{kind=link}

[ad_1]

What you might want to know concerning the SIBOR to SORA transition, and what you might want to do if in case you have an current house mortgage pegged to SIBOR charges.

PSA: You probably have a SIBOR-based mortgage or property mortgage, you might want to know that SIBOR (Singapore Interbank Supplied Price) will likely be discontinued quickly. Instead, SORA (Singapore In a single day Price Common) will now be used as the principle benchmark for SGD-denominated loans.

So in the event you’re an affected borrower, you’ll be able to both proactively change now to a house mortgage of your selection i.e. convert your current SIBOR-based house loans both to a SCP (SORA Conversion Package deal), or to one of many prevailing house mortgage packages provided by your financial institution.

In any other case, in the event you select to do nothing throughout this era of energetic transition (till 30 April 2024), you’ll finally be robotically transformed by your financial institution in June 2024 at a set adjustment unfold of 0.2426% and 0.3571% respectively for loans referencing 1-month and 3-month SIBOR to 3-month Compounded SORA.

SIBOR will likely be formally discontinued after 31 December 2024.

Since curiosity funds can not be calculated for SIBOR-based loans after that and if no motion is taken by 30 April 2024, all excellent SIBOR house loans will subsequently be robotically transformed to the SORA Conversion Package deal in June 2024.

If you need a selection as to which house mortgage bundle you like to change to, then you definitely’re inspired to contact your financial institution throughout this energetic transition interval.

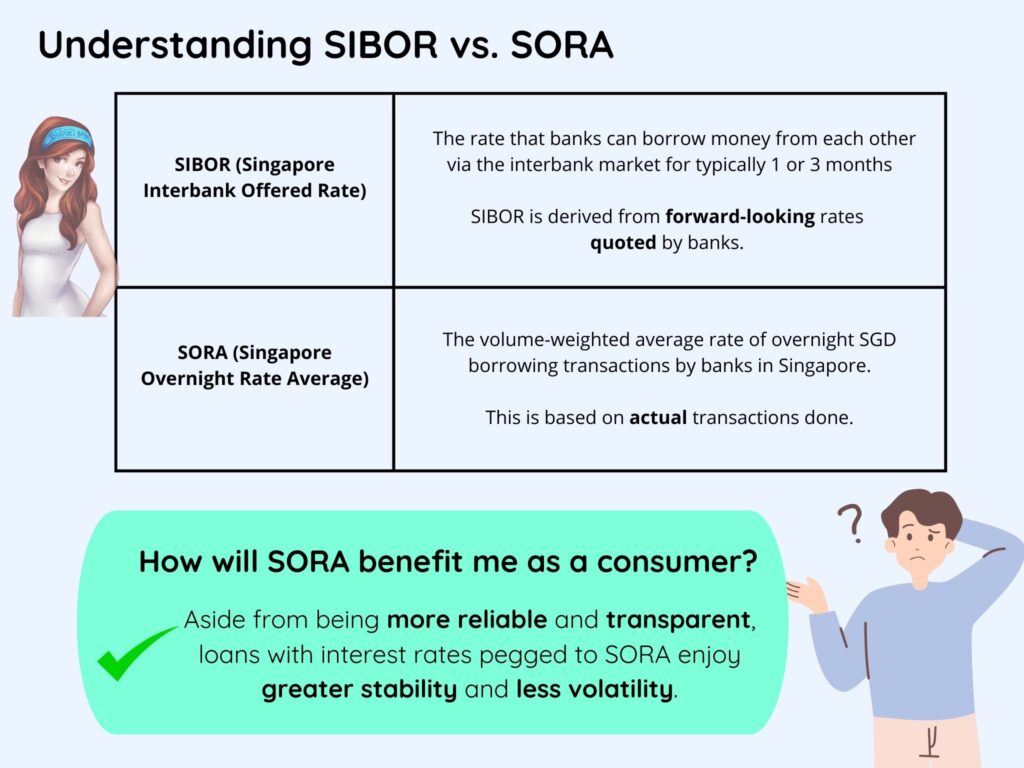

How will SORA profit me as a client?

Apart from being extra dependable and clear, loans with rates of interest pegged to compounded SORA will get pleasure from higher stability and much less volatility.

SIBOR contracts sometimes use a single day’s studying of the benchmark for every curiosity cost interval. The draw back is that debtors are uncovered to market circumstances concentrated in a single single day. For example, some debtors could expertise increased curiosity cost for a whole three-month interval if the SIBOR spiked on specific day on account of a worldwide threat occasion.

In distinction, curiosity funds on SORA mortgage packages are primarily based on compounded SORA, which is computed as an common of particular person SORA readings over the inter-payment interval – e.g. month-to-month or quarterly, relying on how continuously your mortgage curiosity funds are calculated. Thus, using compounded SORA leads to a charge that’s much less uncovered to sudden modifications to rates of interest. As a result of averaging impact, rates of interest spiking increased on one or a couple of days is not going to influence your curiosity funds by as a lot because of the averaging impact. It additionally implies that any change in market circumstances will solely be step by step mirrored over time.

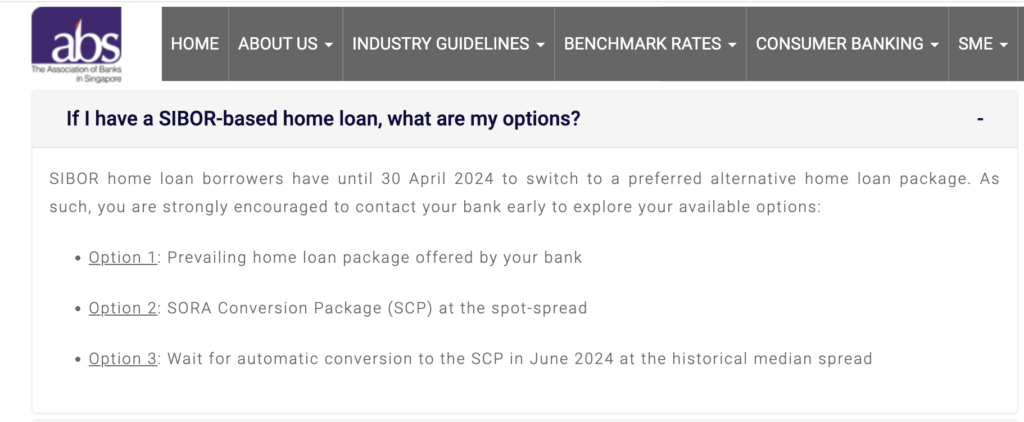

What are my choices if I’ve an current SIBOR mortgage?

Okay, so how does this modification have an effect on house debtors?

In case your present housing mortgage is tied to the 1M or 3M SIBOR, you’ll be able to select between two choices now:

1. Change to the SORA conversion bundle (SCP), or

2. Go for some other mortgage bundle provided by your financial institution.

Alternatively, in the event you take no motion by 30 April 2024, your financial institution will auto-convert your SIBOR-based mortgage to the SCP in June 2024.

The excellent news is, changing your current SIBOR mortgage to the SCP or any of your financial institution’s prevailing mortgage packages with the identical financial institution now will NOT incur any further charges or lock-in interval. Sure, these are a part of a wider business initiative to help prospects who change out of their SIBOR retail loans throughout this energetic transition interval.

You’ll even be exempted from recomputing your Mortgage Servicing Ratio (MSR), Mortgage-To-Worth (LTV), and Complete Debt Servicing Ratio (TDSR), so long as the choice mortgage bundle you’ve opted for is along with your current financial institution.

Word: For those who’re aspiring to refinance your property mortgage and change to a different financial institution, you’d wish to test if some other TDSR exemptions apply e.g. debtors who’re owner-occupiers are exempted from TDSR when refinancing your property loans.

Will this depend as a refinancing of my property mortgage?

No. MAS has beforehand confirmed that the taking over of the SCP and prevailing packages provided by the banks to prospects with current SIBOR property loans is not going to be considered a refinancing of property loans below the regulator’s property mortgage guidelines.

Ought to I change now or later?

There’s nonetheless time, so that you don’t need to rush into a call simply but. Nonetheless, this text is supposed to offer you a heads-up that if you’re an current SIBOR house mortgage borrower, you’re inspired to talk to your financial institution early to discover the out there choices.

That approach, you’ll have extra time throughout this era to resolve on what would be the greatest transfer for you.

Do you have to select to do nothing for now till 30 April 2024, your SIBOR mortgage will likely be robotically transformed by the banks ranging from 1 June 2024. And no, you won’t be able to maintain your SIBOR mortgage, as a result of curiosity funds primarily based on SIBOR can’t be computed anymore after SIBOR is discontinued.

| Dates | What’s occurring? | Remarks |

| 1 September 2023 – 30 April 2024 | Interval of energetic transition for debtors to change to a SORA conversion mortgage or a financial institution’s prevailing mortgage bundle | The SCP will likely be structured as: 3-month Compounded SORA + buyer’s current SIBOR margin + Adjustment Unfold (Retail). The Adjustment Unfold (spot-spread) will likely be decided as the typical distinction between the relevant SIBOR and 3-month Compounded SORA over the previous three-month interval. |

| June 2024 | Interval of computerized conversion throughout the business for all excellent SIBOR retail loans to SORA. | Your financial institution will apply the SCP with the Adjustment Unfold (historic median) set at 0.2426% and 0.3571% respectively to transform loans referencing 1-month and 3-month SIBOR to 3-month Compounded SORA. These signify the 5-year historic median spreads between the relevant SIBOR and 3-month Compounded SORA over the interval 30 June 2018 to 30 June 2023. |

As you’ll be able to see, it’s undoubtedly extra advantageous to begin enthusiastic about whether or not you wish to change to an alternate house mortgage if you can, and not if you have to.

Taking motion now to contact your financial institution to decide on a mortgage that’s appropriate for you earlier than SIBOR loans are totally phased out might be helpful, since you’ll be minimising disruptions to your mortgage when SIBOR is discontinued.

You can even keep away from scrambling to take up any mortgage bundle your financial institution gives you when the deadline comes, which can or will not be the most effective supply then.

What if I wish to change my house mortgage to a different financial institution?

If you’re going with the SCP, which is a regular bundle that every one banks are providing, then there may be little purpose to change banks.

You’ll have to stick along with your present financial institution in an effort to get pleasure from the advantages (charge waiver, exemption of MSR, LTV and TDSR).

Nonetheless, in the event you intend to change to a different mortgage bundle provided by a totally different financial institution as a substitute (e.g. to benefit from a limited-time promotional charge), then do word that it will likely be the identical as the standard course of concerned in refinancing your mortgage(s) i.e. you’ll have to pay all the standard administrative / authorized charges, and be topic to MSR and TDSR critiques (until you may have exemptions from these for different causes, e.g. debtors who’re owner-occupiers are exempted from TDSR when refinancing your property loans).

What are the prevailing packages out there available in the market?

The prevailing packages provided by your financial institution may embody

- floating charge packages, sometimes primarily based on compounded SORA or financial institution board charges, and/or

- mounted charge loans.

Please method your financial institution to seek out out what are the prevailing packages they provide.

For those who’re contemplating SORA-based loans, its key profit lies in its transparency, for the reason that SORA charge is printed on MAS web site on every enterprise day at 9am. Because the unfold that every financial institution fees over compounded SORA is evident to see, it turns into simpler for us as debtors to check house loans in opposition to one other financial institution!

One other different is to go for a floating mortgage pegged to the financial institution’s board charge, which is mounted internally by the financial institution. Nonetheless, these board charges have hardly any transparency as they’re decided solely on the financial institution’s discretion, making it a lot tougher to check mortgage packages.

Ought to I select a set or floating charge house mortgage?

Within the final decade, floating-rate house loans have usually been cheaper than mounted charge loans because of the low rate of interest atmosphere then. The draw back is that these loans are topic to rate of interest fluctuations, which may trigger financing points for debtors who don’t have spare money to cope with the modifications when rates of interest rise. With the unsure rate of interest outlook as we speak, it’s anybody’s guess whether or not a majority of these loans will stay reasonably priced within the quick to medium time period.

If you’re risk-averse, a fixed-rate house mortgage could also be extra acceptable to your threat urge for food as there will likely be no have to panic even when rates of interest rise immediately, because you’ll nonetheless be paying the identical quantity no matter any fluctuations in rates of interest. At occasions, you’ll even get to save lots of extra on the month-to-month instalments throughout spikes in rates of interest.

The trade-off? Mounted-rate mortgage charges are sometimes increased than floating charges, though some individuals don’t thoughts paying increased mortgage rates of interest in change for stability and a peace of thoughts.

Tip: Plan primarily based in your threat urge for food and financing capacity, reasonably than purely primarily based on prevailing rate of interest gives. For those who don't have the spare money or emotional bandwidth to cope with sharp fluctuations in rates of interest, then a fixed-rate mortgage could also be higher for you. Communicate to your financial institution early, who will have the ability to present additional recommendation in your choices.

What’s the greatest mortgage mortgage rate of interest?

Given {that a} mortgage is more likely to be one’s best monetary legal responsibility, we want to verify we proactively handle our house loans, particularly on this interval of financial uncertainties and international rate of interest modifications. Whether or not you’re planning to refinance otherwise you’ve set your eyes on a brand new house, you might face a dilemma when deciding which is the “greatest” mortgage mortgage bundle.

For those who’re uncertain, you’re inspired to contact your financial institution to hunt recommendation from their mortgage specialist, as proactively managing your mortgage is a vital step in constructing a sound monetary plan.

You may even put any curiosity financial savings to good use, reminiscent of leveraging increased interest-yielding financial savings instruments to inflation-proof your emergency funds.

Conclusion

The energetic transition interval for debtors to transform their current SIBOR-based loans to an alternate mortgage bundle is occurring now until 30 April 2024, and you’re going to get to get pleasure from the next advantages when changing your mortgage along with your financial institution:

- A one-time charge waiver

- with no further lock-in interval

- you’ll be exempted from recomputing your Mortgage Servicing Ratio (MSR), Mortgage-To-Worth (LTV) and Complete Debt Servicing Ratio (TDSR)

Extra importantly, you may have the flexibility to decide on a house mortgage bundle that you just desire now, reasonably than scrambling round when the deadline arrives. It’s thus price exploring your choices as we speak to see what is going to go well with you greatest.

For subsequent steps, you’ll be able to both method your financial institution or a mortgage specialist to seek out out what choices can be found to you.

Disclosure: This text is written in collaboration with The Affiliation of Banks in Singapore (ABS), as a part of their academic outreach efforts to lift public consciousness about with the ability to change to SORA or different house mortgage packages throughout this energetic transition interval earlier than SIBOR is formally phased out. The contents and slant mirror each the creator's views and ABS' inputs for factual accuracy.

[ad_2]