{kind=link}

[ad_1]

When inflation picked again up in January 2024, many commentators described it as extra noise than sign. The newest knowledge from the Bureau of Financial Evaluation (BEA) casts doubt on that view.

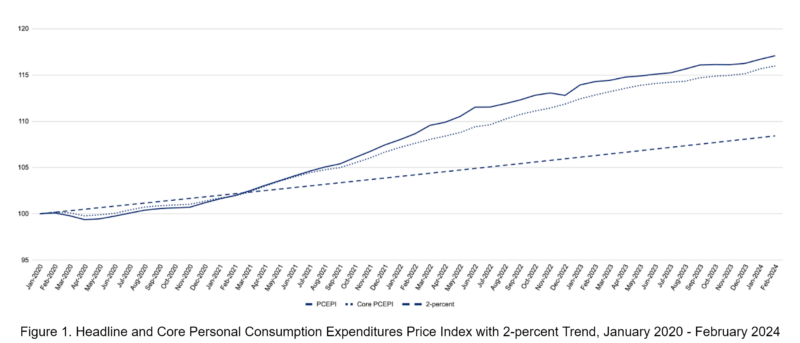

The Private Consumption Expenditures Worth Index (PCEPI), which is the Federal Reserve’s most popular measure of inflation, grew at a constantly compounding annual charge of 4.0 % in February. The PCEPI has grown at an annualized charge of three.3 % during the last three months and a pair of.5 % during the last six months. Costs immediately are 8.7 proportion factors larger than they’d have been had they grown at an annualized charge of two.0 % since January 2020.

Core inflation, which excludes unstable meals and power costs, additionally remained elevated. Core PCEPI grew at a constantly compounding annual charge of three.1 % in February. It has grown at an annualized charge of three.5 % during the last three months and a pair of.9 % during the last six months.

On the press convention following the Federal Open Market Committee (FOMC) assembly in March, Federal Reserve Chair Jerome Powell advised reporters the FOMC was previous cautiously:

We didn’t excessively rejoice the nice inflation readings we acquired within the final seven months of final yr. We didn’t take an excessive amount of sign out of that. What you heard us saying was that we would have liked to see extra. That we might, that we wished to watch out about that call. And we’re not going to overreact as effectively to those two months of knowledge, nor are we going to disregard them.

That would appear to suggest the FOMC doesn’t plan to chop its federal funds charge goal quickly.

Governor Christopher Waller echoed Powell’s view in a chat on the Financial Membership of New York earlier this week:

It’s acceptable to level out {that a} month or two of knowledge doesn’t essentially point out a development, and there are good causes to suppose that progress on inflation will probably be uneven however more likely to proceed down towards 2 %. On the identical time, financial coverage is knowledge pushed, and I do need to take it into consideration when formulating my financial outlook. Whereas I don’t need to over-react to 2 months of knowledge, I do suppose it’s acceptable to react to it.

Waller stated “there is no such thing as a rush to chop the coverage charge.” Given the most recent knowledge, he thinks “it’s prudent to carry this charge at its present restrictive stance maybe for longer than beforehand thought to assist maintain inflation on a sustainable trajectory towards 2 %.”

The median FOMC member continued to challenge three 25-basis-points cuts on the March assembly. However many FOMC members revised their projection up. In December 2023, there have been 5 below-median projections for the federal funds charge this yr. Now, there’s just one.

Market members proceed to anticipate three cuts this yr — and that these cuts will start within the first half of the yr. However they’ve adjusted the percentages. The federal funds futures market places the percentages that the Fed will maintain its goal charge at 5.25 to five.5 % by June at simply 36.4 %, up from 24.4 % one week in the past.

Fed officers look prescient in the meanwhile. They held their federal funds charge goal excessive when low inflation readings led others (myself included) to name for cuts. The months forward will decide whether or not that evaluation stands.

William J. Luther

William J. Luther is the Director of AIER’s Sound Cash Undertaking and an Affiliate Professor of Economics at Florida Atlantic College. His analysis focuses totally on questions of foreign money acceptance. He has revealed articles in main scholarly journals, together with Journal of Financial Habits & Group, Financial Inquiry, Journal of Institutional Economics, Public Selection, and Quarterly Evaluation of Economics and Finance. His in style writings have appeared in The Economist, Forbes, and U.S. Information & World Report. His work has been featured by main media retailers, together with NPR, Wall Road Journal, The Guardian, TIME Journal, Nationwide Evaluation, Fox Nation, and VICE Information. Luther earned his M.A. and Ph.D. in Economics at George Mason College and his B.A. in Economics at Capital College. He was an AIER Summer time Fellowship Program participant in 2010 and 2011.

[ad_2]