{kind=link}

[ad_1]

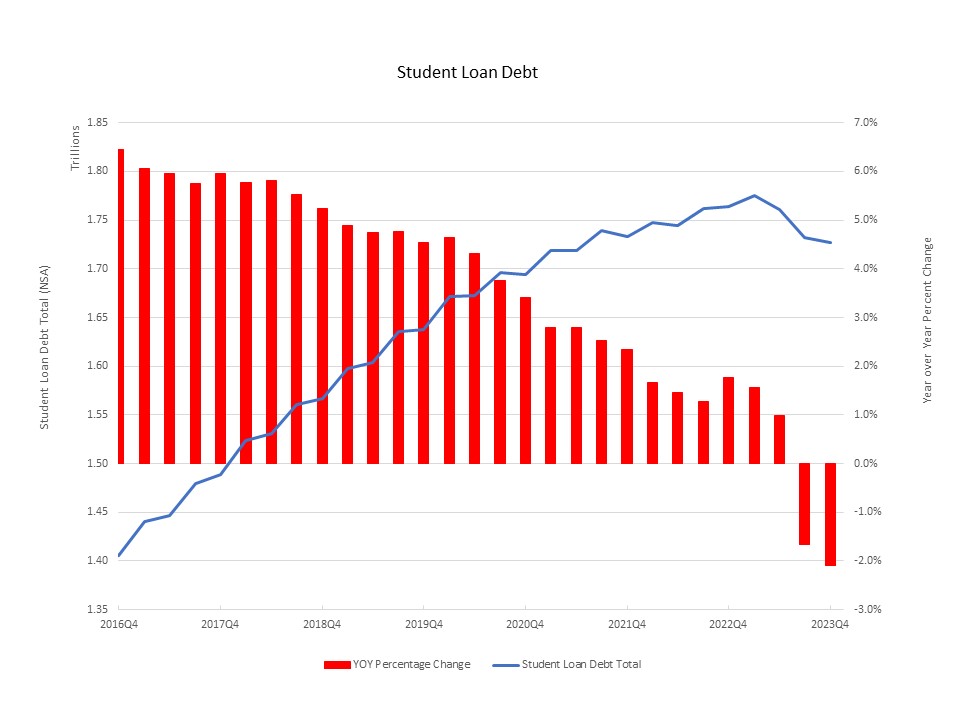

In line with the Federal Reserve’s G.19 Shopper Credit score Report, pupil loans within the fourth quarter of 2023 totaled $1.73 trillion (non-seasonally adjusted), reflecting a lower of 2.1% over the 12 months and following an annual lower of 1.7% within the earlier quarter. The third quarter of 2023 marked the primary year-over-year lower for pupil mortgage debt the info assortment started. This consecutive decrement is presentn within the graph below illustrated by each the degrees and 12 months–over–12 months charges.

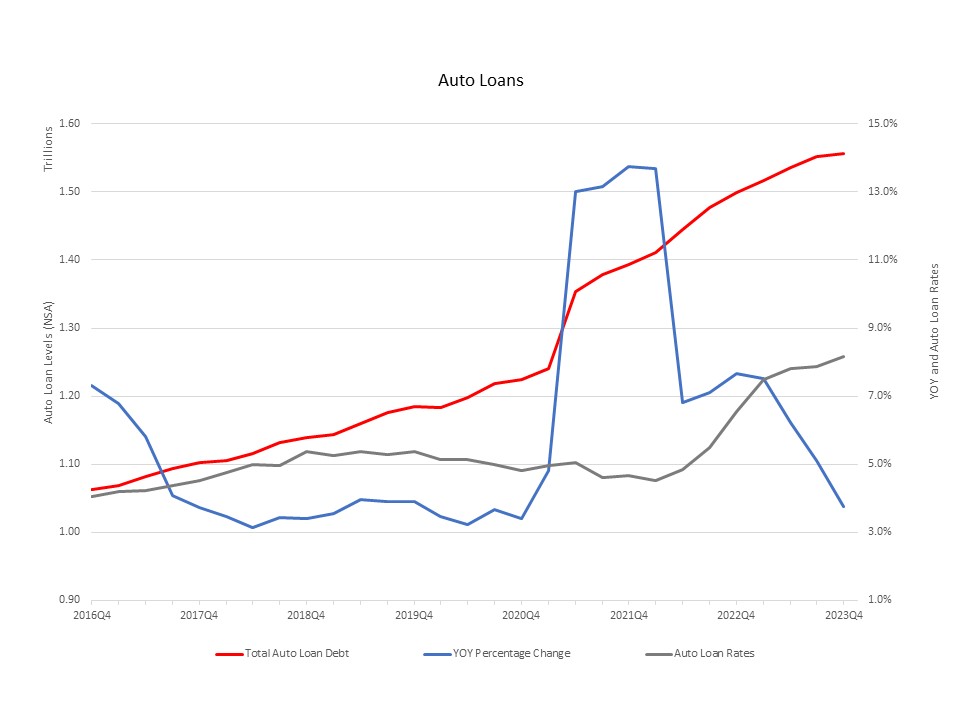

Contrastingly, auto loans proceed to extend, and have surged to a degree of $1.56 trillion (NSA). Nonetheless, equally to pupil loans, we’re seeing a steady deceleration in development charges (see graph under). The fourth quarter of 2021 noticed a excessive of a 13.7% YOY development in contrast to the fourth quarter of 2023 charge of 3.8%. This deceleration partially displays increased financing prices with auto mortgage charges rising from 4.5% in of 2021 to 8.2% in the fourth quarter of 2023.

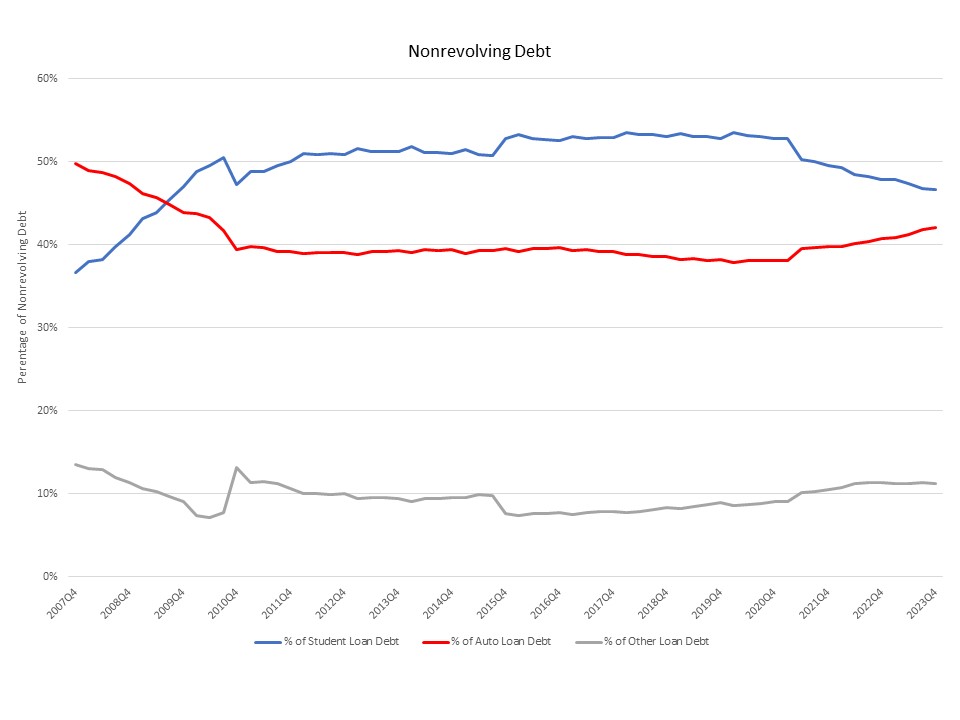

mponents of nonrevolving debt (the G.19 report excludes actual property loans), accounting for 46.7% and 42.0%, respectively. The collective different loans make up the remaining 11.3% of nonrevolving debt. Since information grew to become obtainable in 2006, auto loans accounted for the best share till 2009, when pupil loans took the lead, as depicted within the graph under. With the present pattern of pupil loans reducing and auto loans rising, it is doubtless that auto loans will once more have the upper share.

The overall for nonrevolving debt stands at 3.7 trillion (SA) for the fourth quarter of 2023, an annualized charge (SAAR) of 1.6% enhance from final quarter. Revolving debt, which is primarily made up by bank card debt, stands at $1.3 trillion, an 8.3% enhance from the third quarter (SAAR).

Of the whole excellent US debt within the fourth quarter of 2023, nonrevolving is 73.7%, revolving is 26.3%. The overall debt stands at $5.0 trillion for the quarter, a 3.3% enhance from the third quarter (SAAR). That is barely increased than the will increase for the second and third quarters however is decrease than the expansion charges for all of 2022 and 2021.

[ad_2]