{kind=link}

[ad_1]

In a earlier publish, we described the fast progress of the stablecoin market over the previous few years after which mentioned the TerraUSD stablecoin run of Might 2022. The TerraUSD run, nonetheless, just isn’t the one episode of instability skilled by a stablecoin. Different noteworthy incidents embody the June 2021 run on IRON and, extra lately, the de-pegging of USD Coin’s secondary market value from $1.00 to $0.88 upon the failure of Silicon Valley Financial institution in March 2023. On this publish, primarily based on our latest workers report, we think about the next questions: Do stablecoin traders react to broad-based shocks within the crypto asset business? Do the traders run from the whole stablecoin business, or do they have interaction in a flight to safer stablecoins? We conclude with some high-level dialogue factors on potential laws of stablecoins.

Reactions to Market-Broad Shocks

We research the impression of turmoil within the crypto-asset business on stablecoin flows, specializing in giant declines within the value of bitcoin, which, though attributable to a number of components, characterize shocks to the general crypto ecosystem. Particularly, our evaluation makes use of information from January 2021 to March 2023 to estimate the impression of declines within the value of bitcoin on the web capital flows into stablecoins of various varieties and danger profiles.

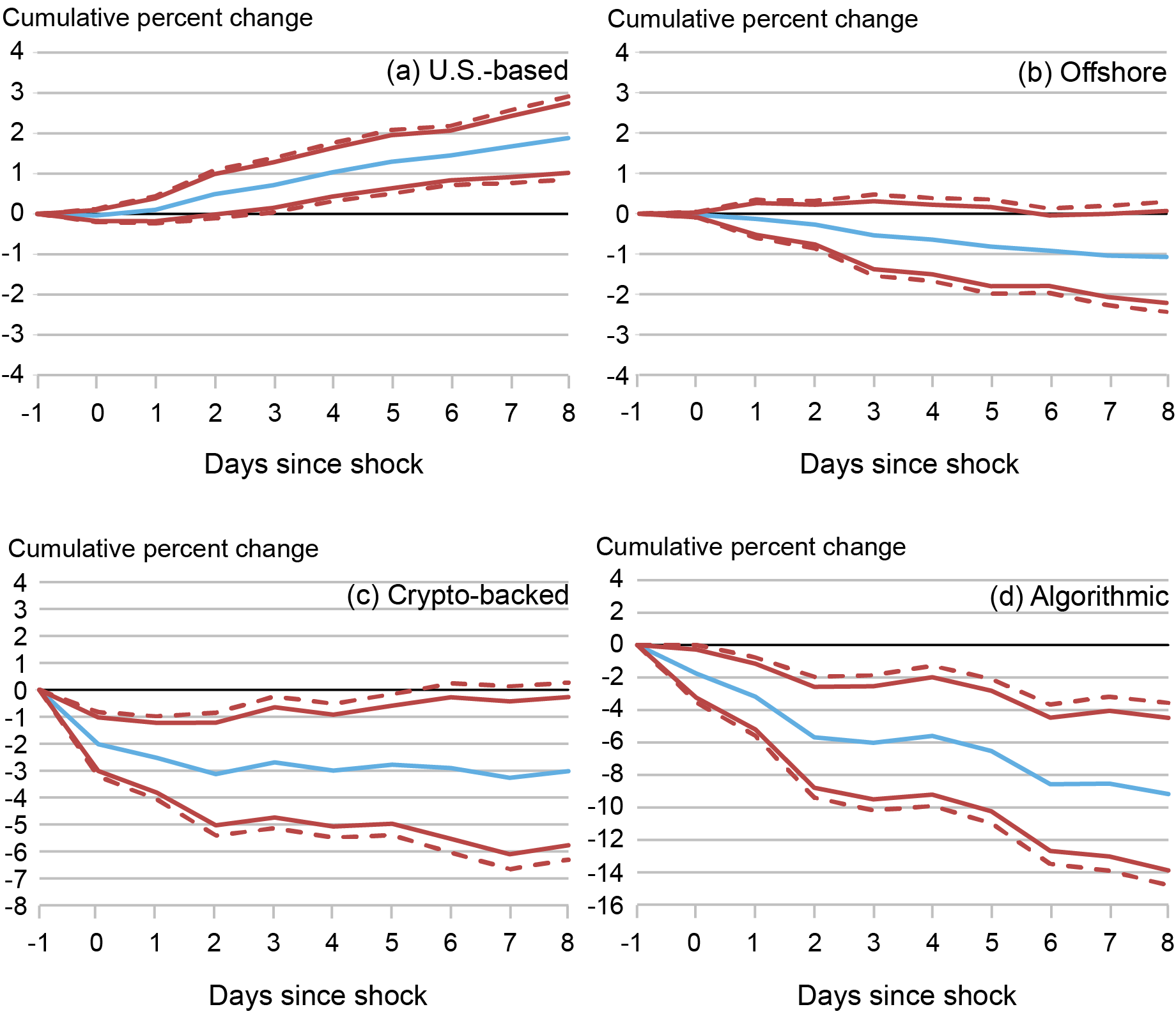

As we did in our earlier publish, we divide stablecoin issuers into 4 broad classes: i) U.S.-based, asset-backed stablecoins (for instance, USD Coin), that are backed by a portfolio of (largely conventional) U.S.-dollar denominated belongings, akin to U.S. Treasury securities and business paper; ii) offshore, asset-backed stablecoins (for instance, Tether), that are additionally backed by U.S.-dollar denominated belongings however are primarily based offshore; iii) crypto-backed stablecoins (for instance, DAI), that are issued towards different crypto-assets (usually with very risky costs), akin to Ether; and iv) algorithmic stablecoins (for instance, TerraUSD), which aren’t backed by collateral and whose pegging mechanism depends on a supply-demand matching algorithm that exploits arbitrage between costs of various crypto tokens.

We then estimate the impulse response of cumulative web flows into stablecoins to shocks in bitcoin costs utilizing native projections. The outcomes are depicted within the chart under. Our estimates present a transparent flight-to-safety sample: after a unfavourable bitcoin value shock, capital flows out of riskier stablecoins (offshore asset-backed, crypto-backed, and algorithmic; see panels (b)-(d)) and into much less dangerous ones (U.S.-based asset-backed; see panel (a)). Our outcomes suggest that when the every day change within the value of bitcoin is within the backside 5 % of its historic distribution, dangerous stablecoins expertise cumulative proportion outflows between about 1 and 9 %, relying on stablecoin sort, over the next eight days. In distinction, much less dangerous stablecoins expertise inflows of about 2 %. Additionally, the outflow is largest for algorithmic stablecoins, per the flight-to-safety speculation.

Impulse Response Capabilities for Varied Forms of Stablecoins to Bitcoin Value Shocks

These flight-to-safety flows are remarkably just like these skilled by cash market funds (MMFs) in periods of stress: In 2008 and 2020, traders redeemed closely from prime MMFs, which maintain riskier debt, and moved into authorities MMFs, which maintain largely U.S. Treasury and Company debt and repurchase agreements collateralized by these devices. These runs on MMFs amplified strains in short-term funding markets, which abated after extraordinary actions by the official sector. By the identical logic, if stablecoins had been to develop bigger and extra interconnected with the monetary markets, runs on stablecoins might additionally grow to be a supply of economic instability and probably require authorities intervention.

Dialogue

Stablecoins are newer devices than MMFs and extra heterogeneous, each by way of pricing and buying and selling mechanisms; moreover, most jurisdictions lack a strong regulatory framework for stablecoins. Thus, questions on methods to regulate them abound.

In a 2021 report, the President’s Working Group on Monetary Markets, the FDIC, and OCC really useful that stablecoins, notably these which can be used for funds, be “topic to applicable federal prudential oversight.” The report additionally highlighted the necessity to enhance transparency in stablecoin preparations, which could possibly be achieved, for instance, by imposing a extra uniform disclosure routine for stablecoins. After all, all regulatory choices entail tradeoffs, and one must steadiness their prices with the advantages, mainly these related to improved investor safety and monetary stability.

Summing Up

Along with idiosyncratic run episodes skilled by algorithmic stablecoins in 2022, stablecoins additionally exhibit systematic flight-to-safety flows in periods of broad-based stress within the crypto asset market. That’s, traders are likely to run from stablecoins perceived as riskier into stablecoins perceived as much less dangerous throughout such episodes. These dynamics are remarkably just like these noticed in MMFs in periods of stress.

Kenechukwu Anadu is a vp within the Federal Reserve Financial institution of Boston’s Supervision, Regulation, and Credit score Division.

Pablo Azar is a monetary analysis economist in Cash and Funds Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Marco Cipriani is the top of Cash and Funds Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Thomas M. Eisenbach is a monetary analysis advisor in Cash and Funds Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Catherine Huang served as a analysis analyst on the Federal Reserve Financial institution of New York and is a Ph.D. candidate in Enterprise Economics at Harvard College.

Mattia Landoni is a senior monetary economist within the Federal Reserve Financial institution of Boston’s Supervision, Regulation, and Credit score Division.

Gabriele La Spada is a monetary analysis advisor in Cash and Funds Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Marco Macchiavelli is an assistant professor of finance on the College of Massachusetts Amherst.

Antoine Malfroy-Camine is a danger analyst within the Federal Reserve Financial institution of Boston’s Supervision, Regulation, and Credit score Division.

J. Christina Wang is a senior economist and coverage advisor within the Federal Reserve Financial institution of Boston’s Analysis Division.

The right way to cite this publish:

Kenechukwu Anadu, Pablo D. Azar, Marco Cipriani, Thomas Eisenbach, Catherine Huang, Mattia Landoni, Gabriele La Spada, Marco Macchiavelli, Antoine Malfroy-Camine, and J. Christina Wang, “Stablecoins and Crypto Shocks,” Federal Reserve Financial institution of New York Liberty Road Economics, March 8, 2024, https://libertystreeteconomics.newyorkfed.org/2024/03/stablecoins-and-crypto-shocks/.

Disclaimer

The views expressed on this publish are these of the creator(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the creator(s).

[ad_2]