{kind=link}

[ad_1]

Editor’s observe: Since this submit was first revealed, the primary paragraph below the “Trying Ahead” subhead has been up to date to make clear the anticipated improve within the pace of FX transaction settlements. (Jan. 25, 2:30 p.m.)

The overseas change market has developed extensively over time, present process vital shifts within the kinds of market individuals and the combination of devices traded, inside a buying and selling ecosystem that has grow to be more and more complicated. On this submit, we focus on elementary adjustments on this market over the previous twenty-five years and spotlight a number of the implications for its future evolution. Our evaluation means that sustaining a wholesome value discovery course of and fostering a degree taking part in discipline amongst individuals are areas to look at for challenges. The results of the evolution of the FX market—effectively past these anticipated twenty-five years in the past—stay energetic areas of analysis and coverage consideration.

Evolving Dimension, Devices, and Forex Composition

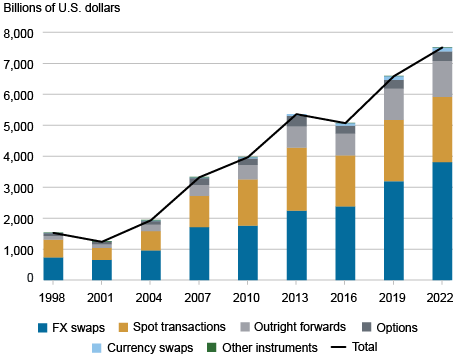

In 1998, when versatile change charges had been in place for twenty-five years, the definitive information to how the FX market operated—“All About The International Change Market in the US”—was written by Sam Cross, at the moment the Government Vice President of the International Division on the Federal Reserve Financial institution of New York. The FX market has grown considerably within the final twenty-five years since that publication, and it continues to be the most important monetary market on this planet by buying and selling quantity. Common day by day turnover elevated from $1.5 to $7.5 trillion between 1998 and 2022 (BIS 2022), with the rise occurring throughout each FX spot and FX derivatives. Over the previous ten years, nonetheless, FX spot buying and selling quantity has stagnated, whereas a lot of the expansion has come from exercise in FX swaps, devices used primarily for funding and hedging. The expansion in FX swap turnover owes partially to the shortening in maturity of those devices, as they now need to be rolled over extra regularly.

The FX Market Continues to Develop Considerably

Notes: The information don’t embrace transaction in exchange-traded FX devices, reminiscent of FX futures and associated choices. The exchange-traded FX sector is small in comparison with the general FX market.

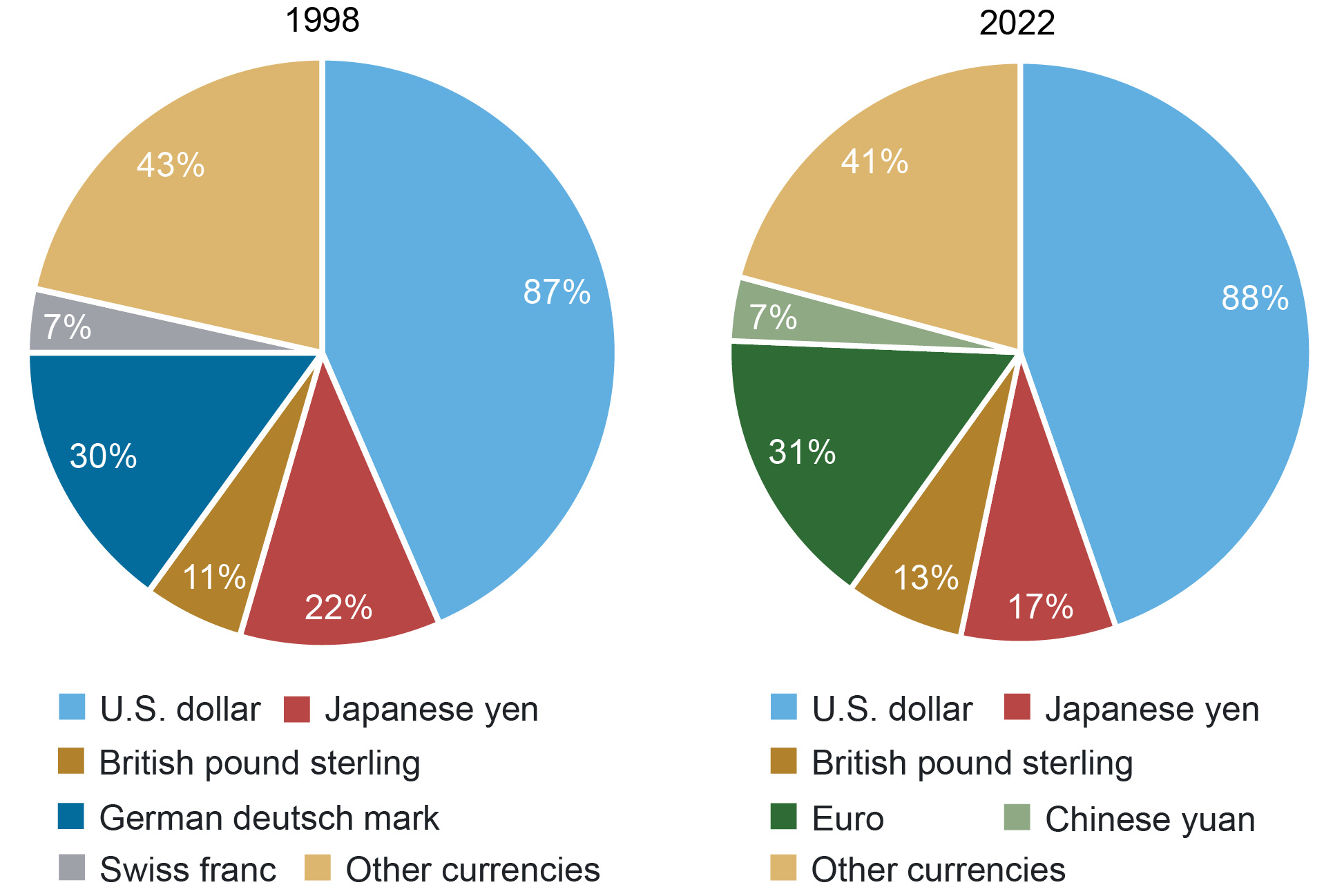

The U.S. greenback continues to play a dominant function within the FX market, because it did twenty-five years in the past. The greenback was on one aspect of 87 p.c of all FX transactions world wide in 1998, and 88 p.c in 2022. The euro, launched in 1999, has changed the German mark because the second most-traded forex and stays concerned in about 30 p.c of all transactions. The Chinese language yuan has changed the Swiss franc because the fifth most-traded forex; it’s now a part of 7 p.c of all FX transactions.

U.S. {Dollars} Stay the Dominant Forex in FX Transactions

Supply: BIS Triennial Central Financial institution Survey, 1998 and 2022.

The placement of buying and selling desks is broadly comparable right this moment in contrast with twenty-five years in the past, with the UK (virtually solely London) and the US (largely New York) accounting for a big share of the worldwide buying and selling quantity (57 p.c). FX buying and selling exercise has grown in Asia, with Singapore, Hong Kong, and Japan now accounting collectively for about 20 p.c of world FX quantity.

The U.S. and U.Ok. Proceed to Dominate FX Buying and selling

| 1998 | 2022 | ||||

| United Kingdom | 32.6 | United Kingdom | 38.1 | ||

| United States | 18.2 | United States | 19.4 | ||

| Japan | 7.0 | Singapore | 9.4 | ||

| Singapore | 6.9 | Hong Kong | 7.0 | ||

| Germany | 4.7 | Japan | 4.4 |

Observe: P.c of whole buying and selling quantity.

Broader Number of Market Individuals

The combo of FX market individuals has modified considerably, particularly within the spot market. Twenty-five years in the past, sellers at giant banks acquired orders about equally from non-financial clients, primarily firms, and from “different monetary” counterparties, reminiscent of small banks, pension funds, and hedge funds. That exercise accounted for a bit greater than a 3rd of world transactions. However virtually two-thirds of the turnover was “interdealer,” the place giant sellers traded amongst themselves to hedge and unwind their positions.

Buying and selling between sellers at giant banks has declined over time to lower than half of total turnover. One vital issue has been the rise of “internalization” whereby sellers match opposing buyer flows in-house as a substitute of unwinding positions by buying and selling within the interdealer market. Sellers in main buying and selling facilities at the moment internalize about 80 p.c of spot orders. In the meantime, buying and selling between sellers and different monetary counterparties generates virtually half of FX market exercise. Principal buying and selling corporations (PTFs, also called high-frequency merchants or HFTs), that are counted amongst different financials, have grow to be vital individuals within the spot FX market. In distinction, buying and selling involving non-financial counterparties has declined considerably, highlighting the truth that worldwide commerce now solely performs a comparatively modest function in driving FX buying and selling.

FX Market Transactions Shift to Extra Buying and selling between Different Monetary Counterparties

| Counterparty Sort | 1998 | 2022 |

| Seller/Seller | 63.0 | 46.1 |

| Seller/Different Monetary | 19.6 | 48.2 |

| Seller/Non-Monetary | 17.4 | 5.7 |

Observe: P.c of whole turnover.

More and more Advanced Ecosystem for Spot FX Market Buying and selling

The buying and selling surroundings has grow to be significantly extra complicated because the variety of execution strategies and buying and selling platforms has grown and the market has grow to be more and more digital (Chaboud, Rime, Sushko, 2023). Within the late Nineties, two digital brokers, Reuters (now Refinitiv) and Digital Broking Companies (EBS), established themselves within the interdealer market because the clear sources of value discovery, changing into recognized collectively because the “major market.” By the early 2000s, digital multi-dealer platforms started to emerge within the dealer-to-customer market, enabling purchasers to concurrently submit a request for quote (RFQ) to a number of counterparties, and banks additionally started to supply proprietary platforms permitting for direct digital commerce with purchasers. The variety of buying and selling platforms has continued to develop since then. Almost 60 p.c of buying and selling now takes place electronically, greater than double what was noticed in 1998 when many trades have been nonetheless carried out by phone.

Issues about FX Market Dangers, Resiliency, and Integrity

We view these developments as growing competitors and offering new choices to market individuals. Nonetheless, they could even have made value discovery harder within the FX market. Due to the multiplicity of buying and selling platforms and the expansion in internalization, the first market has skilled a substantial decline in buying and selling quantity previously decade and is not the only locus of value discovery. Massive market individuals now take into account a broader set of buying and selling platforms when assessing the present degree of every change fee, and the futures market has additionally grow to be more and more vital to cost discovery within the spot FX market (Chaboud, Dao, Vega, Zikes 2023). The rising complexity of the market could then have contributed to a rise within the info benefit of bigger, extra subtle market individuals, who can dedicate extra sources to evaluate the evolution of every change fee at excessive frequency.

As well as, whereas electronification will increase the provision of knowledge and analytics and helps in decreasing transaction prices, it additionally will increase the danger that less-sophisticated market individuals are deprived relative to extra technologically superior, sooner market individuals, particularly PTFs. To deal with this subject, a number of FX buying and selling platforms have launched some constraints on transactions (reminiscent of “pace bumps”), whereas others supply choices to exclude transacting with the quickest merchants.

These developments are related for the broader worldwide roles of the U.S. greenback, together with on invoicing worldwide commerce actions and all kinds of worldwide monetary transactions (Goldberg, Lerman, Reichgott 2022). Tutorial analysis reveals that forex transaction environments and buying and selling prices affect the choice of currencies for various roles, and these roles are synergistic. From the vantage level of the US, and because the greenback roles are strategic belongings, our view is that the integrity, effectivity, and resilience of the FX market assist the worldwide economic system, monetary stability, and the general public’s belief within the monetary system.

To this finish, over the previous twenty-five years, one focus of coverage efforts has been on FX settlement danger, whereas one other vital focus has been round business finest practices. FX settlement danger, or Herstatt danger, is the danger that one get together delivers the forex it has bought however doesn’t obtain the forex it bought. To cut back FX settlement danger within the international monetary system, the Steady Linked Settlement (CLS) establishment was fashioned in 2002 by market individuals with the assist of the official sector to settle FX transactions on a payment-versus-payment (PVP) foundation. This improvement helped be sure that cost in a single forex can solely happen when the cost within the different forex takes place. Whereas not all FX transactions settle via CLS, its institution was a serious milestone that resulted in a considerable discount in settlement danger.

One other focus started over a decade in the past when considerations arose concerning the habits of some market individuals, and official investigations revealed critical misconduct. In response, following a number of years of labor by the official and personal sectors, together with the International Change Committee (FXC), a Federal Reserve Financial institution of New York-sponsored business group, the FX International Code was revealed in 2017. The FX International Code supplies rules and expectations for accountable market conduct and conventions. Adoption of the Code by giant FX sellers has been widespread, and it’s growing amongst the buyside group; central banks additionally adhere to the Code, and the New York Fed has signed a assertion of dedication to display its assist. The FX International Code is an instance of a voluntary code of conduct that has had a notable influence on market habits, informing the educational dialogue concerning the relative effectiveness of strictly enforced guidelines versus voluntary adherence to good follow within the business.

Trying Ahead

On this 50th yr of versatile change charges, and 25 years since Sam Cross’s guide, the worldwide FX market continues to evolve. Conventional bank-dealers are actually challenged by non-bank individuals together with PTFs, contributing to the broader debate concerning the influence of high-frequency buying and selling on volatility and liquidity in monetary markets. Furthermore, the pace with which FX transactions are settled is about to extend quickly. Though the overwhelming majority of spot FX transactions are at the moment settled the second enterprise day after a commerce (T+2), efforts are below solution to put together for a larger quantity of trades requesting settlement of subsequent enterprise day (T+1), matching the upcoming transfer to T+1 for U.S. securities deliberate for mid-2024. This transition will create new challenges, particularly when an FX commerce includes two nations with vast time zone variations.

Additional down the highway, some central banks are growing their very own central financial institution digital currencies (CBDCs). This opens the chance for the quasi-immediate settlement of FX trades, an idea lately examined by the BIS. If many nations undertake their very own CBDCs, there’ll doubtless be far-reaching penalties for the basic construction and functioning of the worldwide FX and cost ecosystem, together with the function of the present intermediaries.

Our views are that analysis must deal with and determine the challenges which can be more likely to come up from these transitions and the broader evolution of the FX market. International currencies play a necessary function in each worldwide commerce and finance. For the U.S. particularly, the greenback’s key worldwide roles implies that developments on this area bear additional evaluation and monitoring. As a well-functioning and resilient FX market is crucial to the worldwide economic system, official establishments will then need to act decisively to foster helpful outcomes on this immensely vital international monetary market.

Alain Chaboud is a senior financial mission supervisor on the Federal Reserve Board of Governors.

Lisa Chung is the director of Capital Markets Buying and selling within the Federal Reserve Financial institution of New York’s Markets Group.

Linda S. Goldberg is a monetary analysis advisor for Monetary Intermediation Coverage Analysis within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Anna Nordstrom is the top of Capital Markets Buying and selling within the Federal Reserve Financial institution of New York’s Markets Group.

How one can cite this submit:

Alain Chaboud, Lisa Chung, Linda S. Goldberg, and Anna Nordstrom, “In the direction of Growing Complexity: The Evolution of the FX Market,” Federal Reserve Financial institution of New York Liberty Road Economics, January 11, 2024, https://libertystreeteconomics.newyorkfed.org/2024/01/towards-increasing-complexity-the-evolution-of-the-fx-market/.

Disclaimer

The views expressed on this submit are these of the writer(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).

[ad_2]