{kind=link}

[ad_1]

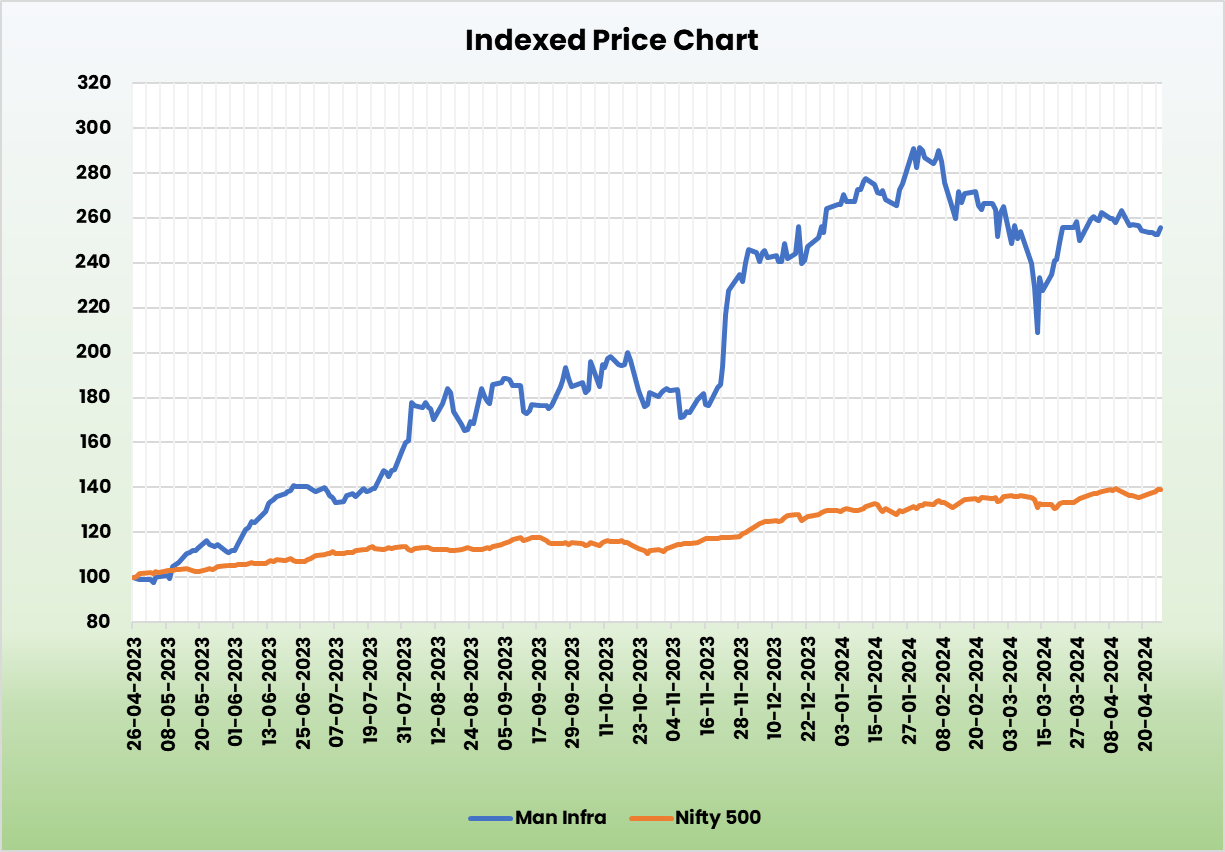

Man Infraconstruction Ltd. – A key participant in infrastructure growth

Man Infraconstruction Ltd (MICL), established in 2002 and headquartered in Mumbai, is an built-in EPC (Engineering, Procurement & Development) firm famend for its experience in numerous development segments. With a observe document of delivering landmark tasks throughout India, MICL is especially acknowledged for its superior high quality development and well timed mission supply in the actual property sector.

Product Portfolio of MICL

- Port infrastructure: Onshore container terminals, land reclamation, operational providers.

- Industrial & Institutional Constructions: IT parks, workplace complexes, accommodations, malls, colleges, hospitals.

- Street constructions: Earthwork, paving, electrification, landscaping.

- Residential Constructions: Excessive rise buildings, townships, luxurious villas.

- Industrial Constructions: Factories, chilly storages, warehouses, manufacturing models.

- Subsidiaries: 17 subsidiaries, 3 affiliate firms, and 1 three way partnership as of FY23.

Progress Methods of MICL

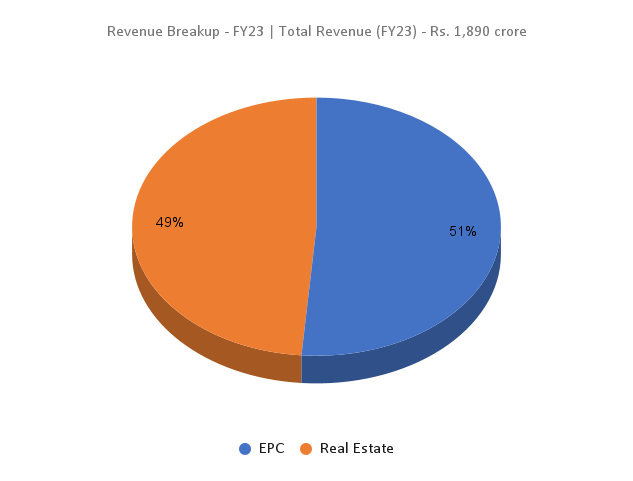

- Diversified enterprise mannequin encompasses Engineering, Procurement, and Development (EPC) alongside Actual Property Growth.

- EPC phase generates earnings from infrastructure tasks like ports, institutional buildings, and residential tasks.

- Potential for extra earnings by Challenge Administration Consultancy (PMC) charges.

- Emphasis on an asset-light method by subsidiaries, joint ventures, and associates.

- Upcoming tasks embrace ultra-luxurious residential ventures in Mumbai and redevelopment tasks.

- Worldwide growth with investments within the US market, together with tasks in Fort Lauderdale and Miami.

Monetary Highlights of MICL

Q3FY24 Efficiency

- Income: Rs.242 crore, reflecting a 47% decline in comparison with Q3FY23.

- Working Revenue: Recorded at Rs.103 crore, marking a 20% lower from Q3FY23.

- Web Revenue: Stood at Rs.87 crore, with a marginal 4% decline.

- Noteworthy Enchancment: Working revenue margin elevated to 43%, and internet revenue margin rose to 36%, up from 28% and 20% respectively in Q3FY23.

- Quarter-over-Quarter Progress: In comparison with the earlier quarter (Q2FY24), income elevated by 13%, working revenue surged by 61%, and internet revenue improved by 34%.

Monetary Efficiency (FY20-23)

- Compound Annual Progress Charge (CAGR): MICL has achieved a commendable income and Revenue After Tax (PAT) CAGR of 24% and 31% respectively over the interval from FY20 to FY23.

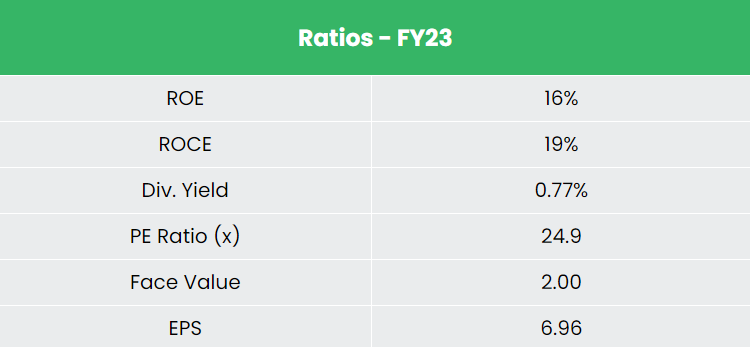

- Return on Fairness (ROE) & Return on Capital Employed (ROCE): The common 5-year ROE and ROCE stand at round 14% and 18% respectively for the FY18-23 interval.

- Robust Steadiness Sheet: MICL boasts a strong debt-to-equity ratio of 0.18, indicating a wholesome monetary place and environment friendly capital administration.

Trade Outlook

- The infrastructure sector stays pivotal for India’s financial development, spearheading complete growth initiatives.

- Authorities deal with coverage implementation ensures the time-bound creation of top-tier infrastructure, driving financial development.

- The development market is poised to broaden considerably, anticipated to succeed in US$ 1.42 trillion by 2027.

- Urbanization developments point out a burgeoning demand for housing, with an estimated 600 million city dwellers by 2030.

- Infrastructure growth acts as a catalyst, fostering development in ancillary sectors like townships, housing, and development tasks.

- Strong development is forecasted, with a projected CAGR of 17.26% through the 2022-2027 interval, signaling ample alternatives for sectoral growth.

Progress Drivers

- Authorities initiatives just like the Nationwide Infrastructure Pipeline and Make in India.

- Funds allocation of Rs.10 lakh crore for infrastructure.

- 100% FDI in accomplished development tasks.

Aggressive Benefit

In comparison with rivals like Macrotech Builders Ltd, NCC Ltd and many others, MICL has the next benefits:

- Superior undervalued inventory with constant gross sales development.

- Efficient utilization of capital in comparison with rivals.

Outlook

- Indian actual property sector anticipated to develop to $1 trillion by 2030, comprising 13% of India’s GDP by 2025.

- MICL poised for development with an actual property gross sales visibility of Rs.12,000 crore from FY24 launches and upcoming tasks.

- Area of interest in redevelopment and cluster tasks guarantees higher returns on capital.

- Monitor document of delivering tasks forward of schedule with superior high quality and execution.

- Lively addition of recent tasks with quicker completion tempo and ongoing mission fund elevate.

- Sequence of tasks slated for launch subsequent 12 months, together with Pali Hill, Kala Nagar, Marine Traces, Ghatkopar, Dahisar, and Goregaon.

- Holding a considerable EPC order e book of Rs.1,047 crore, indicating a strong pipeline for future income.

Valuation

- Favorable financial fundamentals and optimistic client sentiments driving actual property sector development.

- MICL’s wholesome stability sheet and increasing order e book point out regular development potential.

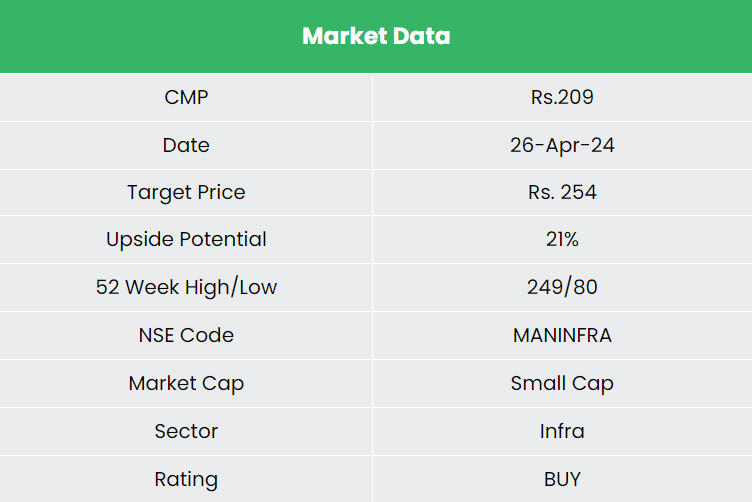

- BUY score with a goal value of Rs.254 30x FY25E EPS.

Dangers

- Geographic focus in Mumbai and MMR might result in gross sales influence as a consequence of delays or stock accumulation.

- An increase in enter prices and regulatory modifications might have an effect on margins and money stream.

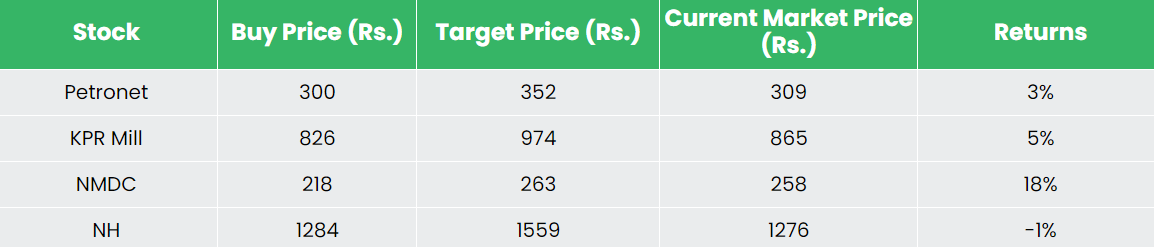

Recap of our earlier suggestions (As on 26 Apr 2024)

Different articles chances are you’ll like

Publish Views:

86

[ad_2]