{kind=link}

[ad_1]

How can we precisely measure adjustments in residing requirements over time within the presence of worth inflation? On this put up, I focus on a novel and easy methodology that makes use of the cross-sectional relationship between earnings and household-level inflation to assemble correct measures of adjustments in residing requirements that account for the dependence of consumption preferences on earnings. Making use of this methodology to information from the U.S. suggests probably substantial mismeasurements in our accessible proxies of common progress in client welfare within the U.S.

These insights and outcomes are based mostly on my latest analysis paper coauthored with Xavier Jaravel of the London College of Economics, which is forthcoming on the Quarterly Journal of Economics.

Background

Financial concept exhibits that we will approximate adjustments in residing requirements utilizing easy formulation often called worth and amount indices. These indices mix noticed information on adjustments within the portions of what we eat and the costs of these objects, and are broadly utilized by statistical workplaces world wide to assemble measures of total inflation in the price of residing and progress in residing requirements. Nonetheless, this strategy hinges on an important assumption—that the composition of what we need to purchase doesn’t shift when our incomes do (see, for instance, Diewert 1993). Sadly, this simplifying assumption, often called homotheticity or earnings invariance, doesn’t match up with a bunch of real-world proof on the dependence of consumption patterns on client earnings, going way back to the work of Engel (1857). Current proof on inflation inequality—the robust relationship between earnings and household-level measures of inflation—underscores the significance of this downside.

Perception and Methodology

A conceptually coherent option to measure residing requirements is to repair a set of costs and calculate the financial expenditure wanted, beneath these costs, to attain any stage of client welfare because it adjustments over time. Allow us to check with this idea as actual consumption, to tell apart it from the nominal expenditure of the buyer beneath altering costs. As an illustration, think about a case the place all costs rise on the similar 2 % charge from one 12 months to the following on account of normal inflation. Right here, a client whose nominal expenditure has risen by 5 % solely experiences a 3 % improve in actual consumption, if we repair the costs within the preliminary or the ultimate 12 months. The important thing query is tips on how to calculate the corresponding measures of inflation and actual consumption progress in real-world settings during which adjustments in costs differ throughout completely different items and companies.

If client preferences are income-invariant, everybody consumes the identical basket of products and companies no matter their earnings stage. Over time, households regulate whether or not to eat roughly of every good or service based mostly on how its worth adjustments relative to others, however these changes are the identical for everybody. Standard worth indices inform us tips on how to common these worth adjustments utilizing the expenditure shares of various items and companies, and concept tells us we have to deflate the expansion in nominal expenditure based mostly on the worth of this common, which is the usual measure of inflation.

In actuality, households select completely different baskets of products and companies that systematically rely, amongst different issues, on their earnings. Subsequently, we discover completely different inflation measures for various households after we compute the worth indices utilizing every family’s personal expenditure shares, one thing that ought to not occur beneath the traditional assumption of earnings invariance. Within the information, we regularly discover decrease inflation measures for richer households, which means that costs rise extra slowly for luxuries—i.e., objects which can be extra closely bought by richer customers (see, for instance, Hobijn and Lagakos 2005, McGranahan and Paulson 2006, Jaravel 2019, Avtar et al. 2022, and Chakrabarti et al. 2023). Subsequently, this stuff have gotten comparatively cheaper than the others over time. This suggests that, if we repair the preliminary costs as our foundation for measuring actual consumption, households that have rising earnings will probably be shifting their consumption towards objects which can be accumulating relative worth declines. In different phrases, sustained inflation bias towards requirements—items and companies favored by poorer households—signifies that we’d like comparatively decrease charges of progress in nominal phrases to take care of the identical charge of progress in actual consumption. Thus, when earnings is rising, customers are literally higher off than that instructed by all accessible measures of actual consumption. The standard measures of inflation and actual consumption miss this mechanism altogether. That is even true of the newer work on inflation inequality, partially cited above, that depends on household-specific worth index formulation however doesn’t explicitly account for earnings dependence.

Because it seems, there’s a comparatively straightforward repair for this downside. We will right for the consequences of this earnings dependence in preferences just by estimating the connection between family earnings and household-specific worth indices. The slope of this relationship results in a correction issue that we have to apply to the nominal expenditure progress after it’s deflated by the family’s personal worth index. This methodology is pretty straightforward to implement and solely requires entry to broadly accessible surveys of consumption expenditure on the family stage. Furthermore, it may be generalized to increase to different family traits, equivalent to age, household dimension, and schooling, that (1) matter for the composition of their consumption expenditure, and (2) probably differ over time on the family stage.

Utility to the U.S. Information

Within the paper, we apply our strategy to information from the US and quantify the magnitude of the bias in standard measures of actual consumption progress that ignore the consequences of earnings dependence in family preferences. We construct a brand new linked dataset offering worth adjustments and expenditure shares at a granular stage from 1955 to 2019, throughout the completely different percentiles of family (pretax) earnings. This dataset combines a number of information sources, primarily drawing from disaggregated information sequence accessible from the Client Value Index (CPI) and the Client Expenditure Survey (CEX). This new linked dataset permits us to offer proof on the inequality in inflation over a very long time horizon, thus extending prior estimates which have targeted on shorter time sequence.

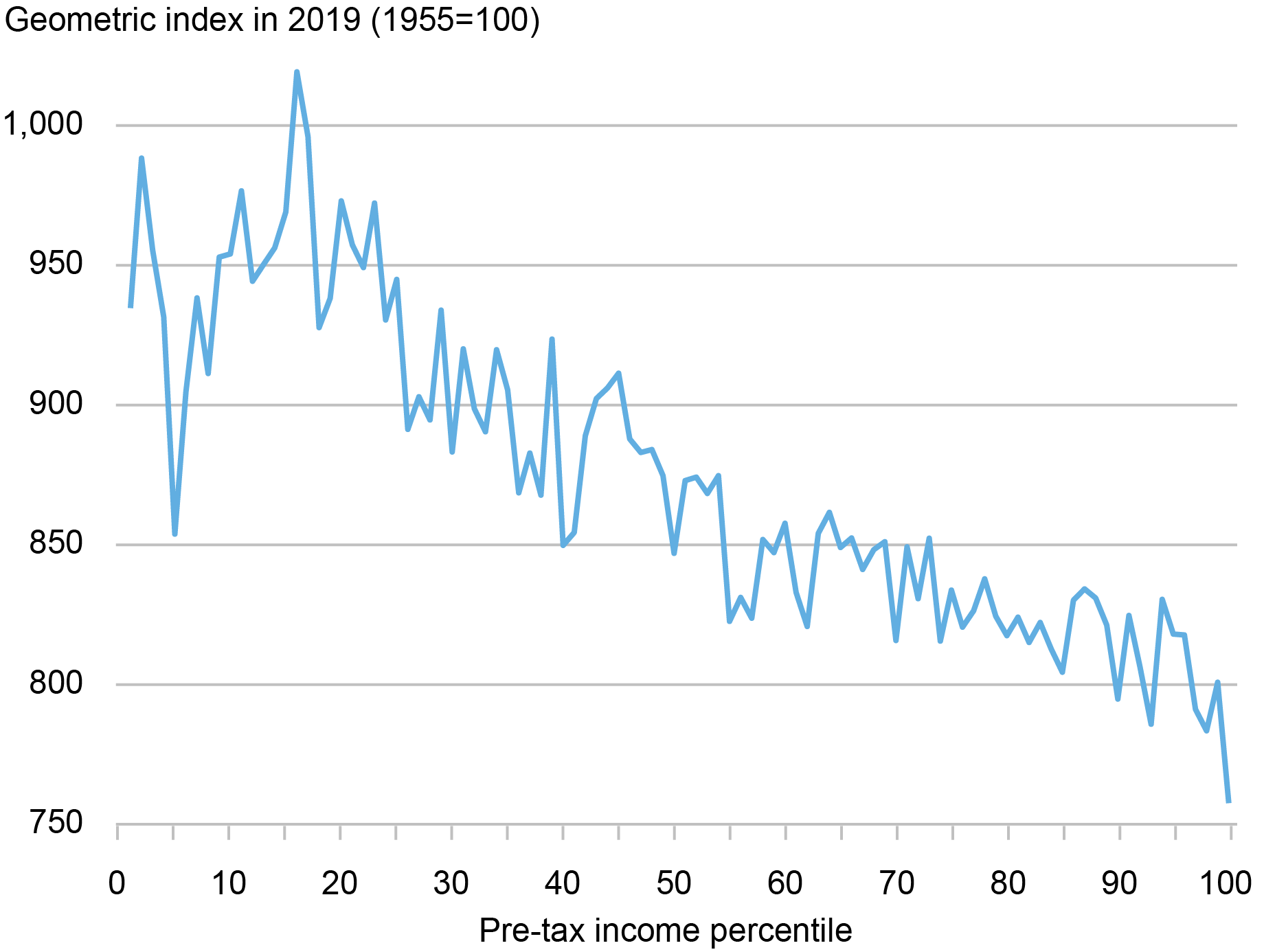

Computing inflation utilizing income-percentile-specific worth index formulation, we discover that inflation inequality is a long-run phenomenon. As an illustration, because the chart beneath exhibits, we discover that cumulative inflation from 1955 to 2019 varies considerably for households with completely different ranges of earnings: whereas costs have inflated by an element of round 10 for the underside earnings teams, they’ve inflated by an element nearer to eight on the prime of the earnings distribution. The hole in inflation skilled by completely different earnings percentiles is sizable when in comparison with the general dimension of inflation over the interval. As such, after we look into the previous from the attitude of at present’s costs, we observe that (1) households had been on common poorer sixty-five years in the past—that’s, that they had stronger preferences for requirements; and (2) requirements had been cheaper relative to luxuries. These empirical patterns suggest that client welfare was larger sixty-five years in the past when accounting for the dependence of preferences on earnings.

Inflation Inequality over the Lengthy Run

Supply: Writer’s calculations based mostly on the historic linked CEX-CPI information.

Notes: This chart exhibits the patterns of inflation inequality within the information. It exhibits the cumulative inflation charges between 1955 and 2019 by pretax earnings percentiles.

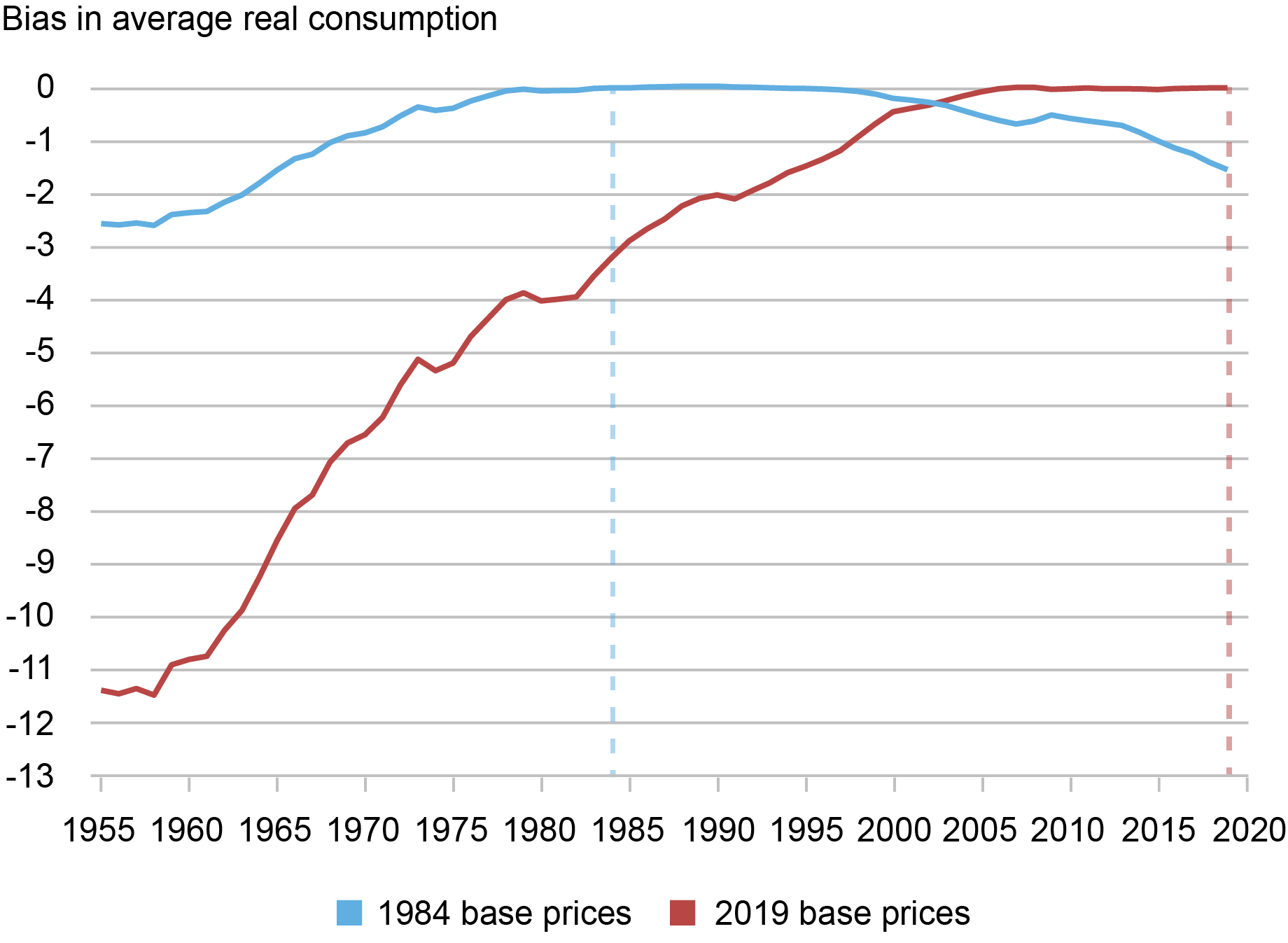

Once we apply our new methodology to this information, we discover that the magnitude of the correction in measured welfare progress as a result of impact of income-dependent preferences might be giant. For instance, as the chart beneath exhibits, by fixing costs in 2019 as the premise of defining actual consumption, we discover that the uncorrected measure underestimates common actual consumption (per family) in 1955 by about 11.5 %. Word that, by definition, the error is zero within the base 12 months and accumulates over time as we transfer in time—on this case backward—away from the bottom 12 months. For comparability, we additionally present the outcomes if we repair costs in 1984. On this case, the bias is smaller just because it accumulates over a shorter time interval, as we transfer away from the bottom 12 months in our information.

Bias in Standard Measures of Common U.S. Actual Consumption (1955-2019)

Supply: Writer’s calculations based mostly on the historic linked CEX-CPI information.

Notes: This chart stories the biases within the stage of common actual consumption per family in standard measures of actual consumption, when put next towards the corrections implied by our methodology, beneath two selections for the fastened costs as the bottom for calculation of actual consumption: costs in 1984 and in 2019.

In fact, bias in measuring the extent of actual consumption results in corresponding biases within the estimated progress. Because the chart above already signifies, if we repair costs in the latest 12 months (2019), the traditional estimates overestimate the speed of progress in common actual consumption as a result of adverse bias within the ranges. Particularly, the uncorrected measure of cumulative actual consumption progress is 270 % over all the 1955-2019 interval, or 2.07 % progress yearly. In distinction, with our correction for earnings dependence and beneath 2019 base costs, cumulative consumption progress falls to 232 %, or an annualized progress charge of 1.89 % per 12 months. Thus, on this case we discover that the annual progress charge from 1955 to 2019 is lowered by 18 foundation factors (2.07 % − 1.89 %).

Word that, for the reason that standard measure all the time underestimates the stage of actual consumption, the signal of the error in measured progress of actual consumption is dependent upon the selection of the bottom costs. As an illustration, if we as an alternative repair 1984 costs as our base, the chart exhibits that the traditional measures in truth underestimate the expansion in actual consumption between 1984 and 2019. In different phrases, since preferences are income-dependent, measured progress in actual consumption ought to in precept rely upon the selection of fastened costs to specific the measure.

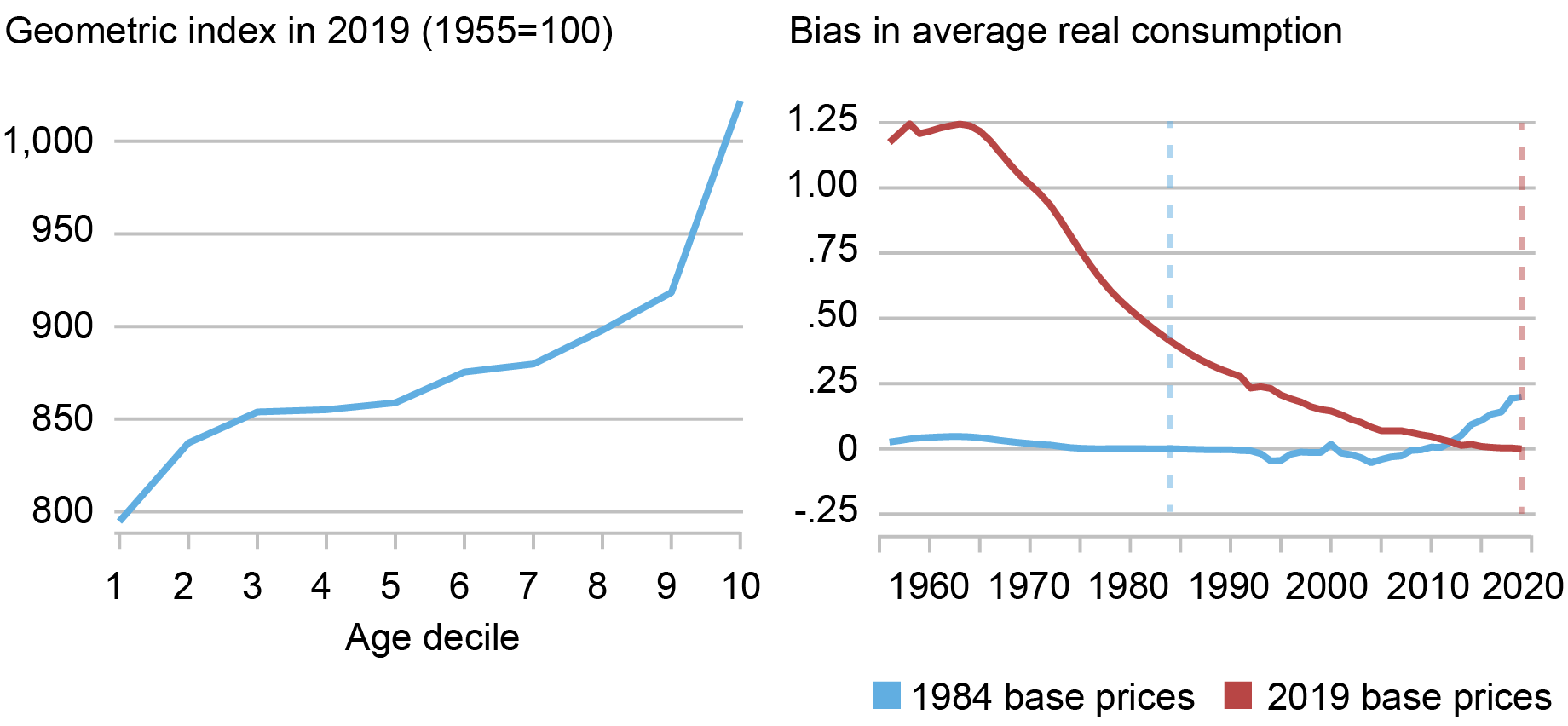

Lastly, we additionally apply our generalized methodology to quantify the adjustment to common actual consumption implied by client growing old in the US. On this case, we reconstruct our measures of inflation by deciles of age and earnings by, first, defining ten deciles of the (pretax) earnings and, then, computing ten age deciles inside every earnings decile. Utilizing this information, because the chart beneath illustrates, we doc a robust constructive relationship between client age and inflation, which alters the measurement of actual consumption as a result of the typical client age will increase over time. We discover that the implied changes to actual consumption are economically significant however a lot smaller than the correction on account of earnings dependence, which justifies our give attention to the latter.

Client Growing older and Actual Consumption (1955-2019)

Sources: Writer’s calculations based mostly on the historic linked CEX-CPI information.

Notes: The left panel of the chart stories the cumulative inflation in the US, from 1955 to 2019, for every decile of age. The proper panel stories the implied bias within the common stage of actual consumption per family in standard measures of actual consumption, when put next towards the corrections implied by our methodology on account of growing old, beneath two selections for the fastened costs as the bottom for calculation of actual consumption: costs in 1984 and in 2019.

Conclusion

Our outcomes could have essential implications for the way in which during which nationwide statistical companies world wide assemble measures of inflation and actual financial worth. Particularly, the empirical outcomes introduced above counsel an strategy that the Bureau of Labor Statistics (BLS) can use, based mostly on already accessible information, to assemble improved measures of actual consumption progress and inequality within the U.S. Along with bettering the measurement of long-run progress and inflation inequality, our new strategy can have essential coverage implications, such because the indexation of the poverty line and a extra environment friendly concentrating on of welfare advantages. This strategy additionally gives a blueprint for distributional nationwide accounts (Piketty et al. 2018) that account for inflation inequality and earnings dependence in family preferences.

Danial Lashkari is a analysis economist in Labor and Product Market Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Tips on how to cite this put up:

Danial Lashkari, “Measuring Value Inflation and Development in Financial Properly‑Being with Revenue‑Dependent Preferences,” Federal Reserve Financial institution of New York Liberty Avenue Economics, January 8, 2024, https://libertystreeteconomics.newyorkfed.org/2024/01/measuring-price-inflation-and-growth-in-economic-well-being-with-income-dependent-preferences/.

Disclaimer

The views expressed on this put up are these of the writer(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).

[ad_2]