{kind=link}

[ad_1]

Laura and her husband Ethan are from Philadelphia, PA, however have been dwelling in Hanoi, Vietnam for the previous two years. Ethan teaches English literature at a world college and Laura is incomes her Grasp’s diploma in public well being. They’ve liked their time in Vietnam and plan to be there for not less than one other yr, however are much less sure of their plans after that.

Finally, they know they wish to return to the US to be able to be nearer to their households, have kids and purchase a house. Laura is worried they’re falling behind on retirement and gained’t be capable to afford a home as soon as they transfer again stateside. Be a part of me right now as we assist these ex-pats chart a secure future!

What’s a Reader Case Research?

Case Research deal with monetary and life dilemmas that readers of Frugalwoods ship in requesting recommendation. Then, we (that’d be me and YOU, pricey reader) learn by their state of affairs and supply recommendation, encouragement, perception and suggestions within the feedback part.

For an instance, take a look at the final case examine. Case Research are up to date by individuals (on the finish of the publish) a number of months after the Case is featured. Go to this web page for hyperlinks to all up to date Case Research.

Can I Be A Reader Case Research?

There are 4 choices for folk all in favour of receiving a holistic Frugalwoods monetary session:

- Apply to be an on-the-blog Case Research topic right here.

- Rent me for a non-public monetary session right here.

- Schedule an hourlong name with me right here.

→Unsure which possibility is best for you? Schedule a free 15-minute chat with me to be taught extra. Refer a buddy to me right here.

Please word that house is restricted for the entire above and most particularly for on-the-blog Case Research. I do my finest to accommodate everybody who applies, however there are a restricted variety of slots accessible every month.

The Objective Of Reader Case Research

Reader Case Research spotlight a various vary of economic conditions, ages, ethnicities, areas, objectives, careers, incomes, household compositions and extra!

The Case Research collection started in 2016 and, up to now, there’ve been 101 Case Research. I’ve featured of us with annual incomes starting from $17k to $200k+ and internet worths starting from -$300k to $2.9M+.

I’ve featured single, married, partnered, divorced, child-filled and child-free households. I’ve featured homosexual, straight, queer, bisexual and polyamorous individuals. I’ve featured girls, non-binary of us and males. I’ve featured transgender and cisgender individuals. I’ve had cat individuals and canine individuals. I’ve featured of us from the US, Australia, Canada, England, South Africa, Spain, Finland, the Netherlands, Germany and France. I’ve featured individuals with PhDs and folks with highschool diplomas. I’ve featured individuals of their early 20’s and folks of their late 60’s. I’ve featured of us who dwell on farms and folk who dwell in New York Metropolis.

Reader Case Research Tips

I most likely don’t must say the next since you all are the kindest, most well mannered commenters on the web, however please word that Frugalwoods is a judgement-free zone the place we endeavor to assist each other, not condemn.

There’s no room for rudeness right here. The objective is to create a supportive atmosphere the place all of us acknowledge we’re human, we’re flawed, however we select to be right here collectively, workshopping our cash and our lives with optimistic, proactive options and concepts.

And a disclaimer that I’m not a skilled monetary skilled and I encourage individuals to not make critical monetary choices based mostly solely on what one particular person on the web advises.

I encourage everybody to do their very own analysis to find out one of the best plan of action for his or her funds. I’m not a monetary advisor and I’m not your monetary advisor.

With that I’ll let Laura, right now’s Case Research topic, take it from right here!

Laura’s Story

Hello Frugalwoods! My identify is Laura and I’m 32 years outdated. My husband Ethan (38) and I are each from Philadelphia, PA however we have now lived in Hanoi, Vietnam for nearly 2 years now. We don’t at present have any children or pets however would really like just a few of each within the close to future :).

We moved to Hanoi for Ethan’s job as an English literature trainer at a world college. Earlier than shifting right here I labored at a non-profit in Philadelphia for 7 years the place I labored my method up from answering telephones within the name middle to software program engineer, after my firm paid for me to go to coding bootcamp. Studying to code was an superior alternative and I preferred it within the context of the group’s mission however it in the end just isn’t what I wish to do with my life. I’m at present in graduate college full-time pursuing a Masters in Public Well being in Maternal and Youngster Well being and a Certificates in World Well being. I’ve a Bachelors in Public Well being and it feels nice to get again into one thing I’ve at all times been keen about. Faculty is nice, however I’m desperate to get again into the workforce in a job I like!

Laura and Ethan’s Hobbies

Ethan and I’ve a variety of hobbies we get pleasure from independently and collectively. I realized to knit in the course of the pandemic and bought a bit obsessed. I like spending a day watching knitting “podcasts” on Youtube and knitting sweaters and hats for myself and household. I’m an avid reader and I like to go for lengthy walks, do yoga and dance. Ethan can be a giant reader, a runner, and a newly obsessed rock climber. Earlier than we moved to Hanoi, Ethan was part mountain climbing the Appalachian Path each summer time break from educating and we might repeatedly go tenting. We like to journey, which was a giant draw for shifting to Southeast Asia. Within the final yr we’ve: spent a month in Indonesia, met my mother and aunt in South Korea, rock climbed on the seaside in Thailand, feasted on sushi in Japan, and traveled Vietnam from high to backside.

Whereas I really feel like we’re doing fairly effectively financially, we’ve had an intense 5 years since we beginning courting. Inside the first 4 months of assembly Ethan, he made his closing pupil mortgage fee on $80k of debt. I’ve at all times been frugal, however I used to be extra of a squirrel hoarding away financial savings, avoiding my debt. He impressed me to assault my pupil loans and, inside 11 months, I paid off practically $60k of debt. Final yr Ethan bought an accelerated Masters in Training, which was vital for him to keep up his educating certification. Between selecting a price efficient possibility and a few skilled growth funding by work, he solely paid $4k out of pocket. I’m paying out of pocket for my MPH, which after scholarships will run me about $17k over two years. I’m pleased with these accomplishments however it’s felt like some huge cash going out for a protracted stretch.

We’re EXTREMELY debt averse because of paying off tens of hundreds of {dollars} in pupil loans. We aren’t positive precisely after we wish to transfer again to the States however we do know that we’d like to purchase a home when that day comes. We’re frightened of taking out a mortgage, particularly with the excessive present rates of interest.

What feels most urgent proper now? What brings you to submit a Case Research?

We haven’t had a great stretch of us each working good jobs whereas not both paying off debt or paying for graduate college. Whereas Ethan feels good about our funds, I’ve loads of nervousness about cash, which I believe is because of:

- Not at present working

- The cash stress I’ve inherited from my mother and father

I believe as soon as I’m accomplished with grad college and we’re each working and might maximize saving I’ll begin to really feel higher.

I’m additionally nervous concerning the transition to shifting again house in just a few years. We at present have extraordinarily low bills and the considered having to pay a mortgage, purchase a automotive or two, all the things being dearer, and many others and many others is de facto aggravating. I wish to take into consideration methods to melt that blow and make the transition much less jarring.

I’m involved that we haven’t contributed to retirement in practically two years. I’m confused about if we are literally allowed to contribute to the Roth IRAs we have already got. Proper now we have now a great amount of money saved that’s earmarked for a home. I’d like to discover with you, Mrs. Frugalwoods, if it ever would make sense to maintain piling up money to pay for a home outright or if we’re being silly right here.

What’s one of the best a part of your present life-style/routine?

Life in Vietnam is simple! Ethan is well-compensated given the price of dwelling right here and his expat package deal consists of hire and flights house for each of us each summer time. Lecturers are well-respected in Vietnam and the job is mostly much less aggravating than it was again in Philly. He will get a lot of lengthy breaks from college which we have now used to journey internationally and discover throughout Vietnam.

We’ve each been capable of spend money on our hobbies in ways in which we by no means would have beforehand. I’ve a fitness center membership so I can go to bounce and yoga courses 4-5 instances weekly; I’ve a basket of beautiful yarn to knit sweaters and hats and socks. Ethan has a vast mountain climbing fitness center membership and climbs with buddies 3 nights per week. We will get pleasure from exploring our metropolis and feasting on the insane Vietnamese delicacies — a bowl of pho is 75 cents, our favourite vegetarian stall is $2 for a large plate of meals, bowl of soup and inexperienced tea. We hardly ever went out to eat at house so this appears like such a deal with.

I had a job in Hanoi from October 2021-January 2023, however stop to concentrate on college full-time. It appears like we have now an unbelievable quantity of freedom to make choices like that, which was by no means an possibility earlier than. Whereas I nonetheless have loads of nervousness concerning the future, I actually do really feel much less pressured about cash than I ever have.

What’s the worst a part of your present life-style/routine?

It’s arduous to be so distant from house. This yr we’ll go to the states for the primary time in two years. I missed my niece’s start in January in addition to 4 good buddies turning into first-time mother and father up to now yr. My mother and father are getting older and I’ve loads of guilt about not being shut by. Hanoi can be actually difficult — the air air pollution within the winter will get actually dangerous, visitors is insane, and the temperature is simply too scorching to go outdoors for months at a time.

I really feel like we’re typically accountable with cash, however we don’t have a plan mapped out for the long run. As a planner, this makes me nervous/really feel uncontrolled! I actually hate not having an earnings of my very own, however I’m so grateful to have the ability to focus solely on college proper now.

It’s arduous to make a plan when there are such a lot of unknown variables:

- The place are we going to dwell after the 2023-2024 college yr? Will we keep in Hanoi? Will we transfer to a brand new nation?

- What job will I get and the way a lot will I make?

- How a lot cash do we want for a home? Does it make sense to maintain saving money to purchase a home outright?

- How can expats contribute to retirement? How far behind are we?

The place Laura and Ethan Wish to be in Ten Years:

Funds:

- I’d prefer to have a paid off home within the states, ideally close to mountains/mountain climbing

- I’d prefer to have a mixed $500k in financial savings (between money and retirement)

- I wish to really feel financially comfy and never beholden to 9-5 jobs

Life-style:

- I’d prefer to have 2 children plus canines and cats operating round

- I’d like to have the ability to spend a lot of time with my household outdoor mountain climbing, tenting, gardening, mountain climbing

- I’d prefer to nonetheless be investing money and time in my hobbies and inventive pursuits

Profession:

- I wish to have labored in a worldwide well being position overseas for just a few years after which discover a hybrid position within the states that permits me to dwell the place I would like and go to the workplace sometimes — a dream is to maneuver to Staunton, VA and discover a job in DC that solely requires 1-2 visits to the workplace month-to-month. I do not know if that is real looking.

- Ethan want to nonetheless be educating at a college that provides him the identical autonomy in his classroom he has loved in Hanoi.

- He additionally has goals of proudly owning a motorcycle store at some point, however I believe that’s extra like 15 years away.

Laura and Ethan’s Funds

Revenue

| Merchandise | Variety of paychecks per yr | Gross Revenue Per Pay Interval | Deductions Per Pay Interval | Internet Revenue Per Pay Interval |

| Ethan’s wage from educating job | 12 | $5,514 | Taxes: 2133 (ouch!) Medical insurance: 391 | $2,990 |

| Laura’s contract work* | 2 | $4,137 | Untaxed | $4,137 |

| Annual gross whole: | $74,442 | Annual internet whole: | $44,154 |

*That is what I earned this yr for this job however I’m now not receiving this earnings. This was a contract that was paid incrementally, so this was not the determine I obtained month-to-month, simply FYI

Money owed: $0

Property

| Merchandise | Quantity | Notes | Curiosity/kind of securities held/Inventory ticker | Title of financial institution/brokerage | Expense Ratio (applies to funding accounts) | Account Kind |

| Ethan Excessive Curiosity Financial savings | $76,500 | We view this as home financial savings. | 3.90% | Marcus – Goldman Sachs | Money | |

| Laura 401k | $51,867 | 401k by earlier employer. | Vanguard Goal Retirement 2055 | Voya | Retirement | |

| Ethan PSERS | $20,692 | PA Lecturers pension | We couldn’t determine this one out | Retirement | ||

| Laura Brokerage | $18,783 | That is my taxable funding account, which I opened (prematurely) a number of years in the past. I think about this home financial savings. | It says I’ve 13 completely different securities: FDIC, MUB, SUB, VB, VBR, VEA, VNQ, VNQI, VO, VOE, VTI, VTV, VWO however I do not know what this implies!! | Ellevest | Investments | |

| Ethan 403b | $17,362 | Retirement by earlier | Vanguard Goal Retirement 2050 | PenServ | Retirement | |

| Ethan 403b | $14,764 | Retirement by earlier | We couldn’t determine this one out | Alerus | Retirement | |

| Laura Excessive Curiosity Financial savings | $10,165 | Again up cash for grad college tuition and home financial savings. | 3.90% | Marcus – Goldman Sachs | Money | |

| Ethan and Laura Vietnamese Checking | $9,477 | We plan to run this empty, as spending the VND earned right here is the most cost effective solution to spend cash right here | 0% | Commonplace Chartered | Money | |

| Ethan IRA | $5,544 | Vanguard | Retirement | |||

| Laura Checking | $5,228 | 0% | TD | Money | ||

| Ethan Checking | $3,000 | 0% | TD | Money | ||

| Laura Roth IRA | $2,326 | Identical as brokerage acct. | Ellevest | Retirement | ||

| Whole: | $235,708 |

Automobiles

Bills

| Merchandise | Quantity | Notes |

| Tuition | $700 | I bought a division scholarship and hoping to get extra! |

| Groceries | $250 | Consists of all meals, alcohol/beer, family and private provides (akin to bathroom paper, shampoo, and many others) |

| Journey (flights, accommodations, taxis, meals out) | $250 | We journey lots, it’s a part of the enjoyment and alternative of dwelling right here. Worldwide flights are low-cost and comfy lodging is often $25-40/night time. We’re reimbursed for the price of two spherical journey tickets to the States each summer time (whether or not we purchase the tickets or not). |

| Eating places, cafes, bars | $150 | We repeatedly exit to eat however prioritize consuming native meals (like pho and vegetarian buffet which value as little as 75 cents) relatively than costly Western eating places. We like to spend a weekend afternoon at a espresso store which is a big a part of Vietnamese tradition. |

| Transportation | $60 | Motorcycle rental, fuel for motorcycle, occasional taxi |

| Electrical | $50 | On common. We don’t ever run the warmth though it DOES get chilly within the north and we reduce AC utilization as a lot as attainable |

| Gymnasium | $50 | We paid for our fitness center memberships upfront. Laura paid $400 for two years and goes to courses practically day by day. Ethan paid $400 for a yr at a bouldering fitness center |

| Garments, sneakers | $45 | We purchase good trainers every year and don’t low-cost out on these. We don’t typically purchase new garments however issues pop up just a few instances a yr. |

| Consuming water | $30 | Faucet water is unsafe right here so we at present purchase 20 liter jugs just a few instances per week |

| Items | $30 | We aren’t massive reward givers – we view our frequent journeys as items for birthdays, anniversaries, and many others – however have had shut 5(!) family and friends have kids this previous yr and ship small items for rapid household birthdays |

| Netflix | $22 | I’d prefer to cancel this as a result of we don’t actually use it however I pay for my household’s account |

| Charitable donations | $20 | I take advantage of the Libby app with my Kindle. It feels good to make a donation to my library again in Philly each month. Would like to do extra. |

| Knitting provides | $15 | That is an estimate. I bought actually into knitting in the course of the pandemic and spent $187 on needles, yarn, patterns final yr. I’ve sufficient yarn and unfinished tasks to final me the entire yr after which some so it’s seemingly this will likely be a lot much less. |

| Spotify | $14 | |

| Cell telephones | $10 | $60/yr every will get us limitless information however no minutes or SMS which is okay as a result of we simply use WhatsApp and by no means make calls |

| Massages, haircuts | $10 | Massages are ~$12/hr and we go a pair instances a yr. Ethan will get a $15 haircut 2x/yr. I’ve been giving myself little trims at house since we’ve lived in VN. |

| Misc (books, and many others) | $10 | We use the Libby app with our Kindles however sometimes order by Thriftbooks for issues unavailable on the library. |

| Dentist | $8 | We every get enamel cleanings 2x/yr (very cheap however prime quality right here – $15 every out of pocket with none insurance coverage!). I had two fillings in January ($40) and hoping to not want any further work accomplished within the close to future |

| Shrole | $6 | Web site for worldwide college job postings |

| Air and bathe air purifier filters | $5 | Air air pollution will get actually dangerous right here throughout winter months so air purifiers are important. The water is closely chlorinated and getting a filter has been immensely useful for pores and skin and hair points! We alter each each 6 months or so. |

| The Atlantic | $3 | |

| VPN | $2 | $56/26 months. Lastly bit the bullet this yr as a result of we couldn’t entry some banking websites from overseas |

| The New York Occasions | $1 | Acquired a deal on a brand new subscription for this yr, will go up subsequent yr or we could cancel |

| Hire | $0 | Ethan’s college pays our hire on to the owner |

| Month-to-month subtotal: | $1,741 | |

| Annual whole: | $20,892 |

Credit score Card Technique

| Card Title | Rewards Kind? | Financial institution/card firm |

| Ethan – Blue Money On a regular basis | 3% money again | American Specific |

| Laura – Citi Double Money card | 2% money again | Citi |

| Joint – Enterprise One Rewards* | 1.25 miles per greenback spent | Capital One |

| Laura – Chase Freedom Limitless | 1.5% money again; 5% on journey | Chase |

*I bought this one after we moved right here as a result of it doesn’t cost overseas transaction charges. I don’t like having this many bank cards. We barely use them since we pay for many issues with money from our Vietnamese checking account.

Laura’s Questions for You:

-

Consuming our method round Seoul Are you able to assist us assume by saving for a home?

- We aren’t even positive when precisely we might do that, however it appears like the following massive factor to save lots of for.

- Given how a lot money we have now at present and that we wouldn’t purchase a home valued at greater than ~$300k, ought to we proceed saving? Is the thought of paying for a home in money horrible?!

- Are expats allowed to contribute to retirement?

- How far behind are we on retirement?

- Our earnings and bills are more likely to change after subsequent summer time once I now not need to pay for grad college and begin making an earnings once more.

- What ought to we do with this extra cash? Retirement? Money financial savings?

- Ought to we begin a separate financial savings earmarked for ‘shifting house’?

- How can I really feel much less anxious concerning the future?

- I’d like to get to a spot the place I’m comfy with what’s coming in and understanding that we’re automated to fulfill our objectives for the long run.

Liz Frugalwoods’ Suggestions

I’m thrilled to have Laura and Ethan as our Case Research topics right now! They convey an attention-grabbing twist with their work overseas and want to at some point transfer again to their house nation. I like that they’re taking the time now to map out their monetary strikes for the following few years. Even when issues don’t go completely to plan, it’s often finest to begin with a plan! Let’s dive into Laura’s questions:

Laura’s Query #1: Are you able to assist us assume by saving for a home?

Laura and Ethan have already got a hefty quantity–$76,500–saved up for a home, which is fabulous! My concern right here is their said want to pay money for a home. Laura requested:

Is the thought of paying for a home in money horrible?!

The reply is that it relies upon. In case you are ridiculously rich–as in, a billionaire or multi-multi-multi-millionaire–then it doesn’t actually matter. Pay money, don’t pay money–both method, you continue to have a ton of cash. However, in case you are within the class of most of us–as in, you’ve some cash, however it’s not limitless–it very hardly ever is sensible to pay money for a home. There are a variety of causes for this, so let’s discover all of them!

Why You Most likely Shouldn’t Pay Money For a Home (or repay your mortgage early)

1) It’s an enormous alternative value.

If you purchase a home in money (or repay a mortgage early), you’re lacking out on the potential funding returns you’d get pleasure from in case your cash was as an alternative invested within the inventory market or a rental property.

The take care of that is {that a} paid-off home returns the speed of your mortgage rate of interest (or the rate of interest you’ll’ve gotten on a mortgage).

For instance: in case your mortgage rate of interest is mounted at 3.75% and also you pay if off, you’re getting a 3.75% charge of return, which is fairly low. By comparability, historic inventory market tendencies show that–over many many years of investing–the market delivers someplace within the vary of seven% yearly. That doesn’t imply 7% yearly, however relatively, a 7% common over the lifetime of an investor. Since 7% is the next return than 3.75%, you’d be higher off–on this hypothetical–with carrying a mortgage and as an alternative investing your additional money within the inventory market.

→The place this logic doesn’t maintain up as effectively is when mortgage rates of interest are excessive.

Nonetheless, even within the case of upper mortgage rates of interest, it nonetheless often is sensible to hold a mortgage due to the chance value of that money sitting round incomes nothing for all of the years it took you to reserve it up. Most of us don’t get up at some point with $300k in our checking account. As a substitute, we’d need to spend a few years–doubtlessly many years–saving up that a lot money. Throughout that point, we’d be persistently exposing ourselves to the chance value of not having that money invested.

The explanation to not save sufficient money to purchase a home outright mirrors the the explanation why we don’t save solely money for retirement:

- Money doesn’t sustain with inflation (day-after-day, your money is price lower than the day earlier than)

- If you spend your money, it’s gone (versus drawing down a sustainable share of an general funding portfolio)

- Money doesn’t have the potential to understand (past the rate of interest you earn in your financial savings account)

2) Saving this a lot money may restrict your retirement contributions.

Because you’re solely permitted to place a sure greenback quantity into tax-advantaged retirement accounts yearly, for those who’re as an alternative placing that cash in direction of money financial savings, you’re taking pictures your self within the foot twice:

- You’re lacking out on the tax benefits conferred by retirement accounts

- You’re lacking out on the potential development of these retirement accounts (alternative value)

When you have the monetary capacity to take action, you wish to max out your whole tax-advantaged retirement accounts yearly. Once more, there’s an annual cap on how a lot you’ll be able to funnel into tax-advantaged retirement accounts, which is why it’s vital to take action yearly.

3) A paid-off home is an illiquid asset.

That is one other salient concern as a result of you’ll be able to’t use a paid-off home to purchase groceries or repair your automotive or pay for medical health insurance for those who lose your a job. Sure, you may be capable to get a House Fairness Line Of Credit score (HELOC), however that’s not a assure and definitely not very seemingly for those who’ve misplaced your job.

Tying up ALL of your extra money in a paid-off home is a harmful proposition. Positive, you would promote the home, however then you definately’ll must pay for elsewhere to dwell.

4) Earlier than shopping for a home in money (or paying off a mortgage early), it is advisable to have the entire following:

- A strong emergency fund of, at minimal, three to 6 months’ price of your dwelling bills, held in an simply accessible checking or financial savings account.

- No excessive rate of interest debt.

- Retirement investments (i.e. a 401k, 403b, IRA, Roth IRA, and many others) which can be totally funded as acceptable in your age, objectives and anticipated retirement date.

I’d additional argue that you simply also needs to have not less than one different type of funding (along with your retirement), akin to:

- A taxable funding account of diversified whole market, low-fee index funds, each home and worldwide (aka shares)

- 529 School Financial savings accounts in your children

- Elective: an income-generating rental property

You actually don’t want to have this whole second checklist of things lined up, however it is best to completely have the primary three on lockdown.

5) A mortgage is a pleasant hedge in opposition to inflation.

Inflation is when cash turns into much less precious. The advantage of a mortgage is that it’s denominated within the {dollars} you initially paid for the home. Thus over time as inflation will increase, which typically occurs, the cash you’re utilizing to repay your mortgage turns into “cheaper.” That is one other method through which a mortgage can actually work to your monetary benefit.

Abstract:

Until you’ve limitless funds (through which case you’re seemingly not studying this… ), paying money for a home (or paying off a mortgage early) is often an emotional choice, not a monetary one.

Laura’s Query #2: Are expats allowed to contribute to retirement?

This reply relies upon totally upon Laura and Ethan’s tax state of affairs. In keeping with H&R Block:

To be able to contribute to an IRA whereas dwelling overseas, it is advisable to have earnings leftover after deductions and exclusions. In case you exclude your whole earnings with the FEIE and don’t have any different sources of earned earnings, you aren’t eligible to contribute to an IRA. Nonetheless, for those who solely exclude a part of your earnings or declare the overseas tax credit score (FTC) as an alternative, you should still be capable to contribute to an IRA.

To place this extra merely, Laura and Ethan must have sufficient earned earnings leftover after claiming the overseas earned earnings exclusion (and some other exemptions, such because the overseas housing exclusion). Since we don’t have Laura & Ethan’s tax returns, we will’t exactly reply this query, however I hope this helps level them in the suitable course. In the event that they’re utilizing an accountant to arrange their taxes, it is a nice query to ask them.

→The opposite factor to notice is that Laura must have earned earnings to be able to be eligible to contribute to an IRA. Since she doesn’t have earned earnings proper now, she will be able to look into opening a spousal IRA.

Right here’s the IRS documentation on this (management F for “Contributions to Particular person Retirement Preparations”).

Laura’s Query #3: How far behind are we on retirement?

Let’s check out what they at present have of their retirement investments:

| Merchandise | Quantity | Notes |

| Laura 401k | $51,867 | Retirement account by earlier employer. |

| Ethan PSERS | $20,692 | PA Lecturers pension |

| Ethan 403b | $17,362 | Retirement account by earlier employer. |

| Ethan 403b | $14,764 | Retirement account by earlier employer. |

| Ethan IRA | $5,544 | |

| Laura Roth IRA | $2,326 | |

| Whole: | $112,555 |

Whereas this whole technically places them behind on retirement given their ages, it additionally doesn’t precisely account for the three mega wildcards right here:

- Ethan’s pension

- Their anticipated Social Safety

- Their future jobs and potential future employer-sponsored retirement plans

As we’ve mentioned in earlier Case Research, pensions are a wild card. In some instances, a pension means you’re set for all times when you retire. In different instances… not a lot. Laura famous that they weren’t in a position to determine Ethan’s pension, however they should. There’s somebody whose job it’s to elucidate the PA pension system to academics and they should name that particular person. I can’t reply this for them since I don’t know the dates of Ethan’s service or his job title, however, it is a worthy rabbit gap for them to go down. I’d begin with the PSERS web site and/or the trainer’s union rep.

→One other a significant factor is whether or not or not Ethan plans to return into public college educating as soon as they’re stateside.

If that’s the case, he’ll seemingly be eligible for one more pension system and he’ll wish to guarantee he understands the ramifications of totally qualifying for that pension. Observe that in some instances, receiving a public worker pension disqualifies you from receiving Social Safety. Moreover, if Ethan teaches in a public college below the identical PSERS pension plan, he’ll wish to spend some high quality time with HR and/or his union rep to make sure he’s capable of apply his earlier years of service.

From their above checklist of retirement accounts, it appears to be like like Laura and Ethan did a terrific job of contributing to retirement by their earlier employers. In mild of that, they need to proceed that behavior as soon as they’re stateside. They will additionally resume their IRA/Roth IRA contributions at the moment.

Laura’s Query #4: Our earnings and bills are more likely to change after subsequent summer time once I now not need to pay for grad college and begin making an earnings once more. What ought to we do with this extra cash? Retirement? Money financial savings? Ought to we begin a separate financial savings earmarked for ‘shifting house’?

I like that Laura’s planning to date forward! Nonetheless, I believe this reply will depend upon the place they’re of their means of shifting again to the states.

Retirement:

In the event that they decide that their tax state of affairs makes them eligible to contribute to their Roth IRA and IRA, they need to completely go forward and max these out. Observe once more that Laura would wish to both have earned earnings or open a spousal IRA.

Moreover, if their future US jobs supply employer-sponsored retirement accounts, they will max these out.

Money Financial savings:

Laura and Ethan are already overbalanced on money, as we will see under:

| Merchandise | Quantity | Notes |

| Ethan Excessive Curiosity Financial savings | $76,500 | We view this as home financial savings. |

| Laura Excessive Curiosity Financial savings | $10,165 | Again up cash for grad college tuition and home financial savings. |

| Ethan and Laura Vietnamese Checking | $9,477 | We plan to run this empty, as spending the VND earned right here is the most cost effective solution to spend cash right here |

| Laura Checking | $5,228 | |

| Ethan Checking | $3,000 | |

| TOTAL: | $104,370 |

In mild of that, I’m hesitant to suggest they stash much more cash in money, for all the explanations I outlined above associated to alternative prices.

I do, nonetheless, totally help their present money stash because it represents:

- A home downpayment

- Buffer for grad college tuition funds

- Their emergency fund

- Vietnamese forex they intend to spend down

- Shifting-back-home cash

→Now I’m going to disagree with myself: regardless of the chance prices of money, it’s additionally true that Laura and Ethan are in flux proper now.

They’re not sure the place they’ll be dwelling in just a few years, how a lot a home will value, after they’ll have children, how rapidly they’ll discover new jobs, what their shifting prices will likely be and what their bills will likely be again in America. That’s loads of unknown variables! And one of the best factor to have when there are a bunch of unknowns is additional money. I do wish to warning them, although, that money just isn’t a longterm funding technique. Neither is it the place to maintain massive chunks of cash for lengthy durations of time.

If it had been me, I’d maintain all of this present money available and wait and see how plans shake out. An alternative choice for them to contemplate are medium-term funding choices, akin to CDs, Cash Market Accounts, and many others. Nonetheless, they’re already in a high-yield financial savings account, which is essentially the most versatile solution to leverage your money.

If Laura and Ethan know they gained’t be utilizing their home downpayment for the following yr or so, they may actually see if there’s a 12-month CD providing the next charge of return than their high-yield financial savings account. That might be one solution to primarily maintain their money, but additionally have it earn extra. A CD locks your cash up for a specified time frame after which delivers you a specified return while you money it out. It’s not a terrific long-term funding automobile–for the reason that returns usually lag behind the inventory market–however it may be nice for short-term objectives.

Laura’s Query #5: How can I really feel much less anxious concerning the future? I’d like to get to a spot the place I’m comfy with what’s coming in and understanding that we’re automated to fulfill our objectives for the long run.

I personally don’t see something of their monetary state of affairs to be significantly anxious about. Their bills are low they usually clearly have good monetary habits ingrained. I get the sense that Laura’s nervousness is likely to be extra concerning the many unknown variables of their life proper now. I additionally don’t know that she’ll be capable to “automate” issues till they’ve moved again to the states and ironed out the place they’ll dwell and work. It’s actually too many variables to regulate for at this level, however I wish to emphasize once more that they’re doing a terrific job! The important thing will likely be for them to retain their glorious cash habits as soon as they return to the US and expertise a dramatically greater value of dwelling.

In lots of method, they’re in a holding sample whereas dwelling in Vietnam. However that’s not essentially a foul factor! Saving up more cash is at all times a sensible choice. When and easy methods to deploy that cash will turn into clear as these different life-style components fall into place. I understand that that is straightforward for me to say since I’m not dwelling it, however, from an outsider’s perspective, Laura and Ethan are doing nice!

Analysis Your Funding Accounts

One closing piece of recommendation for Laura and Ethan is to look into their funding accounts. Whereas it’s improbable that they’ve retirement investments in addition to a taxable funding account, they didn’t present a lot element on what these accounts are invested in. That is the “satan within the particulars” of investing. The primary vital step is to open these accounts and put cash into them. The subsequent most vital step is to be sure to’re investing in a method that matches your priorities and limits the charges you pay.

Rollover the Previous 401ks and 403bs

Since they’ve a variety of accounts from earlier employers, I encourage them to look into rolling over these accounts–the outdated 401ks and 403bs–into IRAs. The explanation to do that is as a way to management what you’re invested in. When you’ve a retirement account by a present employer, you’ll be able to solely select investments which can be provided by your organization’s plan. In some instances, that’s completely advantageous and you’ve got nice choices to select from. In different instances, you’re locked into funds with excessive charges and/or poor efficiency. Regardless of that, it nonetheless is sensible to max out employer-sponsored accounts. However, as soon as you permit that employer, you’re free to roll that account over into an IRA that falls totally below your jurisdiction.

Roll right into a Roth IRA or a Common IRA? In case your 401ks/403bs had been arrange as Roths, you’ll be able to roll them right into a Roth IRA. In the event that they’re not arrange as Roths, you’ll be able to roll them into a conventional IRA. You usually don’t ever wish to roll from an everyday to a Roth as you’d then need to pay allllll the taxes in that calendar yr. Not good!

Right here’s easy methods to execute a rollover:

- Name the brokerage (or do it on-line) that at present holds your 401ks/403bs to ask about doing a “direct rollover” into a conventional IRA (both at that brokerage or a distinct one).

- You’re seemingly not going to wish to roll them into Roth IRAs since you’d then need to pay taxes on the complete quantity all on this calendar yr (assuming these accounts aren’t Roth). If they’re Roths, they will solely be rolled right into a Roth.

- Your new brokerage will wish to know what you wish to make investments your rolled over IRAs in.

Right here’s an article explaining rollovers: Your Information to 401(ok) and IRA Rollovers.

What to Make investments In?

Now that we all know the automobile Laura and Ethan will likely be using–both a Roth or conventional IRA–what ought to they make investments them in? I can’t inform them particularly what to spend money on, however I can inform them the broad strokes that I comply with with my investments.

If it had been me, I’d put all the things into one whole market, low-fee index fund that matched my asset allocation wants and danger tolerance. The explanation for that is that, generally, investing in a complete market index fund provides you the broadest attainable publicity to the inventory market (in addition to the bottom charges).

In a complete market index fund, you’re primarily invested in a teensy bit of each single firm within the inventory market, which supplies you a ton of variety. If one firm–and even one sector–tanks, your complete portfolio isn’t toast. It’s the “not placing your whole eggs in a single basket” model of investing.

Know Your Threat Tolerance

One other key consider investing is knowing your private danger tolerance. Investing within the inventory market is inherently dangerous. In mild of that, Laura and Ethan have to find out how dangerous they wish to be with their investments. A great way to mitigate danger is thru diversification, which is why many people have each shares and bonds of their funding portfolio.

The best method to consider that is that usually, excessive reward = excessive danger and low reward = low danger.

The best method to consider that is that usually, excessive reward = excessive danger and low reward = low danger.

Discover Your Expense Ratios

One thing lacking from Laura and Ethan’s checklist of property are the expense ratios on their funding accounts. This can be a important bit of knowledge they need to look into for the retirement accounts and their taxable funding account. Expense ratios are the share you pay to the brokerage for investing your cash and, as they’re charges, you need them to be as little as attainable.

As Forbes explains:

An expense ratio is an annual charge charged to traders who personal mutual funds and exchange-traded funds (ETFs). Excessive expense ratios can drastically cut back your potential returns over the long run, making it crucial for long-term traders to pick out mutual funds and ETFs with affordable expense ratios.

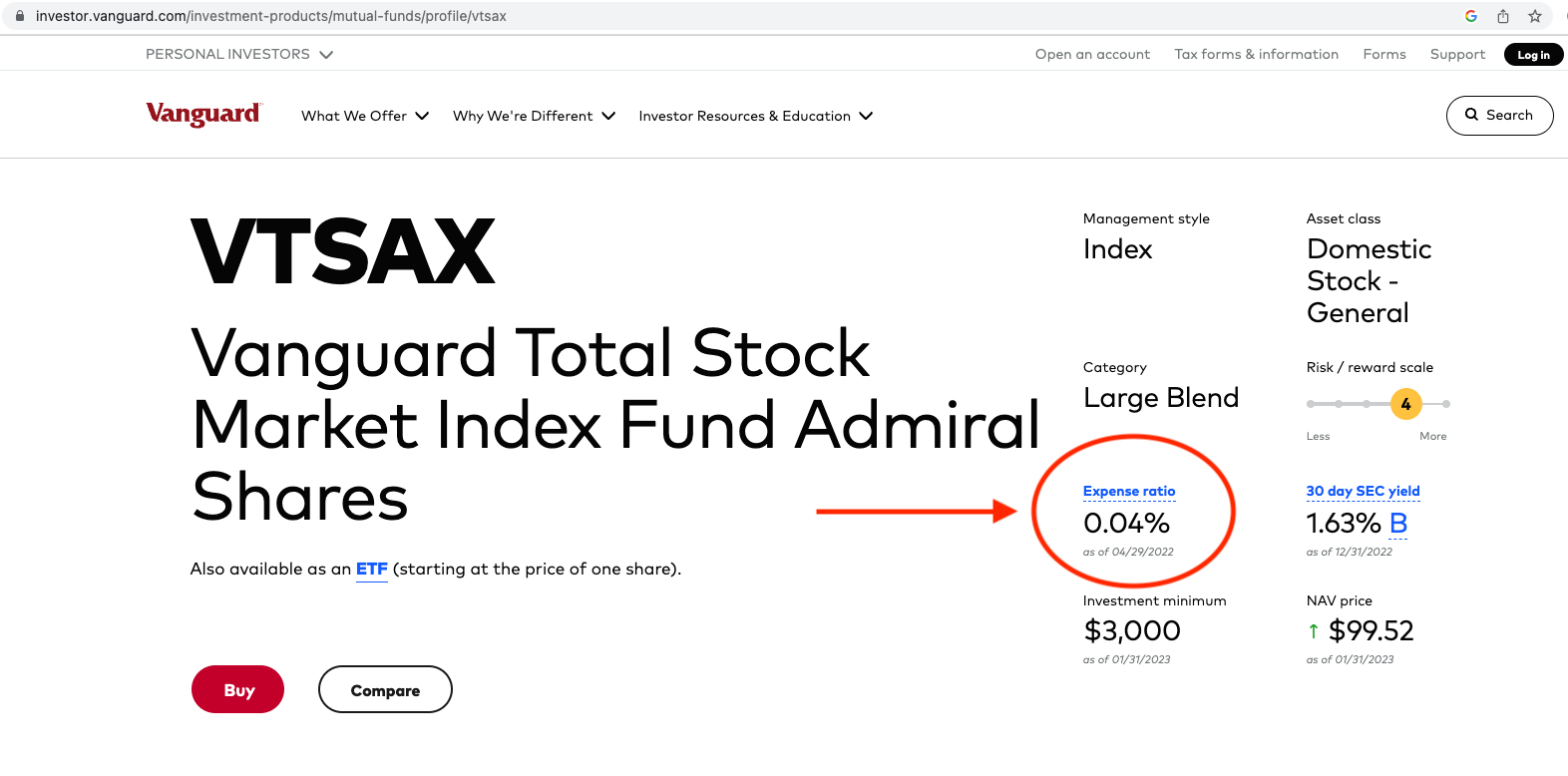

I’ll use Vanguard’s Whole Market Index Fund (VTSAX) in an illustration of easy methods to discover a fund’s expense ratio:

- Google the inventory ticker (on this case I typed in “VTSAX”)

- Go to the fund overview web page

- Have a look at the expense ratio

Screenshot under for reference:

To present Laura and Ethan a way of whether or not or not their investments have affordable expense ratios, the next three funds are thought of to have low expense ratios:

- Constancy’s Whole Market Index Fund (FSKAX) has an expense ratio of 0.015%

- Charles Schwab’s Whole Market Index Fund (SWTSX) has an expense ratio of 0.03%

- Vanguard’s Whole Market Index Fund (VTSAX) has an expense ratio of 0.04%

They will additionally use this calculator from Financial institution Charge to find out what they’ll pay in charges over the lifetime of their investments, based mostly on their expense ratios. In case you discover that your investments have excessive expense ratios, it’s effectively price your time to analyze shifting them to lower-fee funds (or altering brokerages altogether).

Investing 101

I extremely suggest the e book, The Easy Path to Wealth: Your Street Map to Monetary Independence And a Wealthy, Free Life, by: JL Collins, for those who’d prefer to deepen your data round investing. It’s well-written and straightforward to comply with.

Abstract:

- Familiarize yourselves with the drawbacks of paying money for a home:

- Know that not all debt is dangerous. In some instances, leveraging debt is essentially the most financially prudent transfer.

- Study your tax state of affairs to find out whether or not or not you’ve sufficient earned earnings to contribute to your IRA:

- Since Laura doesn’t have earned earnings proper now, she will be able to look into opening a spousal IRA

- Analysis Ethan’s pension:

- This might be a pivotal a part of your retirement and it behooves you to know the parameters.

- Contemplate rolling over your outdated 401ks/403bs into IRAs:

- Analysis funds, learn JL Collins’ e book on investing and find a brokerage that’ll give you low-fee funds that match your required asset allocation and danger tolerance

- Plan to max out your future US employer-sponsored retirement plans:

- If Ethan returns to public college educating, make sure you perceive the pension system

- Really feel assured that you simply’ve made nice monetary choices up thus far and that carrying these good habits ahead will serve you effectively.

Okay Frugalwoods nation, what recommendation do you’ve for Laura? We’ll each reply to feedback, so please be at liberty to ask questions!

Would you want your personal Case Research to look right here on Frugalwoods? Apply to be an on-the-blog Case Research topic right here. Rent me for a non-public monetary session right here. Schedule an hourlong or 30-minute name with me, refer a buddy to me right here, schedule a free 15-minute name to be taught extra or e mail me with questions ([email protected]).

[ad_2]