{kind=link}

[ad_1]

Inflation all over the world elevated dramatically with the reopening of economies following COVID-19. After reaching a peak of 11 p.c within the second quarter of 2021, world commerce costs dropped by greater than 5 share factors by the center of 2023. U.S. import costs adopted an analogous sample, albeit with a decrease peak and a deeper trough. In a new examine, we examine what drove these worth actions through the use of info on the costs charged for merchandise shipped from fifty-two exporters to fifty-two importers, comprising greater than twenty-five million commerce flows. We uncover a number of patterns within the knowledge: (i) From 2021:Q1 to 2022:Q2, nearly the entire progress in U.S. import costs will be attributed to world components, that’s, tendencies current in most international locations; (ii) on the finish of 2022, U.S. import worth inflation began to be pushed by U.S. demand components; (iii) in 2023, overseas suppliers to the U.S. market caught up with demand and account for the decline in import worth inflation, with a major position performed by China.

Methodology

We use bilateral commerce knowledge for all shipments of disaggregated merchandise from an exporting nation to an importing nation for fifty-two international locations, which make up greater than 90 p.c of U.S. imports. We divided the worth of every HS10-country commentary by the amount to type the unit worth, which is our measure of the value. We estimate the typical change in log costs for every exporter and every importer for every product in every quarter, all relative to the worldwide median worth. We consult with the worldwide median because the “world frequent shock,” the exporter common worth change much less the median change because the “idiosyncratic provide shock,” and the importer common worth change much less the median one because the “idiosyncratic demand shock.” Our forthcoming publication within the American Financial Affiliation (AEA) Papers and Proceedings gives extra particulars of this technique. Beneath, we summarize our findings, and for this put up, we prolong the pattern interval to incorporate 2023.

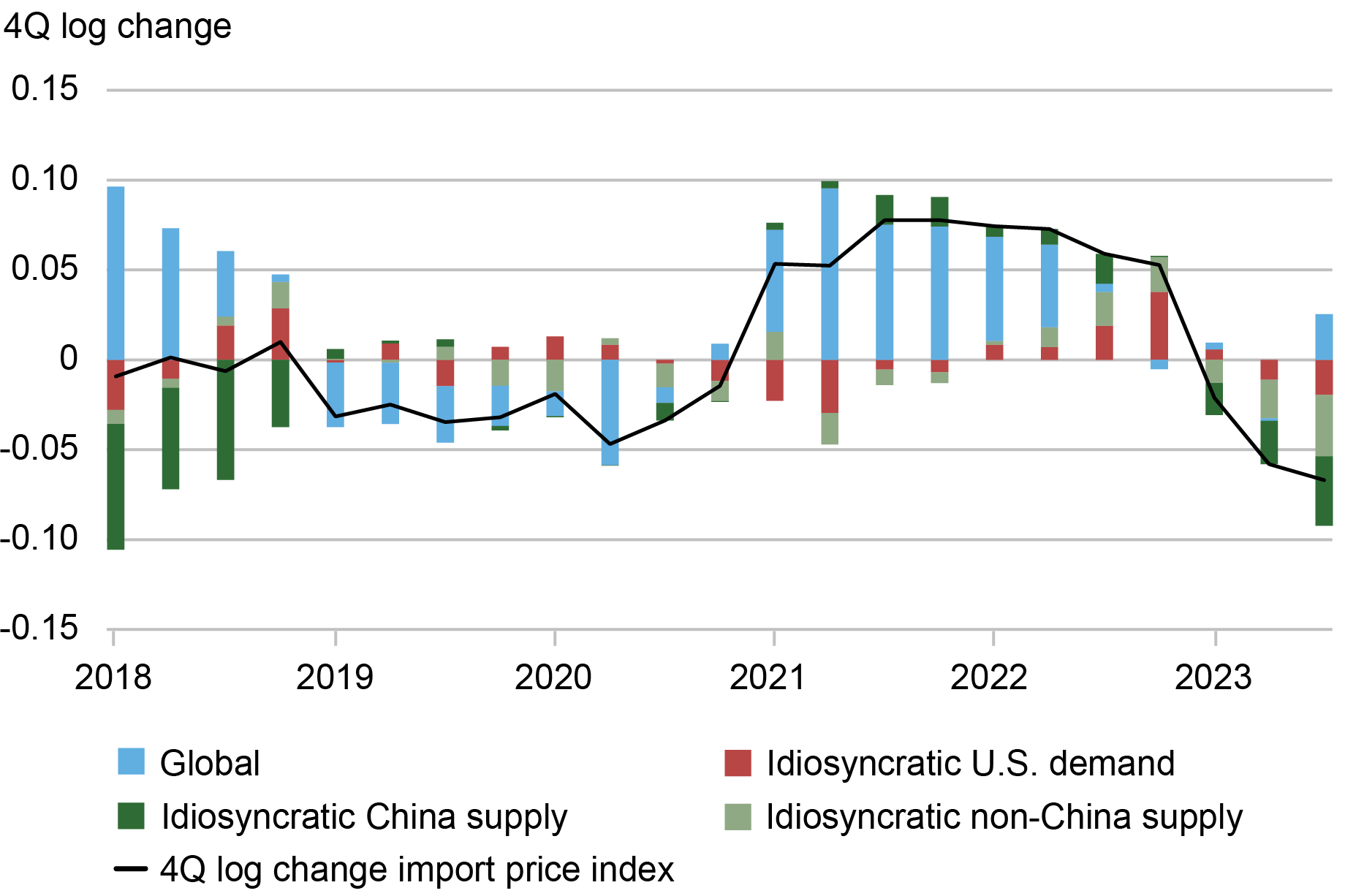

U.S. Mixture Import Costs

The chart beneath plots the decomposition of the modifications in combination U.S. import costs and exhibits the sources of the rise and fall of combination import worth inflation, equivalent to the black line. We additionally plot every of the three parts (frequent, idiosyncratic U.S. demand, and idiosyncratic export provide worth shocks), the place we additional cut up the export provide worth shock into the component pushed by China (darkish inexperienced) and different exporters to the U.S. (mild inexperienced). The sum of the coloured bars equals the change within the combination import costs.

International Elements Drive Progress in U.S. Import Costs after COVID-19 till Mid-2022

Observe: See Amiti, Itskhoki, Weinstein, “What Drives U.S. Import Value Inflation?” for particulars.

The chart exhibits that import worth inflation was pushed primarily by the worldwide frequent shock (blue bars) till the second half of 2022. Import worth inflation rose to eight p.c within the second half of 2021 and fell to -6 p.c by the third quarter of 2023. The worldwide frequent issue (blue bars) performed a dominant position within the aftermath of COVID-19 when all international locations struggled to re-open their economies. Nonetheless, by the top of 2022, the worldwide frequent issue stopped affecting import worth inflation. As an alternative, idiosyncratic U.S. demand and later worth reductions by the main exporters to the U.S. performed the dominant position in worth fluctuations.

Specifically, idiosyncratically robust demand within the U.S. maintained excessive import inflation charges within the second half of 2022. Nonetheless, this demand impact was short-lived and fell to shut to zero firstly of 2023. These findings recommend that the majority import worth inflation was frequent to all international locations till the center of 2022 and, due to this fact, can’t be defined by distinctive U.S. insurance policies or insurance policies peculiar to our buying and selling companions. In different phrases, COVID-19 was a worldwide shock that affected import costs in all international locations roughly equally.

As provide chain pressures have eased, import costs have fallen, and we see that idiosyncratic provide shocks have been answerable for the value declines in 2023. Maybe in response to the excessive import costs that emerged after COVID-19, the U.S.’s main suppliers ramped up manufacturing and dropped costs. The darkish inexperienced bars point out that a lot of the drop in import costs is because of China, whose exporters dropped costs by greater than these in different international locations. These patterns recommend that the U.S. import worth inflation was not as a consequence of a poor selection of buying and selling companions.

Within the wake of COVID-19, import costs rose within the U.S. as a result of they rose in every single place and never due to idiosyncratic U.S. demand or choices made by our main import suppliers. When U.S. import costs fell in 2023, it was largely the product of enormous worth drops by China and our different main import suppliers. A number of the decline within the U.S. import costs in 2023 could also be as a result of relative power of the U.S. greenback, however we discover little correlation between trade-weighted USD and import worth inflation over the remainder of the pattern interval.

Mary Amiti is the top of Labor and Product Market Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Oleg Itskhoki is a professor of economics on the College of California, Los Angeles.

David E. Weinstein is the Carl S. Shoup Professor of the Japanese Financial system at Columbia College.

How one can cite this put up:

Mary Amiti, Oleg Itskhoki, and David E. Weinstein, “International Provide Chains and U.S. Import Value Inflation,” Federal Reserve Financial institution of New York Liberty Avenue Economics, March 4, 2024, https://libertystreeteconomics.newyorkfed.org/2024/03/global-supply-chains-and-u-s-import-price-inflation/.

Disclaimer

The views expressed on this put up are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).

[ad_2]