{kind=link}

[ad_1]

A generally used measure of market liquidity is market depth, which refers back to the amount of securities market members are keen to purchase or promote at explicit costs. The market depth of U.S. Treasury securities, specifically, is assessed in lots of analyses of market functioning, together with this Liberty Avenue Economics submit on liquidity in 2023, this text on market functioning in March 2020, and this paper on liquidity after the World Monetary Disaster. On this submit, we overview the various measurement selections that go into depth calculations and present that inferences in regards to the evolution of Treasury market depth, and therefore liquidity, are largely invariant with respect to those selections.

The place Can One Discover Depth?

The amount of securities market members are keen to purchase and promote at varied costs shouldn’t be absolutely seen. A typical method for a “buy-side” investor, comparable to a mutual fund, to commerce a U.S. Treasury safety is for it to contact a number of sellers (both bilaterally or through a request-for-quote platform) indicating the amount it’s hoping to commerce. Every seller will often reply with the value at which it’s keen to take the opposite facet of the commerce and the investor will then usually select essentially the most enticing value for execution. On this situation, the costs at which sellers are keen to purchase or promote a given amount of a safety are solely revealed after the sellers are contacted, and solely to that buyer and at that instantaneous of time.

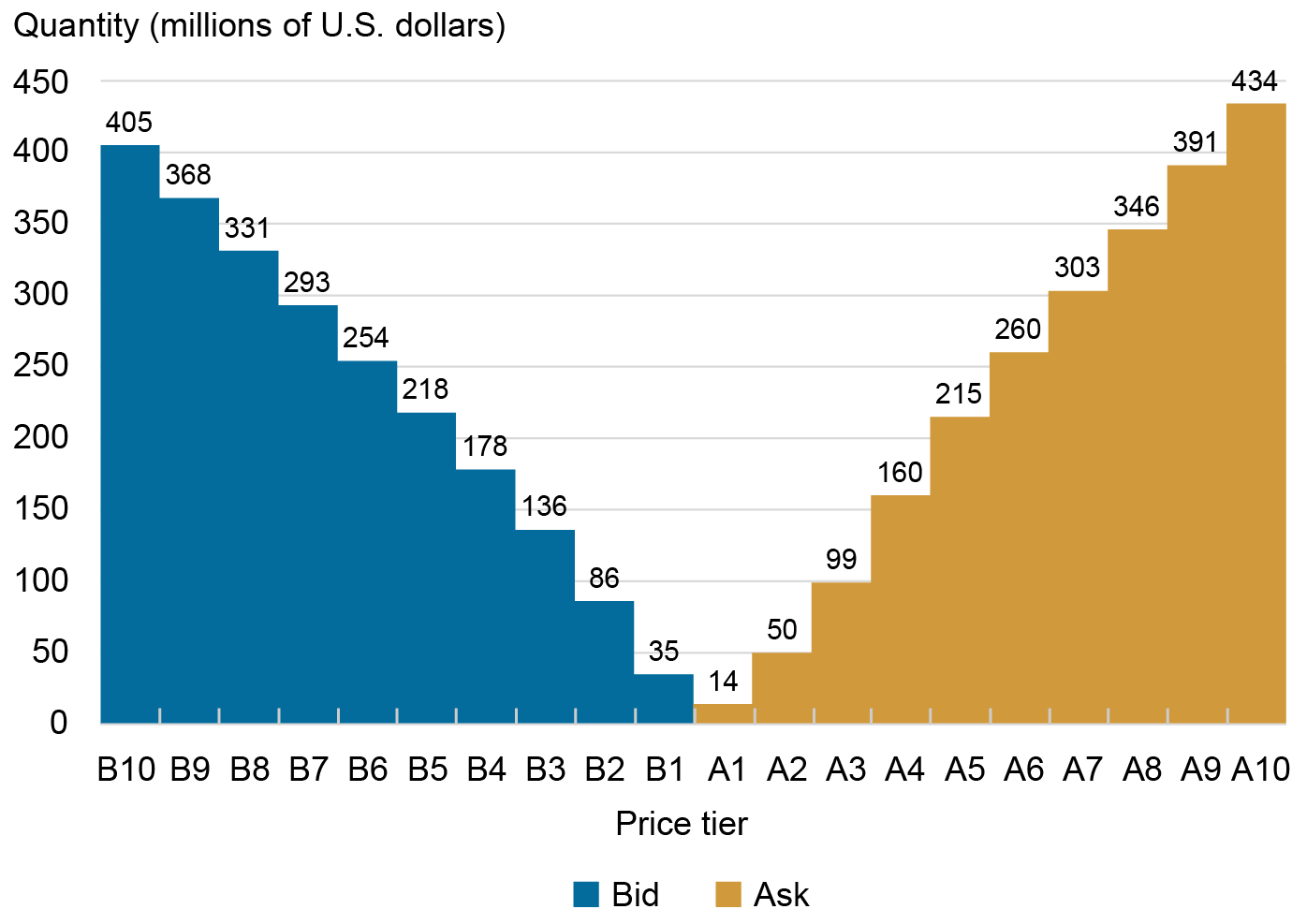

Treasury market depth for sure securities might be noticed within the interdealer dealer (IDB) market, through which sellers and sure different market members commerce amongst themselves. IDBs function central restrict order books, which gather and consolidate buying and selling pursuits from platform members. A snapshot of an IDB’s standing restrict orders for a specific time and safety is plotted under. It reveals that platform members stood prepared to purchase $35 million of the on-the-run (most not too long ago auctioned) five-year word at the most effective bid value and promote $14 million of the word at the most effective ask (or supply) value. Extra purchase (and promote) portions have been out there at barely decrease (and better) costs.

Snapshot of Order Ebook Depth

Notes: The chart plots a snapshot of combination order-book depth for the on-the-run five-year word on December 15, 2023 at 10:30 a.m. The aggregation implies that the $14 million provided at the most effective ask value (A1) is added to the $36 million provided on the second greatest ask value (A2) to get the $50 million complete provided on the second greatest ask value or higher. The worth distinction between adjoining value tiers, together with the most effective bid (B1) and the most effective supply (A1) on this chart, is one tick, which is ¼ of 1/32 of some extent for the five-year word (the place some extent equals 1 % of par). Depth is measured in thousands and thousands of U.S. {dollars} par.

What Does the Depth Knowledge Present?

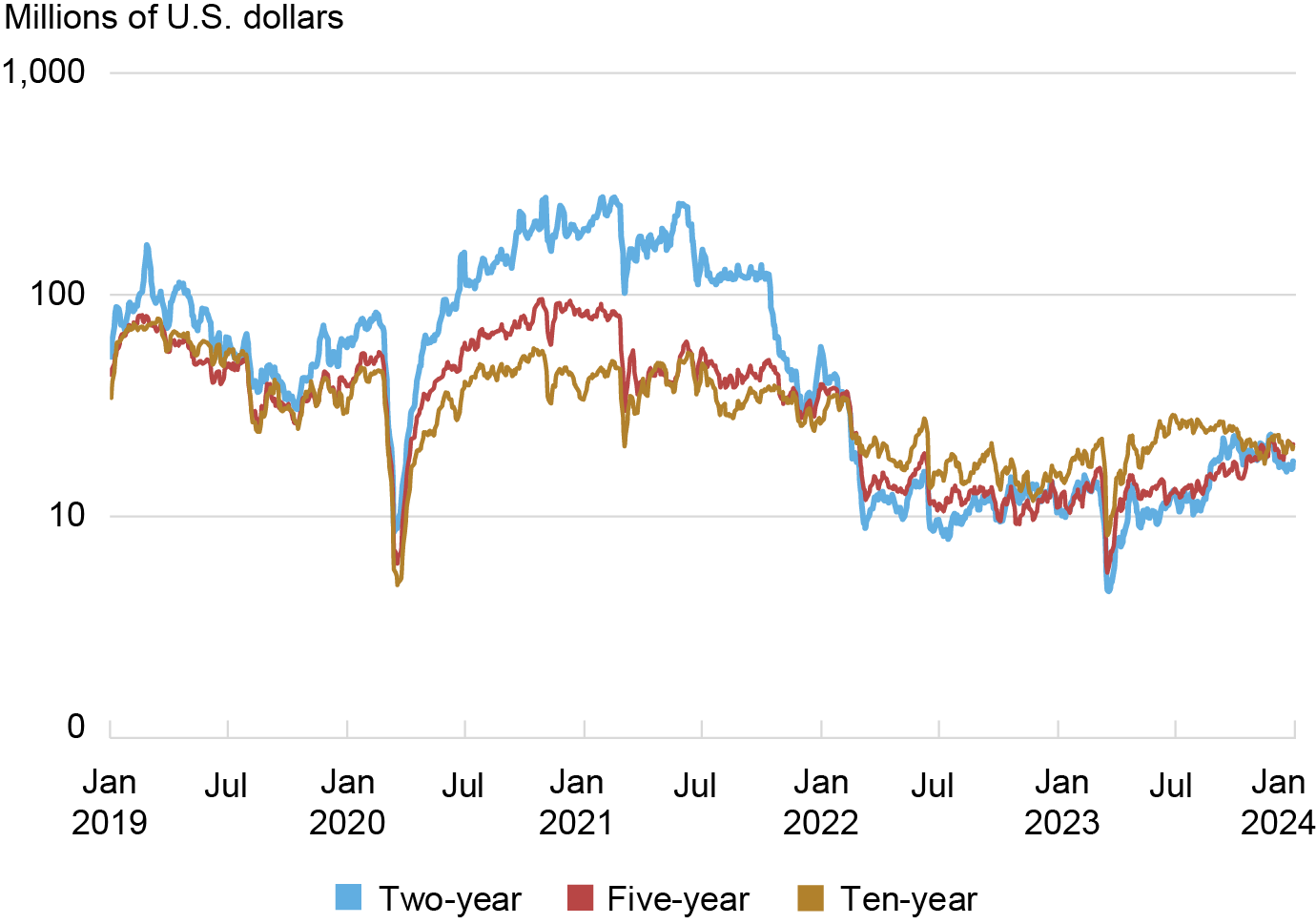

Order guide knowledge present appreciable variation in depth over time, as proven within the chart under. Depth plunged amid the COVID-related disruptions of March 2020, recovered thereafter, decreased once more in late 2021 and 2022 amidst uncertainty in regards to the anticipated path of rates of interest, after which declined abruptly in March 2023 after the failures of Silicon Valley Financial institution and Signature Financial institution. The chart additionally reveals that the evolution of depth throughout securities is very correlated, however that there’s some variation relying on safety. Since rapidly recovering from the March 2023 disruptions, for instance, depth has been trending upward for many on-the-run notes and bonds (suggesting improved market liquidity), however comparatively secure for the ten-year word.

Order Ebook Depth Plunged in March 2020 and March 2023

Notes: The chart plots five-day shifting averages of common each day depth for the on-the-run two-, five-, and ten-year notes from January 1, 2019 to December 31, 2023. Knowledge are for order guide depth on the inside tier, averaged throughout the bid and supply sides. For instance, depth is calculated as $24.5 million for the order guide snapshot plotted above ($24.5 million = [$14 million + $35 million]/2). Depth is measured in thousands and thousands of U.S. {dollars} par and plotted on a logarithmic scale.

Selections, Selections, Selections

Many measurement selections go into the previous chart. Some are frequent to the calculations of many liquidity measures, however may need explicit salience for depth, whereas others are distinctive to depth. In the remainder of the submit, we discover how these selections have an effect on the extent of calculated order guide depth and particularly inferences about adjustments in depth and therefore market liquidity over time.

Variety of Tiers

One key resolution considerations the variety of value tiers over which depth is aggregated. This Employees Report and the previous chart plot depth at the most effective (or inside) bid and supply costs, this report plots depth on the inside three value tiers, and this text plots depth on the inside 5 value tiers. In fact, depth is bigger when aggregation happens over the next variety of value ranges, as proven within the desk under (and the primary chart above).

Depth Will increase with the Variety of Value Tiers over Which It Is Aggregated

| Safety | |||

| No of Value Tiers | Two-12 months | 5-12 months | Ten-12 months |

| One | 72 | 37 | 33 |

| Three | 278 | 158 | 145 |

| 5 | 446 | 256 | 237 |

| Ten | 740 | 446 | 426 |

Notes: The desk reviews common order guide depth aggregated over one, three, 5, and ten value tiers for the on-the-run two-, five-, and ten-year notes. Depth is first averaged over every buying and selling day and throughout the bid and supply sides, after which over the January 1, 2019 to December 31, 2023 pattern interval. It’s measured in thousands and thousands of U.S. {dollars} par.

That mentioned, the time sequence patterns of depth are primarily the identical whatever the variety of tiers examined. The desk under thus reveals correlation coefficients shut to at least one for common each day depth measured throughout various numbers of value tiers for the five-year word. An identical sample is noticed for the opposite on-the-run notes and bonds (as proven within the appendix), though correlations are considerably greater for longer-term securities and considerably decrease for shorter-term ones.

Depth Evolution Is Largely Invariant to the Variety of Value Tiers over Which It Is Aggregated

| One | Three | 5 | Ten | |

| One | 1.000 | |||

| Three | 0.977 | 1.000 | ||

| 5 | 0.962 | 0.997 | 1.000 | |

| Ten | 0.939 | 0.987 | 0.995 | 1.000 |

Notes: The desk reviews correlation coefficients amongst common each day depth aggregated over one, three, 5, and ten value tiers for the on-the-run five-year word over the January 1, 2019 to December 31, 2023 pattern interval. Depth is averaged throughout the bid and supply sides.

Bid vs. Ask Depth

A second resolution considerations whether or not one ought to have a look at bid depth, ask depth, or the typical (or sum) of the 2. Most analyses have a look at the typical (or sum) of bid and ask depth and don’t say something about variations between the bid and supply sides (a few exceptions are right here and right here). In observe, common bid and ask depth are fairly comparable (e.g., $36.4 million and $36.6 million for the five-year word from January 2019 to December 2023), regardless that the metrics can differ meaningfully at any given time limit (as proven within the first chart). Furthermore, the time sequence patterns of common each day bid and supply depth are virtually similar (as proven by the excessive correlation coefficients reported within the appendix).

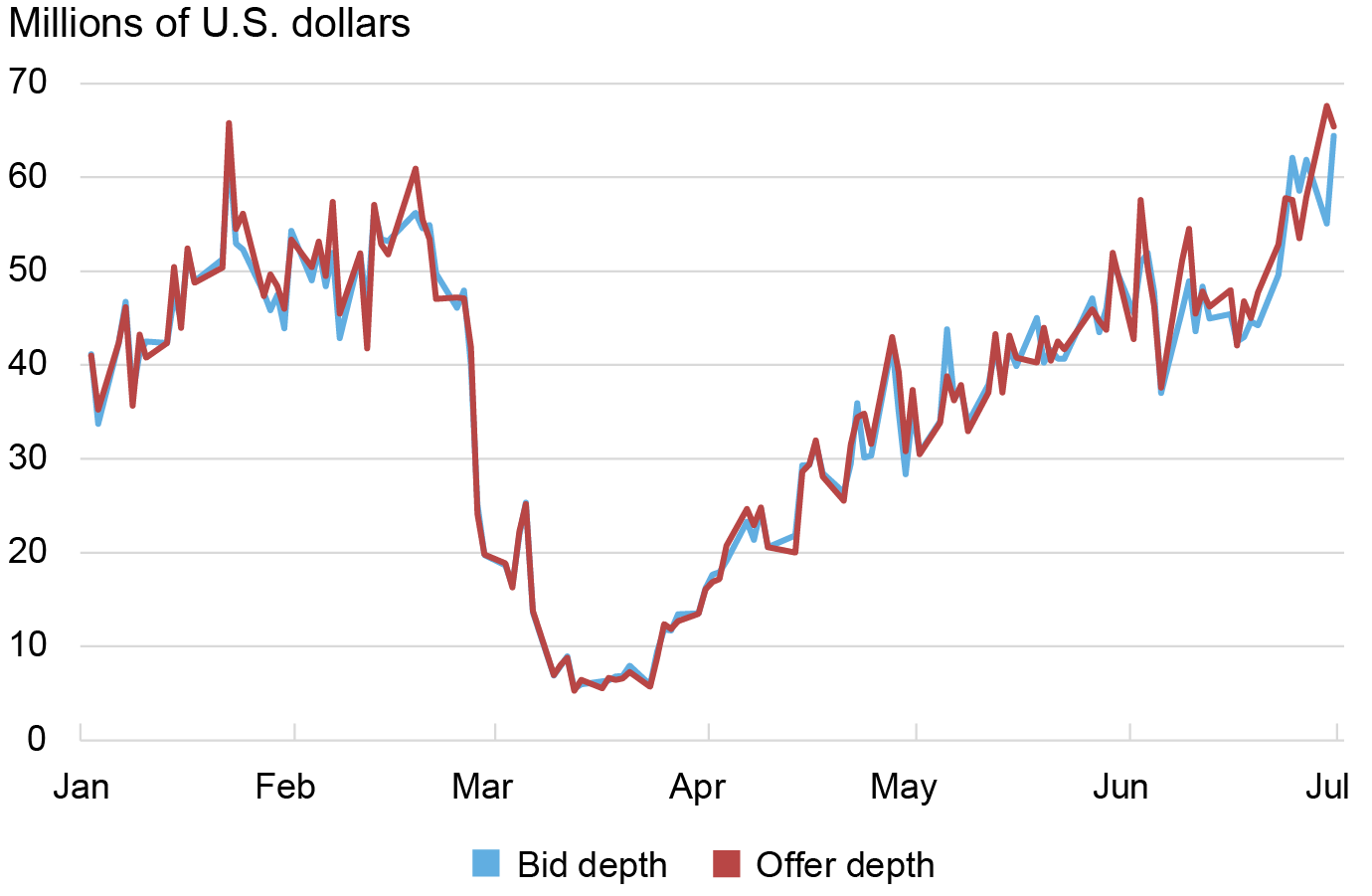

Even in March 2020, when large buyer promoting overwhelmed sellers’ capability to intermediate trades (see right here and right here), common each day depth within the interdealer market was nearly the identical on the bid and supply sides, as proven within the subsequent chart. This paper on liquidity and volatility within the U.S. Treasury market additionally notes that varied depth variables (bid and ask, on the first tier and the subsequent 4 tiers) exhibit comparable variation over time.

Bid and Supply Depth Developed Equally Round March 2020

Notes: The chart plots common each day bid and ask depth for the on-the-run five-year word from January 1, 2020 to June 30, 2020. Knowledge are for order guide depth on the inside tier. Depth is measured in thousands and thousands of U.S. {dollars} par.

To make certain, bid and supply depth could also be individually helpful inputs for buying and selling selections or analyses of market disruptions (comparable to these on October 15, 2014 or February 25, 2021) however for monitoring common depth at a each day horizon or longer, there appears to be little data in a single metric that’s not within the different.

New York vs. World Buying and selling Hours

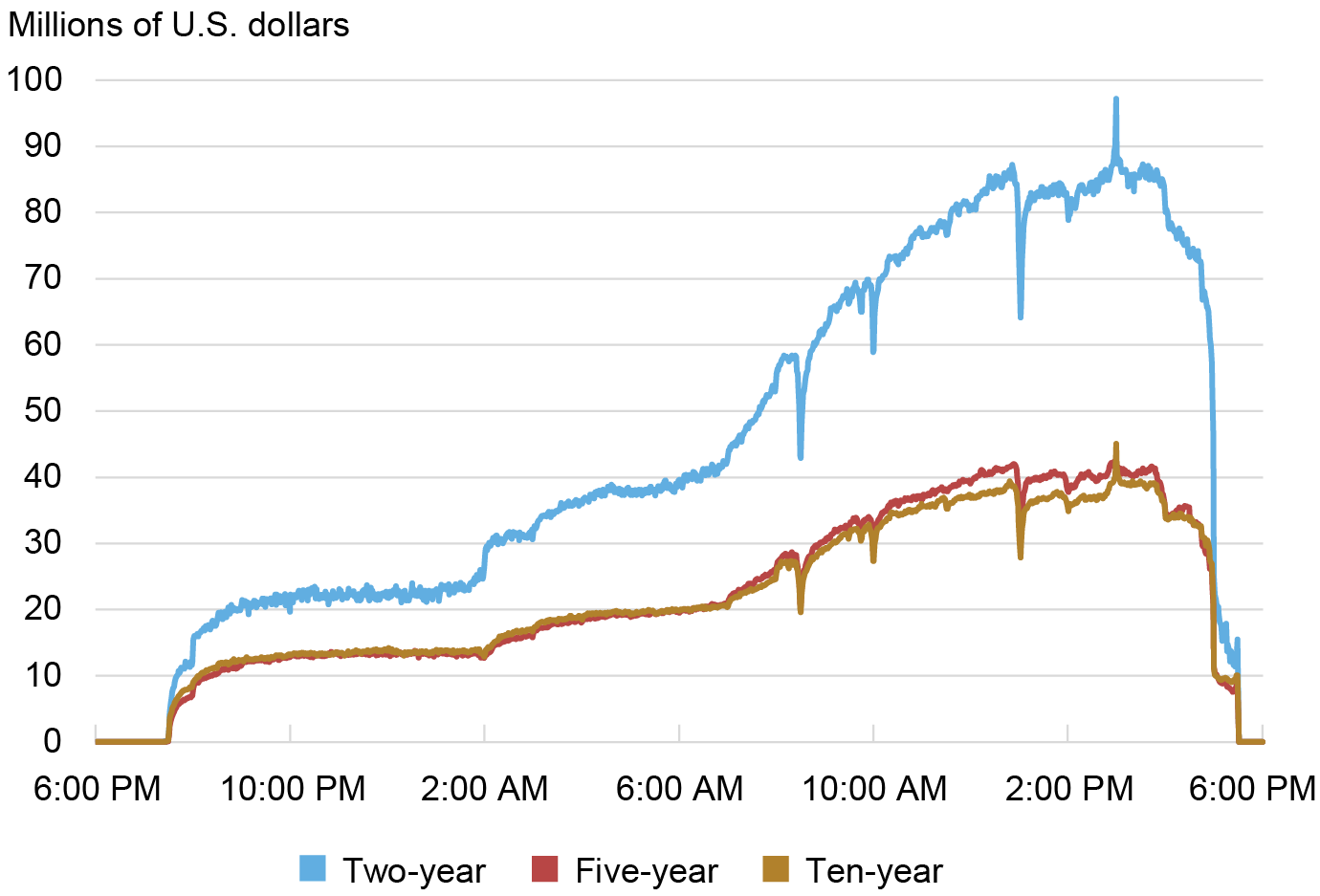

A 3rd consideration when summarizing depth is the buying and selling hours over which depth is averaged. Treasuries commerce practically around the clock in the course of the week, as described on this Financial Coverage Evaluate article. Liquidity is appreciably higher (and buying and selling exercise greater) in the course of the extra energetic New York buying and selling hours, roughly 7 a.m. to five p.m., as proven within the subsequent chart. It follows that common each day depth is greater if the calculations are accomplished over New York buying and selling hours solely (as they’re on this submit). That mentioned, the time sequence patterns of common each day depth are nearly indistinguishable whether or not depth is calculated over New York buying and selling hours or the complete international buying and selling day.

Depth Is Increased throughout New York Buying and selling Hours

Notes: The chart plots common depth by minute over the worldwide buying and selling day for the on-the-run two-, five-, and ten-year notes. Knowledge are for order guide depth on the inside tier, averaged throughout the bid and supply sides, then averaged for every minute throughout the buying and selling days from January 1, 2019 to December 31, 2023 when each the U.Okay. and the U.S. have been on daylight saving time (so that point variations between Japan, the U.Okay., and the U.S. are fixed for this evaluation). Depth is measured in thousands and thousands of U.S. {dollars} par.

Time vs. Tick-Weighting

One different resolution considerations the weighting scheme for calculating common depth. “Time-weighted” implies that depth for every time interval will get equal weight. “Quantity-weighted” implies that depth for every time interval is weighted by quantity in that interval, and “tick-weighted” (used on this submit) implies that depth at every change within the restrict order guide (which might be outlined varied methods) will get the identical weight. On condition that buying and selling exercise varies a lot over the worldwide buying and selling day, common depth essentially varies relying on the tactic of calculation. Once more, nevertheless, the evolution of common each day depth is sort of similar whether or not calculations are time-weighted or tick-weighted.

Summing Up

Many selections go into the calculation of market depth from order guide knowledge. Though these selections have significant results on the typical stage of computed depth, they’ve little impact on inferences about Treasury market liquidity comprised of adjustments in each day depth over time. Whether or not it’s bid vs. supply facet, inside tier vs. many tiers, or New York hours vs. all hours, market depth has been challenged lately by the pandemic, financial institution failures, and rate of interest uncertainty typically, and bears watching (together with different liquidity measures) going ahead.

Michael J. Fleming is the top of Capital Markets Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Isabel Krogh is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Claire Nelson is an economics Ph.D. candidate at Princeton College.

Methods to cite this submit:

Michael Fleming, Isabel Krogh, and Claire Nelson, “Measuring Treasury Market Depth,” Federal Reserve Financial institution of New York Liberty Avenue Economics, February 12, 2024, https://libertystreeteconomics.newyorkfed.org/2024/02/measuring-treasury-market-depth/.

Disclaimer

The views expressed on this submit are these of the creator(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the creator(s).

[ad_2]