{kind=link}

[ad_1]

As proven in a previous Liberty Avenue Economics publish, in the USA, the yields of cash market fund (MMF) shares reply to adjustments in financial coverage charges way more than the charges of financial institution deposits; in different phrases, the MMF beta is way increased than the deposit beta. In keeping with this, the scale of the U.S. MMF trade fluctuates over the rate of interest cycle, increasing throughout instances of financial coverage tightening. On this publish, we present that the connection between the coverage charges of the European Central Financial institution (ECB) and the scale of European MMFs investing in euro-denominated securities can be optimistic—so long as coverage charges are optimistic; after the ECB launched detrimental coverage charges in 2015, that relationship broke down, as MMFs obtained massive inflows throughout this era.

European MMFs

MMFs are a kind of open-end mutual fund that put money into short-term money-market devices with low credit score danger. As a result of nature of their investments, MMFs are money-like devices that present traders with returns near present money-market charges. Just like their U.S. counterparts, European MMFs will be divided into authorities funds (normally referred to as “public debt funds”) and prime funds based mostly on their portfolio holdings: authorities MMFs primarily put money into debt securities issued by the general public sector or repurchase agreements (repos) collateralized by such securities, whereas prime MMFs may put money into uncollateralized debt securities issued by the personal sector. European MMFs are regulated below Regulation (EU) 2017/1131 of the European Parliament and of the Council of the European Union (EU), which was adopted in 2017 in response to the 2008 run skilled by MMFs.

On this publish, we give attention to “euro-denominated MMFs”—that’s, European MMFs investing in euro-denominated securities. The scale of this trade is way smaller than its U.S. equal: in July 2023, euro-denominated MMFs managed $0.72 trillion (€0.65 trillion) in belongings; as compared, U.S. MMFs managed $6 trillion (€5.4 trillion). The composition of the trade can be totally different: euro-denominated MMFs are primarily prime funds with variable internet asset worth (NAV), with authorities funds (working with a continuing NAV) representing lower than 1 p.c of the trade; in distinction, within the U.S., authorities MMFs make up 78 p.c of the trade.

The Beta on European MMFs

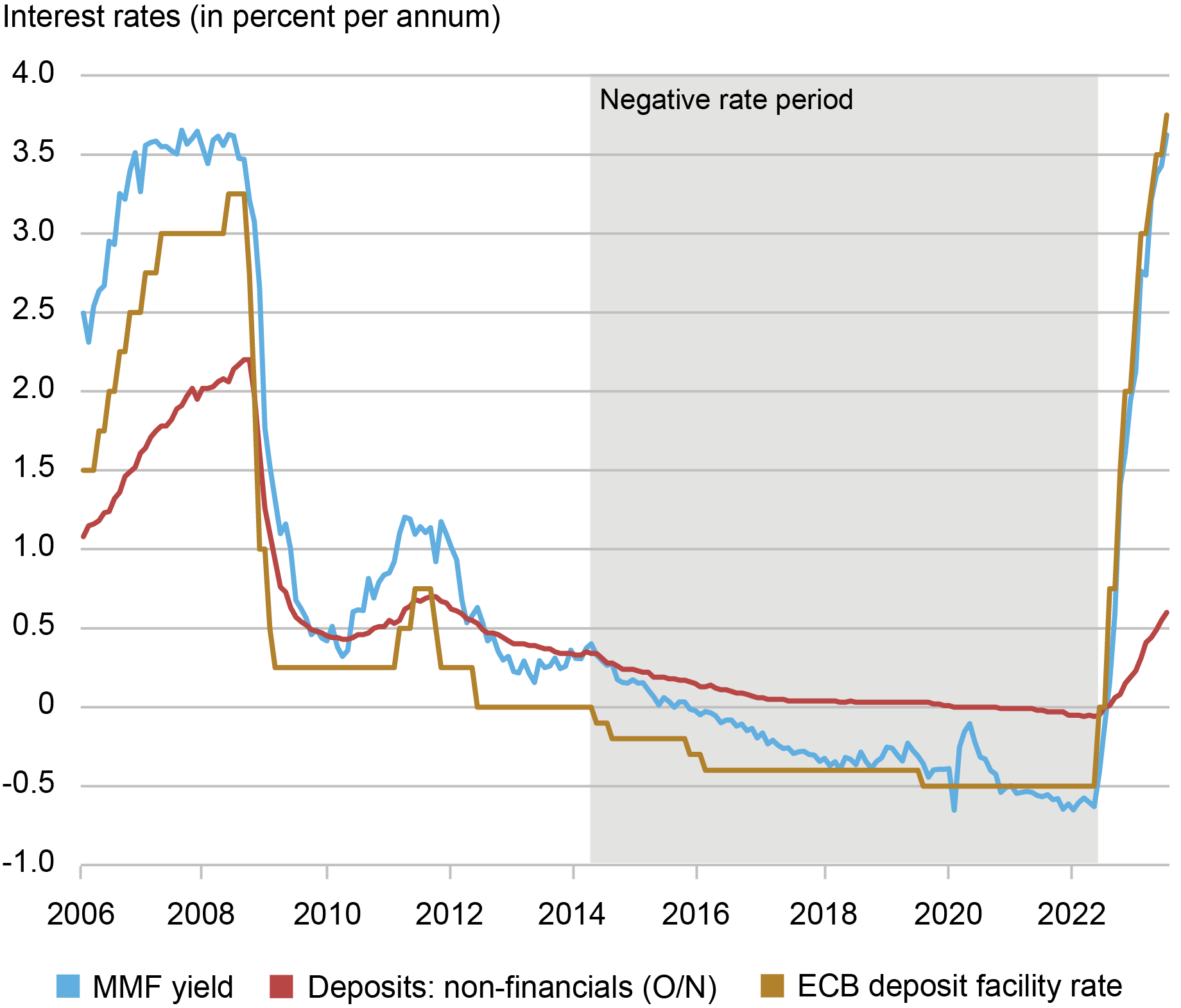

As within the U.S. market, the beta of euro-denominated MMFs is way increased than that of EU financial institution deposits; in different phrases, MMF yields monitor the coverage charge extra intently than financial institution deposit charges do. The chart beneath exhibits the charges on a number of euro-denominated money-market devices between 2006 and 2023: 1) the typical yield on euro-denominated MMFs (blue line); 2) the rate of interest on in a single day financial institution deposits of nonfinancial corporations (crimson line); and three) the ECB’s deposit facility charge (DFR, gold line), which is the speed banks earn on their in a single day deposits on the ECB (and the ECB’s key coverage charge).

Because the chart beneath exhibits, in a single day EU deposit charges transfer slowly, with a low beta, just like what we observe for U.S. deposits: particularly, the EU deposit charge elevated by simply 1 proportion level (pp) throughout 2006-07, whereas the ECB’s DFR was raised by 1.5 pp throughout the identical interval. Through the newest tightening cycle, the distinction has been much more stark: whereas the DFR was raised by 4 pp throughout 2022-23, the deposit charge elevated by 0.6 pp throughout the identical interval. Furthermore, whereas the DFR reached detrimental territory in June 2014, the deposit charge solely went beneath zero in 2021.

MMF Yields Transfer Intently with the ECB Coverage Price

Supply: ECB Knowledge Portal and Morningstar Direct

In distinction, the typical yield of euro-denominated MMFs follows the DFR way more tightly, growing sharply through the transient mountain climbing cycle in 2011 in addition to within the newest mountain climbing cycle initiated in 2022. Certainly, the yield on MMF shares turns into detrimental in December 2015, following the ECB’s adoption of a detrimental rate of interest coverage in June 2014. In different phrases, regardless of the delayed arrival of detrimental MMF yields, the beta on euro-denominated MMFs is way increased than that on financial institution deposits, just like the U.S. expertise.

Financial Coverage and the Measurement of the European MMF Business

As documented in a previous publish, the scale of the U.S. MMF trade strikes along with the financial coverage cycle. When charges improve, U.S. MMFs develop in dimension, after which shrink when the Federal Reserve eases financial coverage. This sample was evident through the cycle, for instance: the belongings managed by U.S. MMFs elevated by $1 trillion between 2022:Q2 and 2023:Q3, reaching over $6 trillion. The optimistic relationship between the Fed’s financial coverage stance and the scale of the MMF trade is in step with traders leaving financial institution deposits for MMF shares due to their considerably increased beta in a rising charge surroundings.

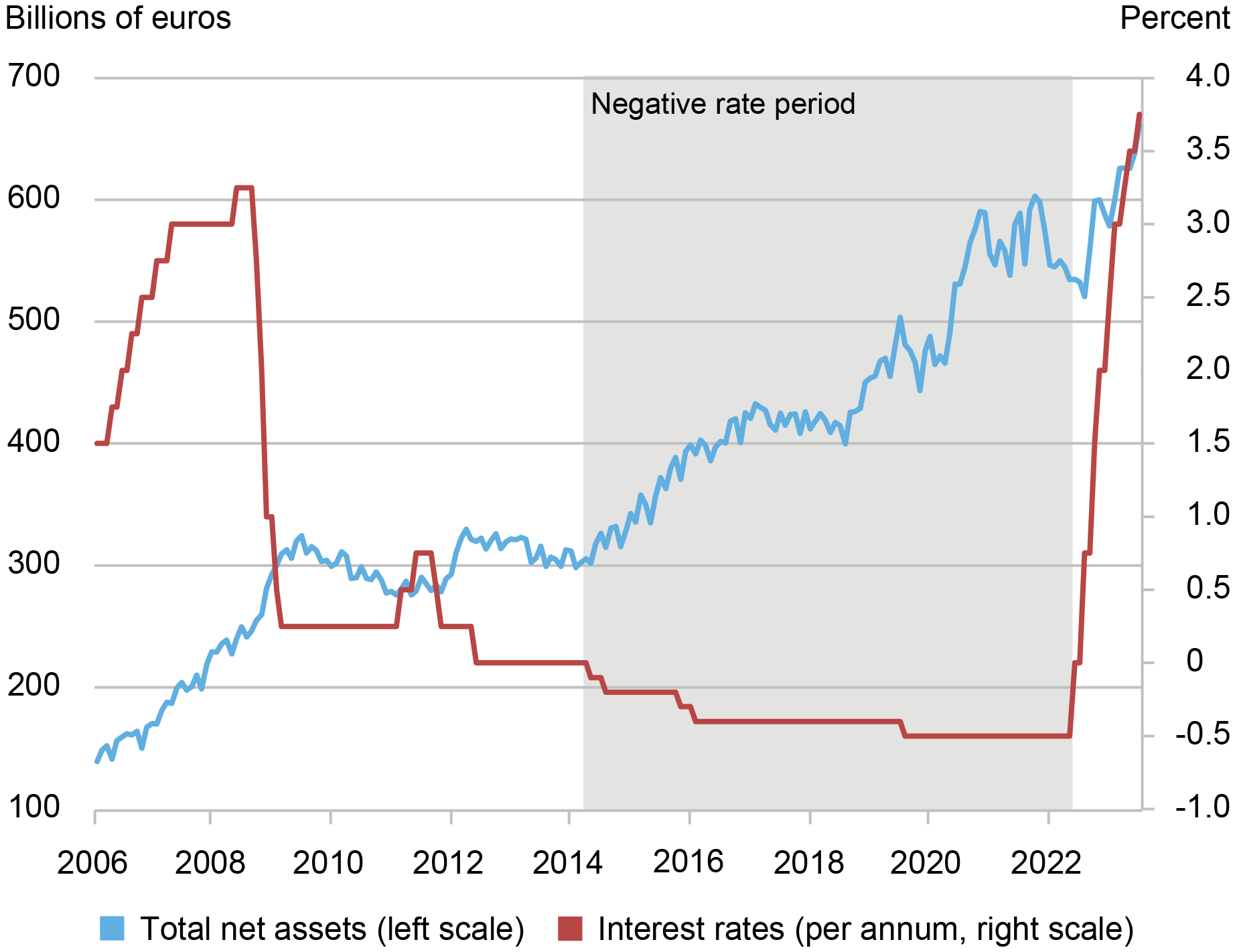

An analogous optimistic relationship existed between the ECB’s coverage stance and the scale of euro-denominated MMFs through the tightening-and-easing cycles of 2006-12. The connection, nevertheless, broke down through the interval of detrimental rates of interest.

The chart beneath exhibits the entire internet belongings managed by euro-denominated MMFs, together with the DFR. Particularly, regardless of coverage charges falling into detrimental territory, European MMFs obtained substantial inflows from 2015 onwards. That is in stark distinction to the standard optimistic relationship between rates of interest and the scale of the MMF sector. The expansion in MMF belongings was significantly pushed by institutional-oriented MMFs, which grew by €43 billion (34 p.c) between June 2014 and June 2016—in comparison with a rise of €27 billion (14 p.c) for retail-oriented MMFs. Because the ECB additional minimize rates of interest in September 2019, MMFs continued to expertise important inflows, regardless of offering detrimental yields.

One motive for the conduct of institutional traders may need been the relative attractiveness of MMF yields in comparison with different wholesale money-market charges obtainable to institutional traders. For instance, the Euro In a single day Index Common (EONIA) and the Euro Quick-Time period Price (€STR), which measure the price of wholesale unsecured in a single day borrowing in euros for banks situated within the euro space, have been even decrease than the yields provided by euro-denominated MMFs through the interval of detrimental charges. In different phrases, in distinction to retail deposit charges, charges provided to institutional traders proceed to intently observe the coverage charge as soon as it turns detrimental, and MMF yields can stay engaging relative to them

Euro-Denominated MMF Business Grew at the same time as ECB Coverage Price Grew to become Unfavorable

Supply: ECB Knowledge Portal and MorningstarDirect

The scale of the euro-denominated MMF trade stabilized in 2021, hovering round €570 billion. The standard optimistic relationship between coverage charges and MMF flows re-emerged after the onset of the ECB’s newest mountain climbing cycle in July 2022. Between June 2022 and August 2023, euro denominated MMFs grew by greater than €100 billion, reflecting each the upper coverage charge and the actual attractiveness of short-term funding autos in an inverted yield curve surroundings.

Summing Up

This publish paperwork that, just like the final sample in the USA, the yields on European MMF shares show a a lot tighter relationship with financial coverage in comparison with financial institution deposit charges. In step with the observations within the U.S. market, such a excessive beta on MMF shares implies that the scale of the European MMF trade normally will increase when coverage charges improve. Through the introduction of detrimental coverage charges, nevertheless, this optimistic relationship broke down: detrimental charges have been related to inflows into euro-denominated MMFs, as MMF yields remained aggressive with respect to different short-term funding autos provided to institutional traders. Through the ECB’s current tightening cycle, the optimistic relationship between the ECB’s financial coverage stance and the scale of the euro-denominated MMF sector re-emerged.

Marco Cipriani is the pinnacle of Cash and Funds Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Daniel Fricke is a analysis economist on the Deutsche Bundesbank.

Stefan Greppmair is a analysis economist on the Deutsche Bundesbank

Gabriele La Spada is a monetary analysis advisor in Cash and Funds Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Karol Paludkiewicz is a senior analysis economist and deputy head of the Monetary Markets Analysis Part on the Deutsche Bundesbank.

The right way to cite this publish:

Marco Cipriani, Daniel Fricke, Stefan Greppmair, Gabriele La Spada, and Karol Paludkiewicz, “Financial Coverage and Cash Market Funds in Europe,” Federal Reserve Financial institution of New York Liberty Avenue Economics, April 11, 2024, https://libertystreeteconomics.newyorkfed.org/2024/04/monetary-policy-and-money-market-funds-in-europe/.

Disclaimer

The views expressed on this publish are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York, the Federal Reserve System, the Deutsche Bundesbank, or the Eurosystem. Any errors or omissions are the duty of the writer(s).

[ad_2]