{kind=link}

[ad_1]

The primary sequence of Sovereign Gold Bond Scheme 2024 Collection 4 will likely be out there for funding from twelfth February to sixteenth February 2024. Do you have to purchase it?

With the latest great returns of the primary Sovereign Gold Bond, many are drawn to this product. RBI issued the primary Sovereign Gold Bond in November 2015. Therefore, 8 years accomplished in November 2023. The difficulty value was Rs.2,684 per gram (per bond). The redemption value set by RBI for this bond was Rs.6,132. Therefore, the return on funding is 10.88% (excluding 2.5% yearly curiosity). If we add the curiosity, then it’s round 12.5% !!

Additionally, the SGB 2018-19, Collection VI which was issued at Rs.3,326 is now eligible for untimely redemption on twelfth February 2024 on the value of Rs.6,263. Then the tax-free return (excluding the curiosity) is 13.49%!!

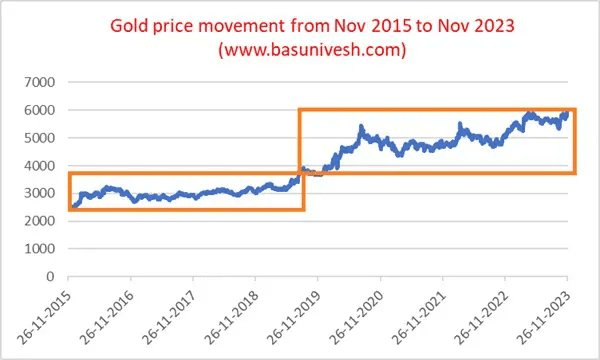

Whether or not the journey easy within the final 8 years for the gold?

Discover the flat and bumpy trip of the final 8 years of gold. From 2015 to 2019 it was one pattern and from 2019 onwards uptrend however throughout the rangebound for the subsequent 4 years. I wrote a publish by wanting on the previous 44 years of gold knowledge and the way a lot the unstable gold value motion is. Additionally, I’ve proven even when you maintain the gold for 8 years (equal to the time horizon of Sovereign Gold Bond), then what could also be written potentialities? You’ll be able to consult with the identical at “Sovereign Gold Bond Returns – How A lot Can You Anticipate?“. Nevertheless, we have now a agency perception that gold will all the time shine!!

This Gold Bonds scheme was launched in November 2015. The federal government launched this scheme to cut back the demand for bodily gold. Indians purchase round 300 tons of gold yearly. That is to be imported from outdoors international locations. Allow us to see the silent options of this scheme.

The Bonds shall be issued within the type of Authorities of India Inventory in accordance with part 3 of the Authorities Securities Act, 2006. The traders will likely be issued a Holding Certificates (Type C). The Bonds shall be eligible for conversion into de-mat kind.

Sovereign Gold Bond Scheme 2024 Collection 4 -Ought to You Purchase?

Earlier than you run to purchase Sovereign Gold Bond Scheme 2024 Collection 4, learn my earlier posts on this regard.

After studying the above posts, when you nonetheless really feel gold is price so that you can make investments, then go forward. Allow us to now talk about the options of this Sovereign Gold Bond Scheme 2024 Collection 4.

# Dates to subscribe

Sovereign Gold Bond Scheme 2024 Collection 4 will likely be open for subscription from twelfth February to sixteenth February 2024.

# Who can make investments?

Resident Indian entities together with people (in his capability as such particular person, or on behalf of a minor youngster, or collectively with some other particular person.), HUFs, Trusts, Universities, and Charitable Establishments can spend money on such bonds.

Therefore, NRIs usually are not allowed to take part within the Sovereign Gold Bond Scheme 2024 Collection 4.

# Tenure of the Bond

The tenor of the Bond will likely be for 8 years with an exit choice from the fifth yr to be exercised on the curiosity fee dates.

Therefore, after the 5 years onward you’ll be able to redeem it on the sixth, seventh, or at maturity of the eighth yr. Earlier than that, you’ll be able to’t redeem.

RBI/depository shall inform the investor of the date of maturity of the Bond one month earlier than its maturity.

# Minimal and Most funding

It’s a must to buy a minimal of 1 gram of gold. The utmost quantity subscribed by an entity is not going to be greater than 4 kgs per particular person per fiscal yr (April) for people and HUF and 20 kg for trusts and related entities notified by the federal government sometimes per fiscal yr (April – March).

Within the case of joint holding, the funding restrict of 4 kg will likely be utilized to the primary applicant solely. The annual ceiling will embody bonds subscribed beneath completely different tranches throughout preliminary issuance by the Authorities and people bought from the secondary market.

The ceiling on funding is not going to embody the holdings as collateral by banks and different Monetary Establishments.

#Curiosity Price

You’ll obtain a hard and fast rate of interest of two.50% each year payable semi-annually on the nominal worth. Such rate of interest is on the worth of cash you invested initially however not on the bond worth as on the date of curiosity payout.

Curiosity will likely be credited on to your account which you shared whereas investing.

# Problem Value

The value of SGB will likely be mounted in Indian Rupees based mostly on a easy common of closing value of gold of 999 purity, printed by the India Bullion and Jewellers Affiliation Restricted (IBJA) for the final three working days of the week previous the subscription interval. The difficulty value of the SGBs will likely be much less by Rs.50 per gram for the traders who subscribe on-line and pay by means of digital mode.

The federal government has mounted the difficulty value at Rs.6,263 per gram of gold. A reduction of Rs.50 per gram from the difficulty value to these traders who apply on-line. For such traders, the difficulty value of a Gold Bond will likely be Rs.6,213 per gram of gold.

# Cost Possibility

Cost shall be accepted in Indian Rupees by means of money as much as a most of Rs.20,000/- or Demand Drafts or Cheque or Digital banking. The place fee is made by means of cheque or demand draft, the identical shall be drawn in favor of receiving an workplace.

# Issuance Type

The Gold bonds will likely be issued as Authorities of India Inventory beneath the GS Act, 2006. The traders will likely be issued a Holding Certificates for a similar. The Bonds are eligible for conversion into Demat kind.

# The place to purchase Sovereign Gold Bond Scheme 2024 Collection 4?

Bonds will likely be bought by means of banks, Inventory Holding Company of India Restricted (SHCIL), designated Publish Workplaces (as could also be notified), and acknowledged inventory exchanges viz., Nationwide Inventory Trade of India Restricted and Bombay Inventory Trade, both instantly or by means of brokers.

Click on HERE to search out out the checklist of banks to Sovereign Gold Bond Scheme 2024 Collection 4.

# Mortgage in opposition to Bonds

The Bonds could also be used as collateral for loans. The Mortgage to Worth ratio will likely be relevant to abnormal gold loans mandated by the RBI sometimes. The lien on the Bonds shall be marked within the depository by the licensed banks. The mortgage in opposition to SGBs could be topic to the choice of the lending financial institution/establishment, and can’t be inferred as a matter of proper by the SGB holder.

# Liquidity of the Bond

As I identified above, after the fifth yr onwards you’ll be able to redeem the bond within the sixth or seventh yr. Nevertheless, the bond is accessible to promote within the secondary market (inventory change) on a date as notified by the RBI.

Therefore, you may have two choices. You’ll be able to redeem it within the sixth or seventh yr or promote it secondary market after the notification of RBI.

Do do not forget that the redemption value will likely be in Indian Rupees based mostly on the earlier week’s (Monday-Friday) easy common of the closing value of gold of 999 purity printed by IBJA.

# Nomination

You’ll be able to nominate or change the nominee at any time limit through the use of Type D and Type E. A person Non – resident Indian might get the safety transferred in his identify on account of his being a nominee of a deceased investor supplied that:

- The non-resident investor shall want to carry the safety until early redemption or until maturity, and

- the curiosity and maturity proceeds of the funding shall not be repatriable.

# Transferability

The Bonds shall be transferable by execution of an Instrument of switch as in Type ‘F’, in accordance with the provisions of the Authorities Securities Act, 2006 (38 of 2006) and the Authorities Securities Laws, 2007, printed partially 6, Part 4 of the Gazette of India dated December 1, 2007.

# Redemption

As I defined above, you may have the choice to redeem solely on the sixth, seventh, and eighth yr (computerized and finish of bond tenure). Therefore, there are two strategies one can redeem Sovereign Gold Bonds. Explaining each under.

a) On the maturity of the eighth yr– The investor will likely be knowledgeable one month earlier than maturity concerning the following maturity of the bond. On the completion of the eighth yr, each curiosity and redemption proceeds will likely be credited to the checking account supplied by the client on the time of shopping for the bond.

In case there are modifications in any particulars, similar to account quantity, or e-mail IDs, then the investor should inform the financial institution/SHCIL/PO promptly.

b) Redemption earlier than maturity – Should you plan to redeem earlier than maturity i.e. eighth yr, then you’ll be able to train this feature on the sixth or seventh yr.

It’s a must to strategy the involved financial institution/SHCIL workplaces/Publish Workplace/agent 30 days earlier than the coupon fee date. Request for untimely redemption can solely be entertained if the investor approaches the involved financial institution/publish workplace no less than at some point earlier than the coupon fee date. The proceeds will likely be credited to the client’s checking account supplied on the time of making use of for the bond.

# Taxation

There are three facets of taxation. Allow us to see one after the other.

1) Curiosity Revenue-The semi-annual curiosity earnings will likely be taxable earnings for you. Therefore, For somebody within the 10%, 20%, or 30% tax bracket, the post-tax return involves 2.25%, 2%, and 1.75% respectively. This earnings it’s a must to present beneath the pinnacle of “Revenue from Different Sources” and need to pay the tax accordingly (precisely like your Financial institution FDs).

2) Redemption of Bond-As I mentioned above, after the fifth yr onward you’re eligible to redeem it on the sixth,seventh, and eighth yr (final yr). Allow us to assume on the time of funding, the bond value is Rs.2,500 and on the time of redemption, the bond value is Rs.3,000. Then you’ll find yourself with a revenue of Rs.500. Such capital acquire arising on account of redemption by a person is exempted from tax.

3) Promoting within the secondary market of the Inventory Trade-There may be another taxation which will come up. Allow us to assume you purchase as we speak the Sovereign Gold Bond Scheme 2023-24 Collection I and promote it on the inventory change after a yr or so. In such a scenario, any revenue or loss from such a transaction will likely be thought-about as a capital acquire.

Therefore, if these bonds are bought within the secondary market earlier than maturity, then there are two potentialities.

# Earlier than 3 years-Should you promote the bonds inside three years and if there may be any capital acquire, such capital acquire will likely be taxed as per your tax slab.

# After 3 years – Should you promote the bonds after 3 years however earlier than maturity, then such capital acquire will likely be taxed at 20% with indexation.

There isn’t any idea of TDS. Therefore, it’s the accountability of traders to pay the tax as per the principles talked about above.

# Whom to strategy in case of any points?

The issuing banks/SHCIL workplaces/Publish Workplaces/brokers by means of which these securities have been bought will present different buyer providers similar to change of tackle, early redemption, nomination, grievance redressal, switch functions, and many others.

Together with this, a devoted e-mail has been created by the Reserve Financial institution of India to obtain queries from members of the general public on Sovereign Gold Bonds. Traders can mail their queries to this e-mail id. Beneath is the e-mail id

RBI E-mail ID in case of Sovereign Gold Bonds-[email protected]

Benefits Of Sovereign Gold Bond Scheme 2024 Collection 4

# After the GST entry, this Sovereign Gold Bond could also be advantageous over bodily Gold cash or bars. This product is not going to come beneath GST taxation. Nevertheless, within the case of Gold cash and bars, earlier the VAT was at 1% to 1.2%, which is now raised to three%.

# Should you maintain it until maturity or redeem it as and when the bonds are eligible, then the acquire is tax-free.

# In case your primary objective is to spend money on gold, then other than the bodily kind, investing in ETF or in Gold Funds, appears to be a greater choice. As a result of you don’t want to fret about bodily safekeeping, no fund prices (like ETF or Gold Funds) and the Demat account isn’t necessary.

# On this Sovereign Gold Bond Problem FY 2023-24, the extra profit other than the everyday bodily or paper gold funding is the annual curiosity fee on the cash you invested.

Therefore, there are two varieties of earnings potentialities. One is curiosity earnings from the funding and the second is value appreciation (if we’re constructive on gold). Therefore, together with value appreciation, you’ll obtain curiosity earnings additionally.

However do do not forget that such curiosity earnings is taxable. Additionally, to keep away from tax, it’s a must to redeem it solely on the sixth, seventh, or eighth yr. Should you promote within the secondary market, then such acquire or loss will likely be taxed as per capital tax acquire guidelines.

# There isn’t any TDS from the acquire. Therefore, you don’t want to fret in regards to the TDS half like Financial institution FDs.

# A sovereign assure of the Authorities of India will make you SAFE.

Disadvantages Of Sovereign Gold Bond Scheme 2024 Collection 4

# In case you are planning to spend money on your bodily utilization after 8 years, then merely avoid this. As a result of Gold is an asset, which provides you volatility just like the inventory market however the returns of your debt merchandise like Financial institution FDs or PPF.

# The important thing level to grasp can be that the curiosity earnings of two.5% is on the preliminary bond buy quantity however not the yearly bond worth. Therefore, allow us to say you invested Rs.2,500, then they pay curiosity of two.5% on Rs.2,500 solely although the worth of gold moved up and the worth of such funding is Rs.3,000.

# Liquidity is the largest concern. Your cash will likely be locked for five years. Additionally, redemption is accessible solely yearly after fifth yr.

In case you wish to liquidate in a secondary market, then it’s onerous to search out the precise value, and capital acquire tax might smash your funding.

# Sovereign assure of the Authorities of India might really feel you safe. Nevertheless, the redemption quantity is solely based mostly on the worth motion of the gold. Therefore, if there’s a fall within the gold value, then you’re going to get that discounted value solely. The one assure here’s a 2.5% return in your invested quantity and NO DEFAULT RISK.

Sovereign Gold Bond Scheme 2024 Collection 4 – Do you have to purchase?

Above I’ve shared my earlier posts on gold. You seen that gold can be a extremely unstable asset like fairness. Nevertheless, many people discover it onerous to consider.

In case you are nonetheless keen on gold, then somewhat than exposing your self to gold an excessive amount of, be certain that to have a correct asset allocation amongst completely different asset courses like fairness, debt, actual property, and gold. Don’t be obsessive about anyone single asset class and above that we’re uncertain of which asset class will carry out higher throughout OUR funding journey. Therefore, diversification needs to be your mantra.

Conclusion:- Put money into Sovereign Gold Bond Scheme 2024 Collection 4 in case your primary objective is to build up bodily gold after 8 years or so. Nevertheless, in case your objective is to have publicity to gold in your funding portfolio, then higher to remain away. As they’re illiquid, it’s onerous so that you can promote whereas doing the rebalancing exercise. As a substitute, go for extremely tradable Gold ETFs or Gold Funds (The price will enhance extra in comparison with ETF and each ETF and Gold Funds are taxed in a different way) are higher choices.

Suppose and make investments properly somewhat than BLIND funding.

[ad_2]