{kind=link}

[ad_1]

Lambert right here: Hopefully a subject of purely educational curiosity!

By Silvia Marchesi, Professor of Economics College of Milano Bicocca, and Giovanna Marcolongo, Postdoctoral Fellow, Crime and Legislation Financial Evaluation unit Bocconi College. Initially revealed at VoxEU.

A lot of the present analysis on offshore monetary centres has targeted on the roles of tax havens in superior economies, and fewer is understood in regards to the case of growing nations, particularly after a monetary disaster. This column exhibits that tax havens not solely facilitate tax evasion and corruption in ‘regular instances’, additionally they harbour funds throughout financial crises, slowing down restoration. That is significantly related for low income-countries characterised by excessive inequality. The diversion of capital to tax havens by the richest shifts the burden of the restoration onto the remainder of the inhabitants, additional exacerbating inequality.

Capital flight options prominently in up to date debates about financial growth. In growing nations, capital is comparatively scarce and the identical home buyers could favor to find a part of their belongings outdoors of the nations’ borders (e.g. Cuddington 1986, Eaton 1987). Ranging from the good monetary liberalisation within the Nineteen Eighties, wealth has been transferring throughout the borders at increased frequency, typically reaching offshore locations characterised by a close-to-zero tax fee. Offshore capital shouldn’t be employed productively within the nation of origin. Moreover, when offshore wealth is hidden from the tax authorities of the nation of origin, or when regulation – resembling bilateral tax agreements – shouldn’t be in place or not enforced, the nation of origin can not levy any taxes on it. This concern turns into extra regarding for low- and middle-income nations, the place the rule of regulation and state capacities are sometimes weaker.

In keeping with Zucman (2013), about 8% of all world monetary wealth reached tax havens, equivalent to a tax income lack of $190 billion. Newer proof means that companies e-book round 7% of their world income in tax havens, leading to important income losses (Zucman and Wier 2022). This subtraction of assets, being it direct (by way of capital flight) or oblique (by way of non-levied taxes) turns into much more regarding at instances of monetary crises, when productive use of home assets might foster restoration. If, on the excessive, the motion of capital towards tax havens accelerates much more throughout a monetary disaster, then two units of unfavorable penalties derive: slower restoration on one aspect, and better burden of the disaster on poorer residents on the opposite. Certainly, entry to tax havens is skewed closely in direction of the highest-income people (Alstadsaeter et al. 2018, 2019).

Our Examine

In our current paper (Marchesi and Marcolongo 2023), we give attention to the cross-country relationship between monetary (i.e. banking and sovereign debt) crises and ‘hidden wealth’. We measure hidden wealth utilizing information on financial institution deposits in offshore monetary centres offered by the Financial institution of Worldwide Settlements (BIS) and, as robustness, information from the Offshore Leaks Database (the Panama Papers and subsequent leaks such because the Pandora Papers and Paradise Papers) measuring the chance of observing the incorporation of shell firms in tax havens.

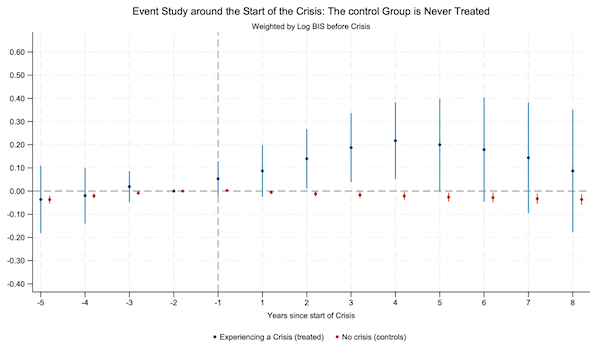

Determine 1 Monetary disaster: Funds to tax havens

Notes: Stacked difference-in-differences. It exhibits estimates of funds flowing to tax havens round a monetary disaster. Markers characterize 90% confidence intervals.

Analysing 144 growing nations, utilizing quarterly information and each a two-way mounted results (TWFE) and stacked difference-in-differences methodology, we estimate the impact of monetary crises on financial institution deposits in tax havens over the 1977-2020 interval. We offer empirical proof of a hyperlink between the start of a monetary disaster and a rise in offshore financial institution deposits in the identical interval. Utilizing an event-study evaluation, we detect a rise in deposits of about 20% three years after the start of a disaster (Determine 1). The impact is economically sizeable: the common improve of deposits into tax havens corresponds to about $1 billion through the disaster (equivalent to barely lower than 1% of a growing nation’s common annual GDP). The impact doesn’t persist past the tip of the disaster.

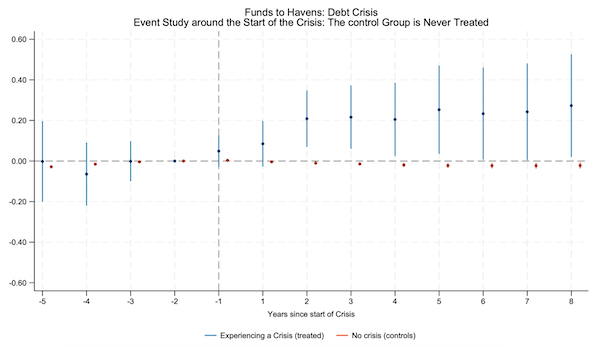

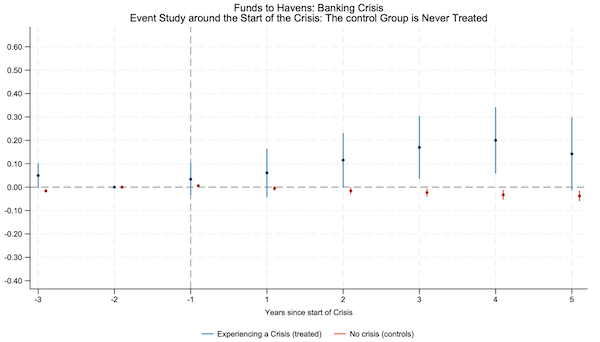

Given the completely different traits between sovereign debt and banking crises, we discover whether or not the flows of funds to tax havens differ throughout these two forms of shocks. We discover the outcomes are qualitatively comparable throughout banking and debt crises, though the rise in financial institution deposits after a sovereign debt default is extra persistent (Determine 2).

Determine 2 Sovereign debt and banking crises and funds to tax havens

a) Sovereign debt crises

b) Banking crises

Notes: Stacked difference-in-differences. Panel a exhibits funds to tax havens throughout a sovereign debt disaster, panel b exhibits funds to tax havens throughout a banking disaster. Markers characterize 90% confidence intervals.

So far as doable mechanisms are involved, we examine whether or not the 2 principal drivers of funds to tax havens steered by the literature – particularly, tax evasion and corruption – clarify the rise in hidden wealth throughout monetary crises. We doc no improve within the efficient tax on capital following the beginning of a disaster (tax charges are sometimes very low in low-income nations), whereas we discover proof of a rise within the expropriation danger, which is usually increased in nations with extra fragile establishments.

With out Contemplating Tax Havens We Underestimate Inequality

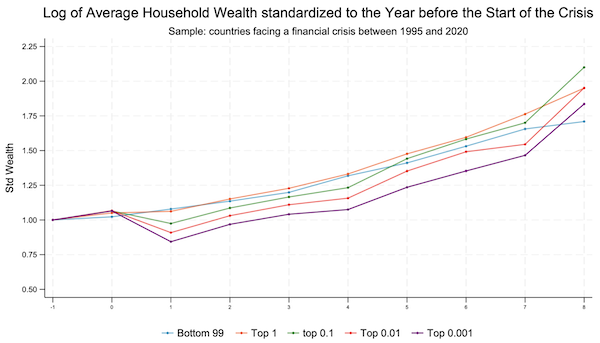

In the end, as emphasised by Alstadsaeter et al. (2019), you will need to have in mind the position tax heavens play in underestimating inequality. When testifying the implications of a monetary disaster on inequality, you will need to think about each home (noticed) in addition to offshore (hidden) wealth. The truth is, solely the sum of the 2 permits us to assemble a dependable measure of the wealth distribution. We offer suggestive proof of the truth that the bigger the quantities of funds a rustic diverts to tax havens throughout a monetary disaster, the upper the discount within the noticed family wealth of the best quantiles (high 0.01%) of the distribution (Determine 3). We present that this discount shouldn’t be a mechanical byproduct of the home results of the monetary disaster (resembling, for instance, falling costs on monetary belongings). On the identical time, the impact of the monetary disaster on the inhabitants’s (noticed) common wealth decreases progressively as we transfer away from the richest segments of the inhabitants. This reality is in step with the richest segments of the inhabitants harbouring a part of their funds in tax havens.

Determine 3 Dynamic of common wealth by revenue quantiles after the beginning of a monetary disaster

Notes: Standardised wealth of nations experiencing a monetary disaster by completely different percentiles of common wealth over time

Conclusion

We add to earlier works by investigating the connection by monetary crises and hidden wealth. To the most effective of our information, that is the primary time on this literature that the hyperlink is considered. Earlier literature offered measures of internet wealth positions and estimates of offshore tax evasion (Lane and Milesi-Ferretti 2007, Zucman 2013, Johannesen 2014, Johannesen and Zucman 2014). Furthermore, Johannesen and Rijkers (2020), Andersen et al. (2022) and Andersen et al. (2017) have documented that tax havens could be facilitators of corruption. We present that tax havens not solely facilitate tax evasion and corruption in ‘regular instances’, additionally they harbour funds throughout financial crises, slowing down restoration.

Furthermore, whereas a lot of the present analysis has targeted on the roles of tax havens in superior economics, we contribute to this literature by highlighting how tax havens appeal to funds from growing economies as properly, particularly from nations with weak establishments. Particularly, we present that tax havens, in addition to permitting tax and sanction evasion and harbouring the proceeds of legal actions, take in assets at troublesome instances and should result in a downward bias when measuring inequality in a rustic. To attract an entire image of the prices of a monetary disaster and its penalties for inequality, we can not ignore the position of hidden wealth. Because the pandemic and the more moderen geopolitical turmoil have elevated monetary instability, you will need to perceive how a disaster could have an effect on the scale of funds in tax havens, harbouring assets when most wanted and shifting the burden of adjustment on poorer residents.

References accessible on the unique.

[ad_2]