{kind=link}

[ad_1]

Yesterday, the Financial institution of Japan elevated its coverage goal fee for the primary time in 17 odd years and it set the noise degree among the many commentariat off the charts – ‘lastly, they’ve bowed to the strain from the monetary markets’, ‘main tightening’, ‘scraps radical coverage’, and many others – all of the hysteria. The fact is sort of totally different as they moved the goal from -0.1 per cent to 0 per cent – no main shift, only a modest variation after higher than anticipated – Shuntō outcomes for staff, which can lastly sign that the deflationary mindset amongst staff and corporations is coming to an finish. Nevertheless, to suppose that the Financial institution of Japan has simply radically modified its tune is naive and never in keeping with the info. After analysing the Japanese scenario we have now some good music right now – given it’s Wednesday.

Financial institution of Japan makes a minor adjustment

Commerce unions in Japan are organised by enterprise quite than sector, which might usually make it arduous to get coordinated wage outcomes for staff.

The height physique of the union motion solved that drawback manner again in 1954 when it proposed coordinated annual wage will increase for many staff and corporations.

The so-called ‘spring wage offensive’ or – Shuntō – is carried out in February and March every year and it’s a supply of stability within the industrial relations system in Japan.

This text from the Japanese Middle for Financial Analysis – Historical past of Shunto and Its Financial Significance (October 17, 2023) – gives a number of details about the method if you’re curious about studying extra.

Whereas the negotiations begin with the bigger unions in bigger enterprises the ultimate outcomes unfold to SMEs which would not have robust union organisation and make up the vast majority of the workforce

Because the property crash in 1991, unions have misplaced protection and the capability to achieve wage will increase by the shuntō has decreased.

Till lately, unions have been on the again foot.

Nevertheless, with authorities help lately, who noticed the one manner out of the deflationary mindset was by stronger wage outcomes, the unions had been extra profitable and the shuntō course of has regained effectiveness.

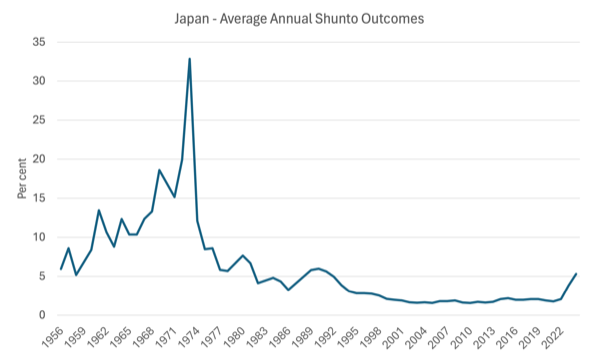

Listed below are the typical annual outcomes since 1956 (annual proportion rises).

After the distruption arising from the OPEC oil worth hikes within the Seventies, nominal wage outcomes grew to become very modest within the Nineties after the property bubble burst in 1991.

With inflation rising lately coupled with authorities help, the shuntō is lastly delivering stronger nominal wages progress.

And right here is the actual wage equivalents of these common annual wage rises for the reason that property bubble burst in 1990.

In 2023, the typical annual wage final result from the spring wage offensive was 3.8 per cent, which delivered very small actual buying energy will increase to staff, given the inflation fee of round 3.3 per cent

The present estimate for the 2024 spherical is 5.28 per cent at a time when inflation is now fallen to low ranges once more.

So staff will take pleasure in a major actual wage improve in Japan this yr.

The Financial institution of Japan has lengthy indicated that when it was clearer that the interval of suppressed shuntō wage outcomes was coming to an finish, then they’d begin to improve rates of interest.

And that’s what they did yesterday.

The Financial institution has additionally indicated it needs the annual inflation fee to run at a steady fee of round 2 per cent and for that to occur, given productiveness progress, the wage outcomes needed to be extra sturdy.

Yesterday (March 19, 2024), the Financial institution issued a number of statements to accompany the financial coverage determination (you may see them on their Dwelling Web page).

The assertion – Modifications within the Financial Coverage Framework – explains the choice.

We learn:

On the Financial Coverage Assembly held right now, the Coverage Board of the Financial institution of Japan assessed the virtuous cycle between wages and costs, and judged it got here in sight that the value stability goal of two % could be achieved in a sustainable and steady method towards the top of the projection interval of the January 2024

The Financial institution additionally stated that there have been no main adjustments in coverage settings anticipated “in the interim” on account of the “present outlook for financial exercise and costs”.

So the coverage adjustments are minimal:

1. “encourage the uncollateralized in a single day name fee to stay at round 0 to 0.1 %” – a minor rise from -0.1 per cent within the in a single day fee.

2. “The Financial institution will proceed its JGB purchases with broadly the identical quantity as earlier than.”

3. “In case of a speedy rise in long-term rates of interest, it would make nimble responses by, for instance, rising the quantity of JGB purchases and conducting fixed-rate buy operations of JGBs” – in different phrases, (2) and (3) imply that the Financial institution will keep its strict management of longer-term charges and yields utilizing its capability because the currency-issuer.

There have been another adjustments (scrapping the purchases of personal exchange-trade funds and actual property funding trusts).

However general, the shifts are minor.

The Financial institution now hopes that the wage actions are indicative of a shift in mindset in Japan from a deflationary bias to a extra normalised surroundings the place client demand can drive financial progress by way of stronger wage contributions.

Observe the choice isn’t a mirrored image that the Financial institution of Japan is coming into line with the remainder of the central banks.

The Financial institution of Japan didn’t reply to the supply-side pressures which have pushed the current inflationary episode.

They at all times thought of that episode to be of transitory standing and that rate of interest rises would do little to handle the foundation causes of the value pressures.

Nevertheless, one shouldn’t assume that the Financial institution of Japan ever deserted ‘monetarist’ pondering with respect to the causes of inflation and the position that rate of interest will increase would possibly play.

They’re pushing charges up a bit, not as a result of the monetary markets have been pressuring them to hike, however as a result of they suppose charges have a job to play in containing inflationary pressures that come up from demand-side pressures that stronger wage actions will carry.

That could be a very orthodox view.

At any fee, the spring wage offensive this yr was a superb final result for staff and hopefully the ‘wage drawback’ in Japan is coming to an finish.

Central banker going off the planet

Whereas quite a lot of consideration was positioned on the Financial institution of Japan’s determination yesterday, one other former central banker and now chief govt of the Financial institution for Worldwide Settlements was demonstrating his willingness to implement the mainstream fictions about public debt and many others.

It’s fascinating that these so-called ‘impartial’ central bankers suppose they’ve the scope to make commentary about fiscal issues, that are inately political issues.

However, after all, the ‘independence’ of the central banks is simply one other facet of the ficitonal world that the mainstream economists have created to depoliticise financial determination making and make it more durable for coverage makers to be politically accountable to the voting public.

Anyway, Agustin Carstens gave a speech – Belief and macroeconomic stability: a virtuous circle – in Germany on March 18, 2024 and spun the standard scare claims about public debt, inflation and many others.

Amongst different issues he stated that:

… it’s crucial for fiscal authorities to curb the relentless rise in public debt … the times of ultra-low charges are over. Fiscal authorities have a slender window through which to get their home so as earlier than the general public’s belief of their commitments begins to fray. As I identified earlier, monetary markets can stay calm within the face of enormous imbalances till abruptly, sooner or later, they not are.

That’s the reason fiscal consolidation in lots of economies wants to start out now.

So at a time when many countries are in recession or approaching that state, this bullyboy is urging governments to make that scenario worse and drive unemployment up even additional.

Already, journalists are claiming that the ‘Truss mini-budget’ in October 2022 is an instance of how monetary markets will sink a nation that’s not obeying sound finance rules.

The Truss folly is simply one other of those legendary occasions which can be used to eschew the usage of fiscal coverage to advance basic well-being.

The monetary markets attacked the gilt market and the pound at the moment as a result of they knew the dedication of the coverage authorities to their plan of action was weak, given the political circumstances.

Bond yields did rise however that was as a result of the Financial institution of England allowed them to.

And Truss was so precariously in situ because the PM that the gamblers within the markets knew they might wager towards her and win.

Comparable bets have constantly misplaced in Japan through the years as a result of the authorities there are far more sure of their energy and targets.

Anyway, that can do for right now.

Music – Booker Little

That is what I’ve been listening to whereas working this morning.

It’s from American trumpet participant – Booker Little – together with his greatest quartet comprising:

1. Tommy Flanagan – piano (tracks 1, 2, 5 and 6).

2. Wynton Kelly – piano (tracks 3 & 4).

3. Scott LaFaro (tracks 1-6) – bass

4. Roy Haynes (tracks 1-6) – drums

The self-title album – Booker Little – was recorded in 1960 and launched the identical yr.

Booker Little died the yr after its launch on the age of 23 (affected by kidney failure).

He was within the arduous bop custom and was profilic throughout his energetic years which began as a youngster.

What else he would have achieved if he had have lived a full life is unknown however he left some fabulous music which is frequently on my play checklist.

That’s sufficient for right now!

(c) Copyright 2024 William Mitchell. All Rights Reserved.

[ad_2]