{kind=link}

[ad_1]

I used to be going to put in writing in regards to the acquisition of U.S. Metal in the present day, however I ended up studying an entire lot in regards to the historical past of the metal business, in order that’ll have to attend till tomorrow. Within the meantime, right here’s a fast submit about macroeconomics.

At this level, most commentators agree that the U.S. is prone to obtain the elusive and much-sought-after “comfortable touchdown” — bringing inflation down with out hurting employment or wages. The truth is, that is truly a a lot higher end result than what I personally would have known as a “comfortable touchdown” — that is nearer to what I’d have known as “immaculate disinflation”.

Economists usually assume that there’s speculated to be a short-term tradeoff between inflation and unemployment. Principally, the best way you’re speculated to deliver inflation down is to throw lots of people out of labor, after which they cease shopping for as a lot stuff, which brings down demand, which lowers costs. That’s the “Previous Keynesian” mind-set, and relying on which fashions and which parameters you utilize, it’s how a whole lot of New Keynesian fashions work too.

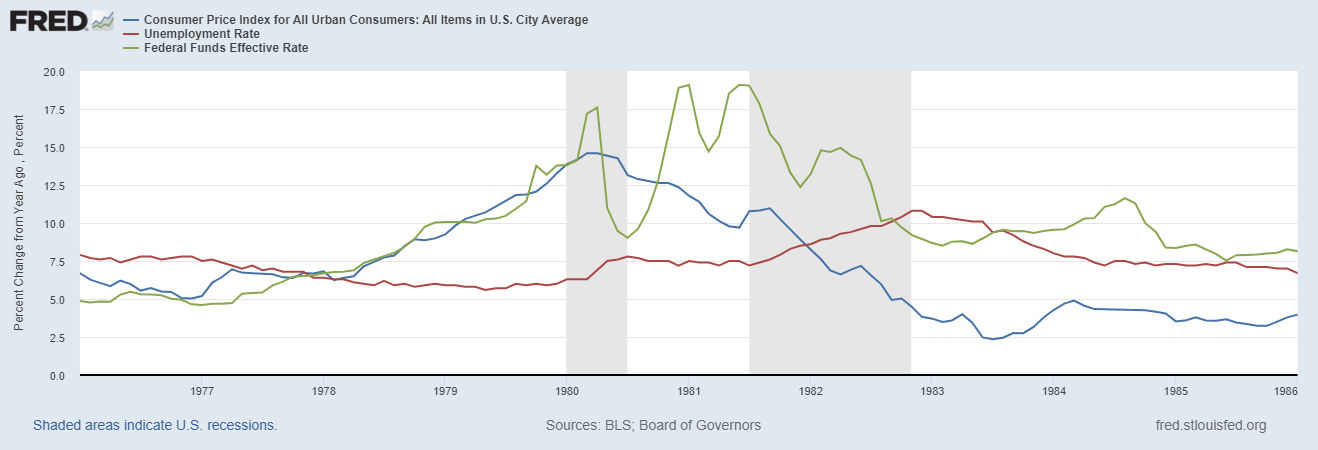

This isn’t simply principle, although — that is the way it truly labored up to now. Right here’s an image of the years when Paul Volcker ended the inflation of the Seventies. You may see that Volcker hiked rates of interest (inexperienced), which introduced down inflation (blue), but in addition prompted an enormous rise in unemployment (purple):

This was a “exhausting touchdown”. And most economists thought that one thing related would occur this time round. A survey of 47 economists in mid-2022 discovered that three-quarters believed a recession was coming earlier than the beginning of 2024:

So why had been the economists incorrect, and the way did we handle to tug off this feat? There are three fundamental theories.

This principle, endorsed by Paul Krugman and another principally Keynesian economists, is that the inflation of 2021-22 was prompted primarily by non permanent provide shocks, which light over time.

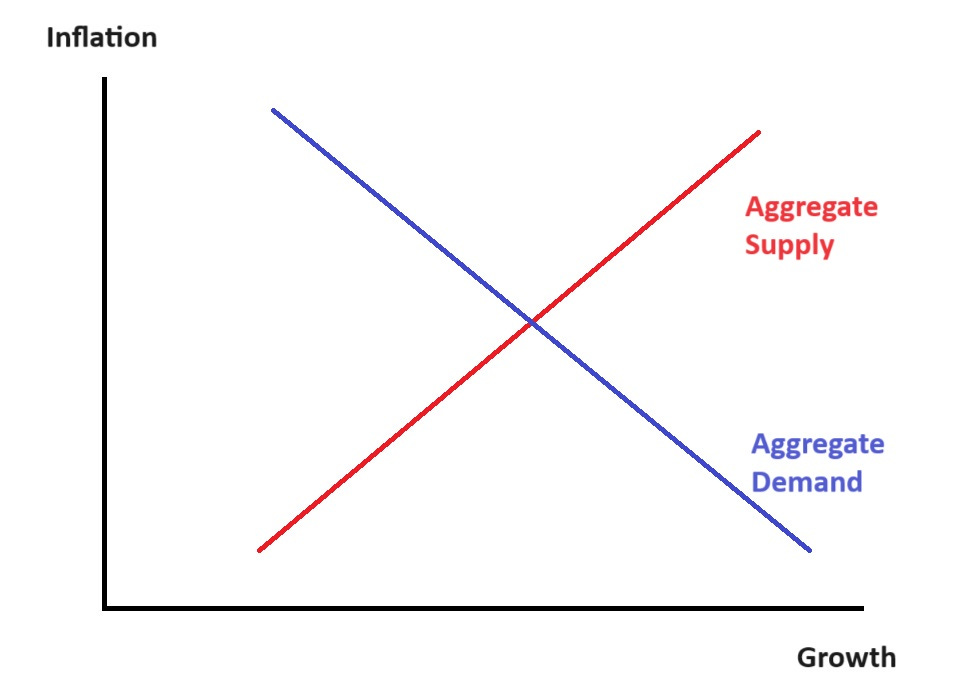

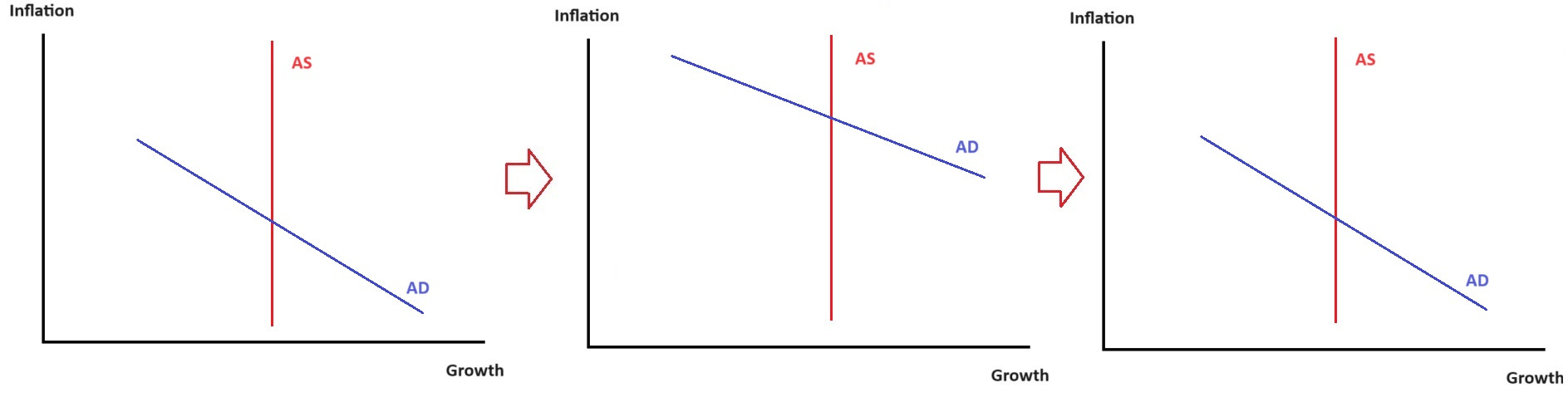

Let’s keep in mind our fundamental macroeconomic principle of combination provide and combination demand:

Additionally, do not forget that larger development means decrease unemployment.

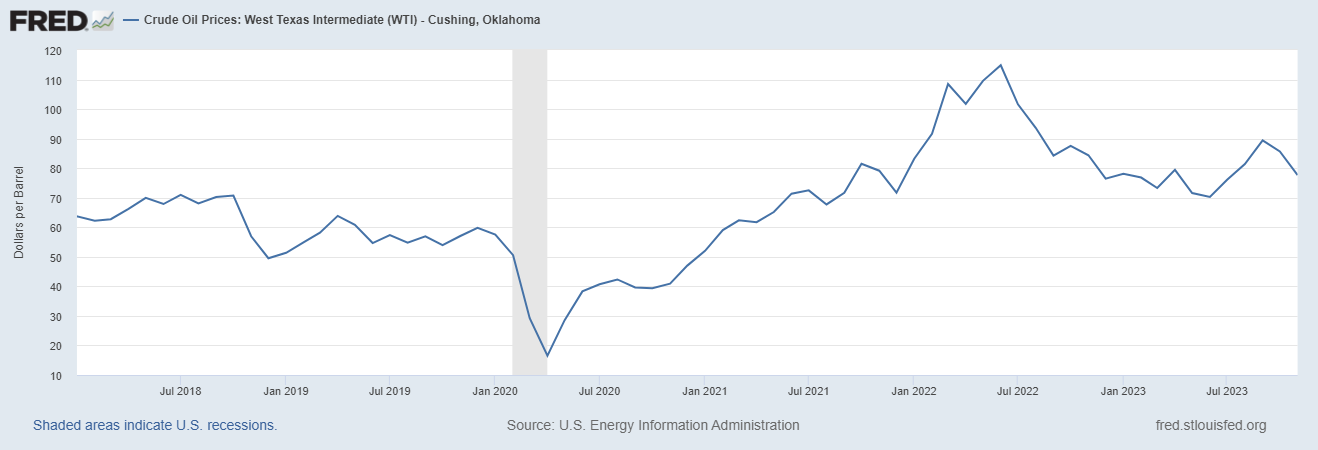

Anyway, after the pandemic we had a bunch of snarled provide chains, after which in early 2022 we obtained a speedy rise in oil costs from Putin’s invasion of Ukraine. Then provide chain pressures began to ease in 2022 and had been again to regular by the beginning of 2023:

And oil costs fell in late 2022:

So principally, right here’s what that sequence of occasions would seem like within the easy AD-AS principle:

Principally, provide bounces forwards and backwards and finally ends up the place it was earlier than. Inflation is briefly larger and development is briefly decrease, after which every thing goes again to the way it was.

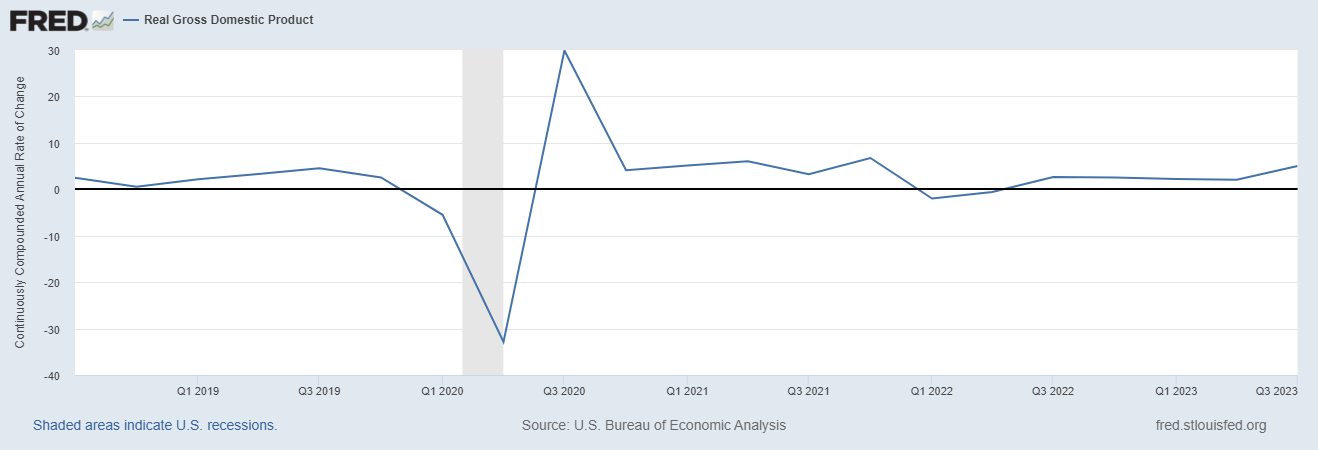

The issue with this principle is…development didn’t actually sluggish a lot. It wobbled for a few quarters in early 2022, however not sufficient for a recession to be known as:

However provide chains had been very wired in 2021, and oil costs had already begun rising. Why was development so robust in 2021? Even for those who assume that combination demand may be very inelastic (i.e. that the blue line on the diagram I drew goes straight up and down), it’s exhausting to clarify why 2021 was such a growth 12 months, if the one factor occurring was a unfavorable provide shock.

The opposite downside with the Lengthy Transitory principle is that it means the Fed’s energy to have an effect on both inflation or the actual financial system may be very restricted. If elevating rates of interest from 0% to five% and massively growing the federal funds deficit principally does nothing to combination demand, it calls into query the entire energy of Keynesian stabilization coverage. Lengthy Transitory is principally a principle of Fed irrelevance.

The speculation of Actual Enterprise Cycles (RBC) is definitely much more complicated than the best way I’m going to explain it proper right here, however I feel this will get the simplest model throughout.

Principally, within the context of this easy mannequin, you may consider RBC as saying that combination provide strikes round by itself — that it doesn’t matter what occurs to combination demand, the financial system merely produces as a lot because it’s going to provide. In that case, the one factor that combination demand can do is to have an effect on costs. In the phrases of Ed Prescott, the inventor of RBC principle, which means financial and financial coverage are “as efficient in bringing prosperity as rain dancing is in bringing rain” — you may print cash and lend cash and hand out authorities checks, however all it’ll do is pump up inflation.

So the RBC story of 2021-2023 could be one thing like this: In 2020-21, the Fed lowered rates of interest to zero and did a ton of quantitative easing and lent out a bunch of cash, and the federal government additionally ran an enormous deficit. However in 2022 it largely stopped doing these issues. This created a transitory improve in inflation that finally ended. But it surely principally did nothing to the actual financial system, as a result of in RBC-world, financial and financial coverage by no means have an effect on the actual financial system.

Within the context of our little AD-AS graph, right here’s what that may seem like:

On this rationalization, the Fed made an enormous mistake — it ought to have merely sat there and let the free market do its factor, as a substitute of pumping up inflation.

The weak spot of this principle is that whereas it matches the essential information of 2021-23, it doesn’t match previous expertise. Volcker’s rate of interest hikes actually did appear to lift unemployment to fairly a excessive degree. And plenty of quantitative analysis has discovered that financial and fiscal coverage actually do have an effect on the actual financial system.

So if RBC explains 2021-2023, it’s a thriller as to why it labored this time when it hasn’t labored different occasions.

The primary two theories relied on the concept just one essential factor occurred to the U.S. financial system in 2021-23. However what if two essential issues occurred? What if there was a transitory demand shock and a transitory provide shock?

Underneath this “the entire above” rationalization, the story goes like this:

-

In 2020-21, the federal government printed some huge cash and lent some huge cash and borrowed some huge cash, pumping up combination demand. However in early 2022 this ended.

-

In 2021-22, provide chains obtained harassed, and oil costs rose. However in late 2022 this ended.

-

By 2023, each provide and demand had been again to regular.

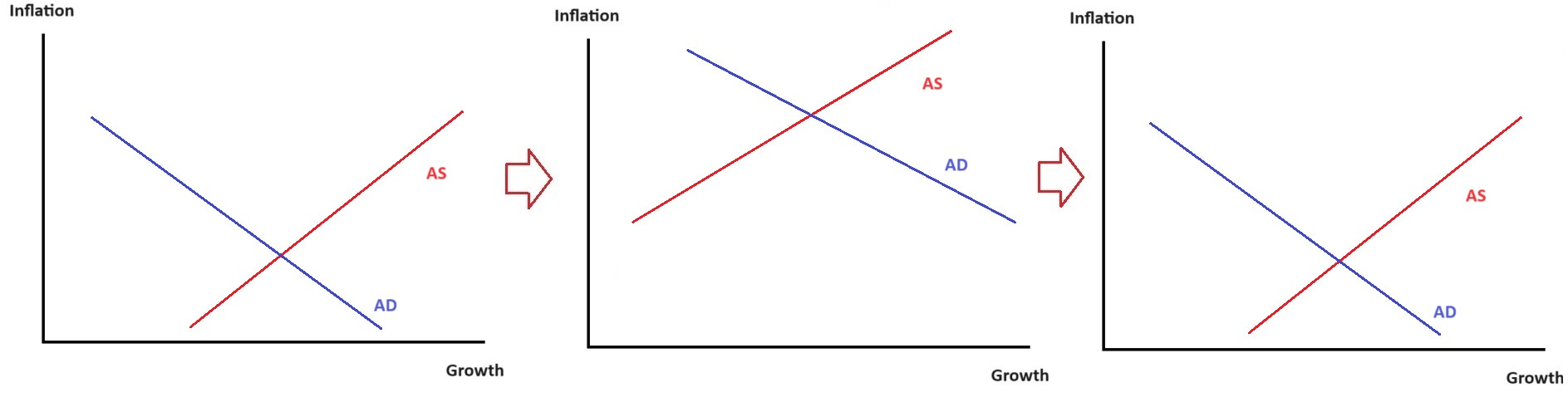

Within the context of our little AD-AS mannequin, right here’s what that appears like:

Principally, inflation rises after which falls (leaving costs completely larger than earlier than), whereas development isn’t actually affected.

That…type of appears to be like like what occurred! And in reality, the differential timing of the demand and provide shocks may even clarify why development was robust in 2021 and stumbled a bit in early 2022 — the unfavorable provide shocks got here a little bit later than the optimistic demand shocks, so in early 2022 the financial system was hit by oil costs at the same time as authorities was now not giving issues a lift.

So this principle is very good at explaining what occurred during the last three years. The issue is that it’s not very parsimonious. The good scientist John von Neumann is alleged to have remarked “with 4 free parameters I can match an elephant, with 5 I can wiggle his trunk”. We reward theories for being easy, as a result of complicated theories make issues too straightforward.

However that mentioned, generally the actual world simply isn’t parsimonious. A macroeconomy is a really complicated factor, with a whole lot of transferring elements, and every thing tends to occur abruptly. So perhaps 2021-23 simply isn’t a easy story in any respect, a lot as we’d favor it to be one.

Notice that on this rationalization, the Fed might need made a mistake in 2020-21. This hybrid principle holds that the Fed boosted development on the worth of inflicting extra inflation, and whether or not that was a superb tradeoff is dependent upon which of these belongings you care about extra. However in 2022, in response to this principle, the Fed did precisely the best factor — it lowered combination demand simply as combination provide was righting itself, resulting in decrease inflation with out slower development.

There’s yet another principle I ought to point out right here — the speculation of expectations.

Fashionable macroeconomic fashions aren’t often so simple as the little AD-AS graphs I drew above. A method they’re extra complicated is that they permit for an enormous function for expectations. In these fashions, if individuals consider that Fed coverage will probably be very dovish towards inflation sooner or later, they increase their costs in the present day, and inflation goes up. But when individuals consider that the Fed will probably be hawkish sooner or later, they’ll count on decrease inflation, and so they received’t increase costs in the present day, and inflation will go down.

In response to this principle — which macroeconomist Ricardo Reis utilized in September 2022 to efficiently predict a fall in inflation — the Fed can get one thing near immaculate disinflation if it may handle expectations successfully. And as a bonus, expectational results occur quick — they don’t should filter by a years-long chain of causality, from excessive charges to excessive unemployment to decrease shopper spending to decrease costs.

In different phrases, in response to expectations administration principle, Fed fee hikes in 2022 satisfied the nation that the spirit of Paul Volcker nonetheless animates the establishment, and that prime inflation will merely not be allowed to persist, then maybe the Fed beat inflation with out having to lift charges so excessive that they threw individuals out of labor. So on this story, as within the earlier one, the Fed did an incredible job in 2022.

How believable is that this story? We will observe the monetary market’s inflation expectations instantly, by wanting on the 5-year breakeven. This reveals that inflation expectations rose strongly in 2021, then spiked even larger in early 2022 earlier than falling to solely a little bit larger than their pre-pandemic common:

Reis has argued that the true affect of expectations was even greater than what this graph may counsel, as a result of it contained appreciable skewness — there have been lots of people who had been paying some huge cash to hedge in opposition to very excessive inflation. (There might be different causes for that sample, however it’s suggestive.)

However though this sample may appear roughly in keeping with the expectations story, different explanations are additionally doable — for instance, perhaps expectations simply comply with precise inflation, and don’t matter a lot in any respect. As standard in macroeconomics, it’s fairly exhausting to show what’s inflicting what.

So anyway, these are the 4 fundamental easy theories of how the U.S. achieved a comfortable touchdown. You may select for your self which set of assumptions you discover probably the most believable right here, and resolve which principle is your favourite. As for me, I’m simply glad all of it labored out.

[ad_2]