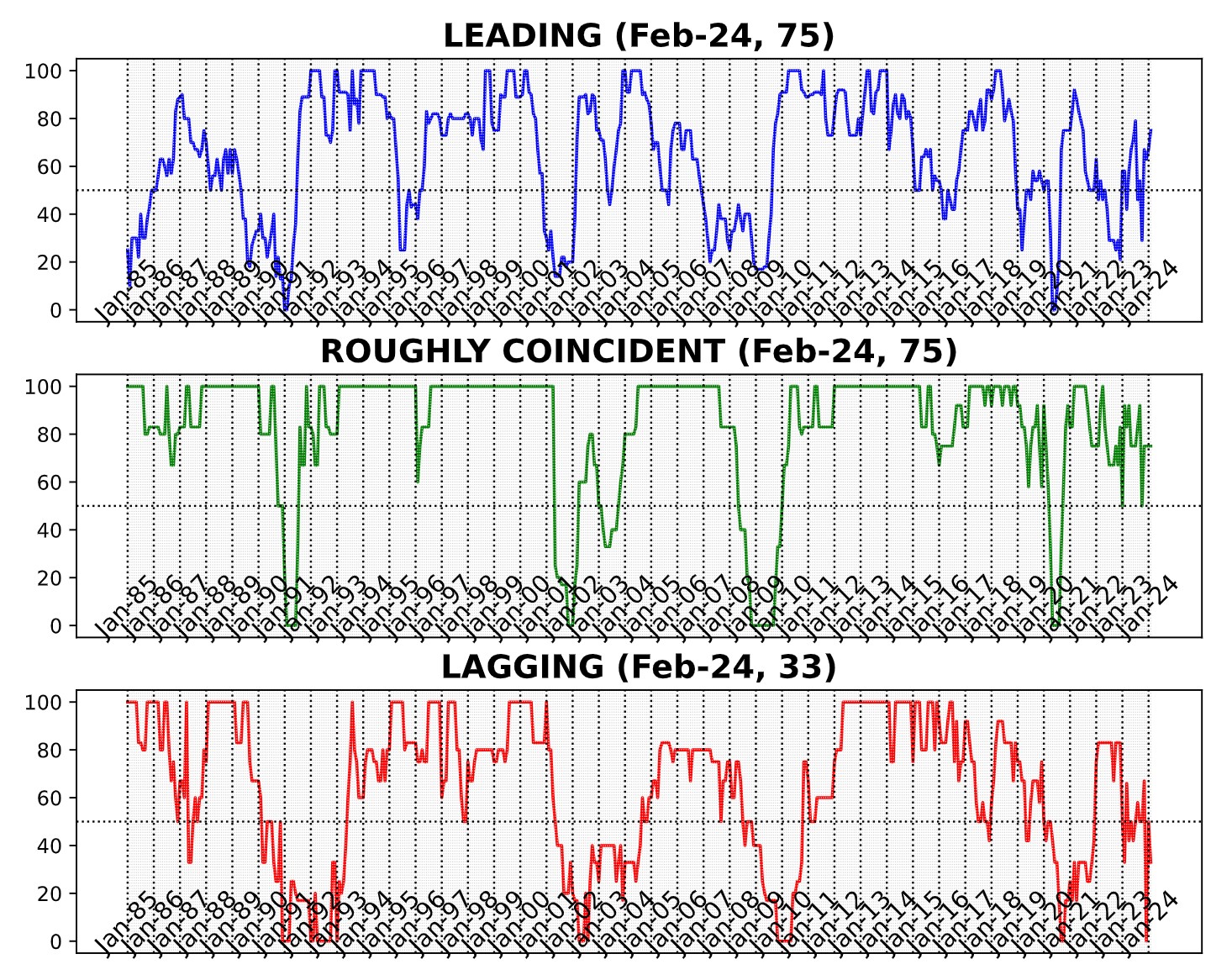

In February 2023, the AIER Enterprise Situations Month-to-month demonstrated divergent alerts but once more. The Main Indicator rose from 67 to 75 with the Roughly Coincident Indicator spending a fourth month on the 75 degree. The Lagging Indicator, which dropped to 0 in December 2023 earlier than rebounding to 50 in January fell again once more to 33.

{kind=link}

Main Indicator (75)

Among the many twelve parts of the Main Indicator, seven rose and 5 declined.

Rising in February 2023 had been the US New Privately Owned Housing Models Began by Construction Whole SAAR (12.7 p.c), FINRA Buyer Debit Balances in Margin Accounts (5.9 p.c), Convention Board US Main Index Inventory Costs 500 Frequent Shares (4.3 p.c), Adjusted Retail & Meals Providers Gross sales Whole SA (0.9 p.c), Convention Board US Producers New Orders Nondefense Capital Good Ex Plane (0.6 p.c), US Common Weekly Hours All Staff Manufacturing (0.5 p.c), and the Convention Board US Main Index Manuf New Orders Client Items & Supplies (0.1 p.c). The 5 declining parts had been the Stock/Gross sales Ratio: Whole Enterprise (-0.7 p.c), United States Heavy Vehicles Gross sales SAAR (-1.6 p.c), College of Michigan Client Expectations Index (-2.5 p.c), US Preliminary Jobless Claims (-5.3 p.c), and the 1-to-10 yr US Treasury unfold (-6.4 p.c).

The Main Indicator, at 75, suggests a sustained degree of average progress, sustaining a constant pattern inside the vary of above-neutral efficiency noticed over the previous yr.

Roughly Coincident (75) and Lagging Indicators (33)

Among the many six constituents of the Roughly Coincident indicator 4 rose, one was impartial, and one declined in February. US Industrial Manufacturing (0.4 p.c), Convention Board Coincident Private Earnings Much less Switch Funds (0.2 p.c), Convention Board Coincident Manufacturing and Commerce Gross sales (0.2 p.c), and US Staff on Nonfarm Payrolls (0.2 p.c) rose. The US Labor Power Participation Price was unchanged, and the Convention Board Client Confidence Current Scenario SA 1985=100 declined 4.8 p.c.

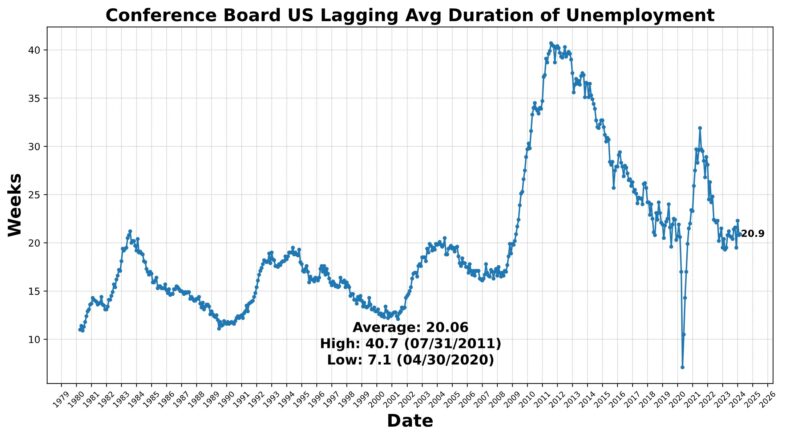

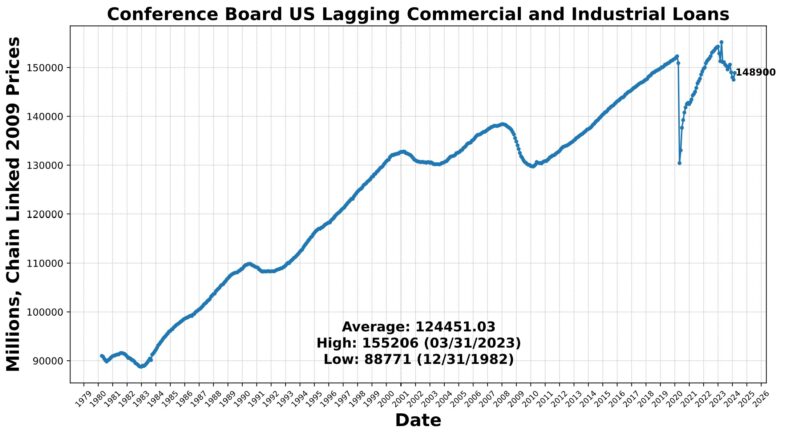

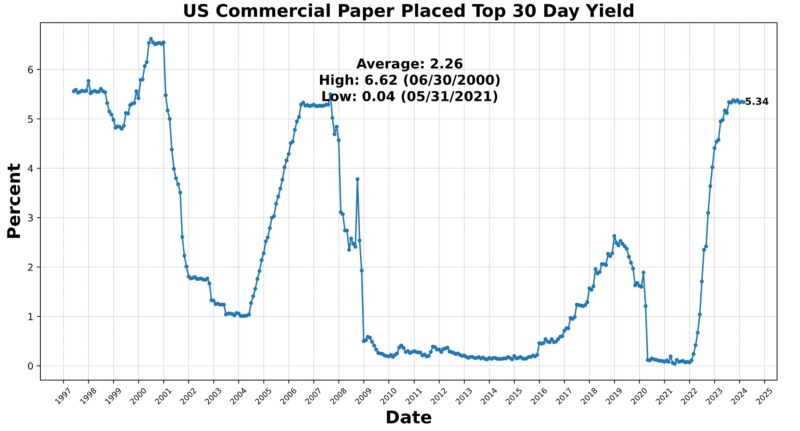

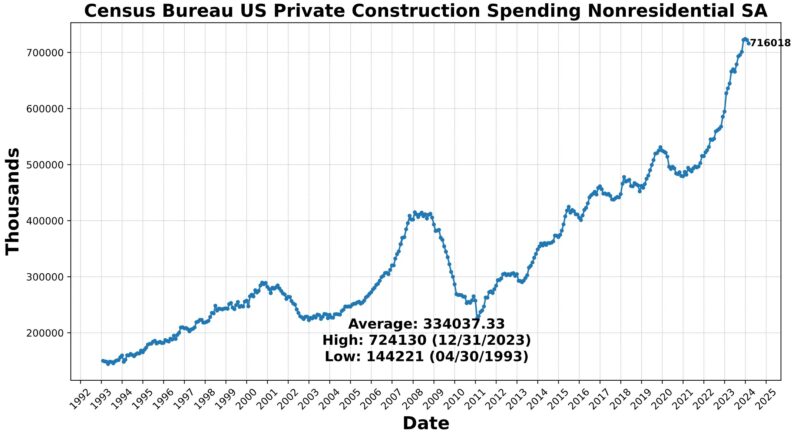

The Lagging Indicator had three rising and three falling parts. Within the first class had been the Convention Board US Lagging Business and Industrial Loans (0.9 p.c), Convention Board US Lagging Avg Period of Unemployment (0.5 p.c), and US Manufacturing & Commerce Inventories Whole (0.5 p.c). US Business Paper Positioned High 30 Day Yield fell 0.2 p.c, as did Census Bureau US Non-public Constructions Spending Nonresidential (-0.9 p.c) and US CPI City Customers Much less Meals & Power year-over-year (-2.7 percentAt the 75 degree for 4 months now, the Roughly Coincident Indicator suggests relative stability of average progress. In distinction, the Lagging Indicator suggests average contraction, persevering with a sample of sizable fluctuations from month to month.

Dialogue

The discharge of the Fed’s Beige Ebook on April 17, 2024, supplied insights into financial situations throughout numerous areas of the US. The primary quarter of 2024 was characterised by a “slight” growth, aligning with earlier downbeat descriptions of exercise. Ten Federal Reserve districts reported progress in comparison with eight in February, though client spending confirmed a minimal improve, which contrasts with latest retail gross sales figures. Amongst different traits famous had been growing worth sensitivity and decreased discretionary spending. Respondents to Fed surveys expressed cautious optimism about progress, though employment progress remained modest with ongoing labor shortages in sure sectors. Wage pressures continued to ease, whereas inflation remained regular, although some districts reported growing stress on margins on account of problem in passing on worth will increase, posing potential upside dangers.

The March industrial manufacturing report introduced an upside shock, exceeding preliminary expectations. Manufacturing manufacturing, specifically, confirmed surprising energy, with February’s information revised upward, setting the next base for measuring month-to-month progress. The surge in manufacturing was fueled by sturdy client demand for vehicles, historically an interest-sensitive sector, in addition to gas. With client demand resilient and survey information indicating strengthening situations, it could be the case that US industrial manufacturing has surpassed its earlier trough. Not solely did deadline industrial manufacturing develop in March, aligning with consensus and expectations, however February’s figures had been revised up considerably from 0.1 p.c to 0.4 p.c. Notably, manufacturing manufacturing outperformed forecasts, rising by 0.5 p.c in the course of the month, exceeding each survey expectations and consensus estimates. The rise in client items manufacturing, significantly in vehicles and elements, contributed considerably to this progress. Sturdy-goods manufacturing and manufacturing of nondurable items additionally made substantial contributions to month-to-month industrial-production progress.

The employment panorama depicted by the Bureau of Labor Statistics’ institution survey (which polls roughly 144,000 companies) and family survey (which surveys roughly 60,000 households) have diverged considerably of late, revealing contrasting financial realities. Sectors buoyed by spending from asset-appreciation beneficiaries (leisure, hospitality, and healthcare, amongst others) are exhibiting sturdy employment positive aspects whereas different sectors are witnessing decreased demand. The latter are usually related to lower-income shoppers, and are experiencing slowing progress and hiring limitations. This disparity is more likely to persist, exacerbating difficulties in interpretation.

Current energy in nonfarm payrolls information has outpaced expectations, averaging round 250,000 new jobs monthly. That is greater than twice the Federal Reserve’s estimated regular state tempo of 100,000 monthly. A prevailing idea attributes that sturdy progress to the unimaginable surge in immigration over the previous few years, suggesting {that a} new, greater impartial hiring tempo of from 150,000 to 250,000 monthly.

But there’s trigger for skepticism relating to the accuracy of nonfarm payrolls in capturing undocumented staff. The family survey probably affords a extra correct reflection of labor market well being than the institution survey does. Regardless of the consensus view, the family survey signifies a cooling labor market, difficult the notion of continued sturdy hiring amidst an inflow of migrants. Methodological variations between the institution and family surveys underpin the discrepancy, with the family survey simpler in recording the employment of probably undocumented staff. Whereas the institution survey captures jobs extra liable to pro-cyclical fluctuations – resembling short-term positions and “gig financial system” work – the family survey gives a extra complete image of labor market dynamics.

Consequently, policymakers might have to recalibrate their evaluation of the financial system’s capability to soak up a big inflow of low-skilled migrants amidst mounting labor market slack. Current coverage modifications, resembling California’s important minimal wage hike are moreover impacting employment dynamics, exacerbating the softening within the labor market. Regardless of the energy in nonfarm payrolls, family survey information recommend weaker employment positive aspects, reflecting a cooling labor market.

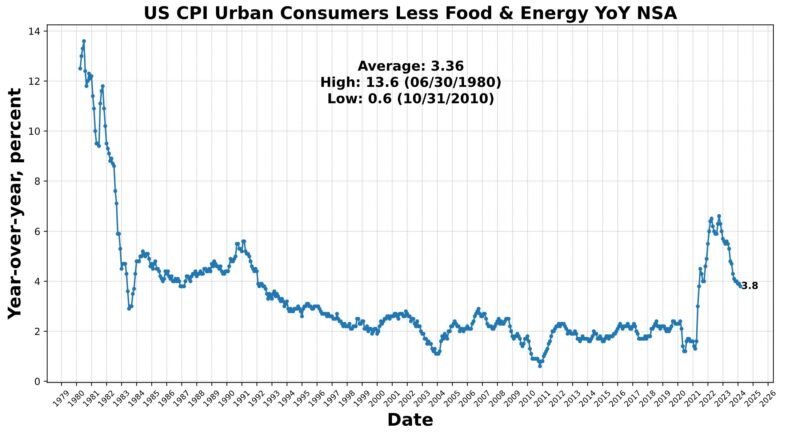

The March’s Client Value Index (CPI) information introduced a regarding sign for the continued struggle in opposition to inflation, particularly contemplating the favorable seasonal patterns usually conducive to disinflation throughout this era. Each headline and core CPI remained unchanged from February, with year-over-year figures ticking up barely. Of explicit be aware is the persistent momentum in core CPI on numerous timescales, indicating that progress on disinflation might have stalled or successfully stopped. Notably, vitality costs and shelter prices proceed to be main drivers of inflation, with gasoline costs and rents contributing considerably to headline CPI progress. Moreover, core providers, significantly transportation providers, are experiencing notable inflationary pressures reflective of the lingering results of worth will increase in new and used automobiles.

Regardless of some encouraging indicators of disinflation in sure classes, resembling core items, the diffusion of disinflation stays uneven. Financial coverage’s effectiveness in curbing inflationary pressures seems to be enhancing, as evidenced by declining worth pressures in some interest-sensitive spending classes. Nevertheless, the share of core spending classes experiencing outright deflation stays comparatively excessive, indicating ongoing challenges in attaining broad-based disinflation.

In gentle of those developments, and evidenced by statements made by Fed officers in latest weeks, policymakers are reassessing their inflation outlook and the ensuing coverage trajectory. It’s fairly probably that the Fed’s timeline for fee changes shall be delayed. Market-implied coverage fee markets, which late in 2023 predicted 5 – 6 fee cuts in 2024 have downgraded their forecast to 2.

Amidst combined financial information harking back to many of the previous two years, there are pockets of energy that are nonetheless overshadowed by inflation considerations and hypothesis relating to financial coverage actions within the coming quarter or two. Labor markets are cooling, including to the uncertainty surrounding the trajectory of the US financial system. Notably, each the spot worth of gold and the S&P 500 have reached document highs in shut succession on a number of events previously month, handily reflecting market-expressed uncertainty concerning the financial outlook. Whereas the probability of a pronounced financial contraction appears to be diminishing, traditional indicators of recession proceed to strongly sign a downturn inside the subsequent 12 months. The absence of a discernible path recommends objectively presenting factual information and traits devoid of bias or prognostication.

LEADING INDICATORS

ROUGHLY COINCIDENT INDICATORS

LAGGING INDICATORS

CAPITAL MARKET PERFORMANCE

Peter C. Earle

Peter C. Earle, Ph.D, is a Senior Analysis Fellow who joined AIER in 2018. He holds a Ph.D in Economics from l’Universite d’Angers, an MA in Utilized Economics from American College, an MBA (Finance), and a BS in Engineering from the US Army Academy at West Level.

Previous to becoming a member of AIER, Dr. Earle spent over 20 years as a dealer and analyst at various securities companies and hedge funds within the New York metropolitan space in addition to participating in intensive consulting inside the cryptocurrency and gaming sectors. His analysis focuses on monetary markets, financial coverage, macroeconomic forecasting, and issues in financial measurement. He has been quoted by the Wall Road Journal, the Monetary Instances, Barron’s, Bloomberg, Reuters, CNBC, Grant’s Curiosity Price Observer, NPR, and in quite a few different media retailers and publications.

[ad_2]