{kind=link}

[ad_1]

A traditional query for U.S. monetary corporations is whether or not to arrange themselves as entities which might be affiliated with a bank-holding firm (BHC). This affiliation brings advantages, resembling entry to liquidity from different affiliated entities, in addition to prices, significantly a bigger regulatory burden. This publish highlights the outcomes from a latest Workers Report that sheds mild on this tradeoff. This work makes use of confidential knowledge on the inhabitants of broker-dealers to review the advantages of being affiliated with a BHC, with a give attention to the worldwide monetary disaster (GFC). The evaluation reveals that affiliation with a BHC makes broker-dealers extra resilient to the combination liquidity shocks that prevailed in the course of the GFC. This ends in these broker-dealers being extra keen to carry riskier securities on their steadiness sheet relative to broker-dealers that aren’t affiliated with a BHC.

Information and Background

Dealer-dealers symbolize a great setting to investigate the worth to being affiliated with a BHC for 2 causes. First, broker-dealers exist as each standalone corporations and as a part of BHCs, the required variation in organizational kind. Second, broker-dealers are typically extremely levered and as such are delicate to modifications in market and funding liquidity. As such, an affiliation with a BHC, and thereby entry to the liquidity {that a} BHC can present, could possibly be fairly essential to a broker-dealer, particularly throughout instances of stress.

Our evaluation makes use of steadiness sheet and revenue assertion knowledge from the Monetary and Operational Mixed Uniform Single (FOCUS) report varieties filed by all broker-dealers which might be registered with the U.S. Securities and Trade Fee (SEC). The Monetary Business Regulatory Authority (FINRA) offered entry to those confidential stories filed by its member corporations, the overwhelming majority of broker-dealers. As such, the complete cross part of broker-dealers is taken into account. The work focuses on the GFC, as a result of it’s exactly throughout such an mixture liquidity shock that one expects an affiliation with a BHC to matter.

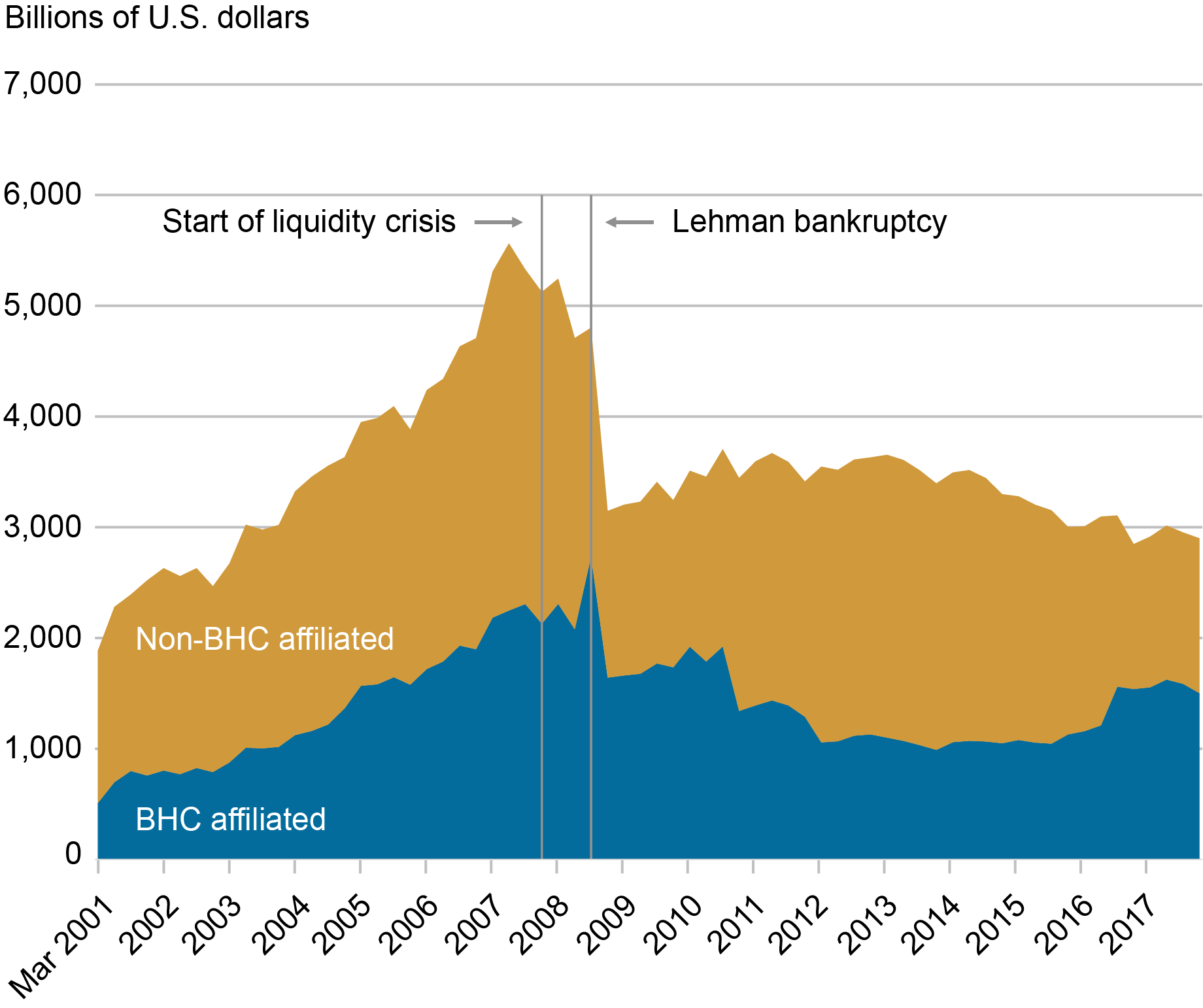

The chart under demonstrates that by way of whole belongings, broker-dealers are roughly spilt throughout BHC affiliated and non-BHC affiliated from 2004 to 2011. Each forms of broker-dealers suffered in the course of the GFC, with a big decline in whole belongings after the chapter of Lehman Brothers in September 2008.

BHC and Non-BHC Dealer-Sellers Misplaced Property after the Lehman Chapter

Evaluation

Our evaluation of sellers’ steadiness sheets seems to be for proof of broker-dealers shifting towards buying and selling Treasuries to a bigger diploma over the GFC, given the protection and liquidity of those securities. Moreover, the evaluation considers whether or not there’s a distinction in conduct between BHC-affiliated and non-BHC affiliated broker-dealers. Modifications in buying and selling technique round Treasuries will present up on steadiness sheets as modifications in repo and reverse repo exercise, in addition to lengthy stock holdings. Consequently, we give attention to these three steadiness sheet objects.

The desk under particulars how these three steadiness sheet objects, as a share of whole belongings, assorted throughout the pre-crisis interval (2004:Q1 to 2007:Q3) and in the course of the disaster (2007:This autumn to 2011:This autumn).

Within the Disaster, Non-BHC Dealer-Sellers Moved Towards Buying and selling Treasuries Not like BHC Dealer-Sellers

| Non-BHC | BHC | |||

| Pre-crisis | Disaster | Pre-crisis | Disaster | |

| Repo share of whole belongings | 40.7% | 43.4% | 45.3% | 30.0% |

| Reverse repo share of whole belongings | 31.9% | 37.9% | 33.2% | 21.6% |

| Authorities securities share of lengthy stock | 50.2% | 54.7% | 45.6% | 42.5% |

Notes: BHC is the group of broker-dealers affiliated with a bank-holding firm, non-BHC is the group of broker-dealers not affiliated with a bank-holding firm. Additional, pre-crisis is from the primary quarter of 2004 to the third quarter of 2007 and disaster is from the fourth quarter of 2007 to the fourth quarter of 2011.

In the course of the disaster, non-BHC affiliated broker-dealers elevated their repo and reverse repo actions as a share of whole belongings. For these broker-dealers, repo exercise’s share of whole belongings climbed from 40.7 to 43.4 %. Equally, reverse repo exercise’s share elevated from 31.9 to 37.9 %. In distinction, BHC broker-dealers decreased their repo and reverse repo exercise by substantial quantities.

These modifications in repo and reverse shares are in line with the story of non-BHC affiliated broker-dealers reacting to an mixture liquidity shock with a flight to high quality and so growing their buying and selling of Treasuries. Moreover, BHC affiliated broker-dealers, given their entry to inside capital markets, didn’t face the identical liquidity pressures and decreased their share of buying and selling Treasuries.

This story is additional supported by contemplating authorities securities’ share of lengthy stock. Non-BHC affiliated broker-dealers enhance this share by 4.5 proportion factors, on common, whereas BHC affiliated broker-dealers decreased this share by 3.1 proportion factors.

Formal regression evaluation reinforces this message and demonstrates that the outcomes outlined above are strong. A most important result’s that non-BHC affiliated broker-dealers shift towards the usage of repos and reverse repos as a share of whole belongings by greater than 10 proportion factors relative to BHC affiliated broker-dealers. As well as, there’s a dramatic distinction within the composition of lengthy stock, the place the estimated coefficients indicate that non-BHC affiliated broker-dealers elevated the share of Treasuries held in lengthy stock by 5 proportion factors whereas BHC affiliated broker-dealers decreased that share by 10 proportion factors.

Takeaway

Our most important consequence supplies proof that broker-dealers that aren’t related to BHCs dramatically re-structured their steadiness sheet in the course of the GFC, pivoting away from illiquid belongings and towards extra liquid authorities securities. Sellers related to BHCs didn’t must endure such excessive modifications partially as a result of that they had entry to inside liquidity. This allowed BHC-affiliated sellers to supply extra intermediation companies in a variety of monetary markets that have been underneath stress, possible decreasing the extent of the disruptions.

The advantages from getting access to inside liquidity are possible informative about the advantages of entry to liquidity from the Federal Reserve. The truth is, the advantages of entry to central financial institution liquidity are prone to be higher since that liquidity needs to be extra dependable than entry to inside liquidity. Amongst broker-dealers, the Federal Reserve’s Standing Repo Facility (SRF) is simply obtainable to major sellers. The outcomes of this work counsel that there could possibly be advantages to wider entry to broker-dealers, particularly these not affiliated with BHCs, consistent with the advice of the Group of Thirty report.

Adam Copeland is a monetary analysis advisor in Cash and Funds Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Cecilia Caglio is the chief of the monetary construction part on the Federal Reserve Board.

How you can cite this publish:

Cecilia Caglio and Adam Copeland, “Inner Liquidity’s Worth in a Monetary Disaster,” Federal Reserve Financial institution of New York Liberty Avenue Economics, April 8, 2024, https://libertystreeteconomics.newyorkfed.org/2024/04/internal-liquiditys-value-in-a-financial-crisis/.

Disclaimer

The views expressed on this publish are these of the creator(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the creator(s).

[ad_2]