{kind=link}

[ad_1]

This publish presents an replace of the financial forecasts generated by the Federal Reserve Financial institution of New York’s dynamic stochastic common equilibrium (DSGE) mannequin. We describe very briefly our forecast and its change since September 2023. As ordinary, we want to remind our readers that the DSGE mannequin forecast shouldn’t be an official New York Fed forecast, however solely an enter to the Analysis workers’s total forecasting course of. For extra details about the mannequin and variables mentioned right here, see our DSGE mannequin Q & A.

The New York Fed mannequin forecasts use knowledge launched via 2023:Q3, augmented for 2023:This autumn with the median forecasts for actual GDP progress and core PCE inflation from the November launch of the Philadelphia Fed Survey of Skilled Forecasters, in addition to the yields on 10-year Treasury securities and Baa-rated company bonds based mostly on 2023:Q3 averages as much as November 21. Beginning in 2021:This autumn, the anticipated federal funds price (FFR) between one and 6 quarters into the longer term is restricted to equal the corresponding median level forecast from the most recent accessible Survey of Main Sellers (SPD) within the corresponding quarter. For the present projection, that is the November SPD.

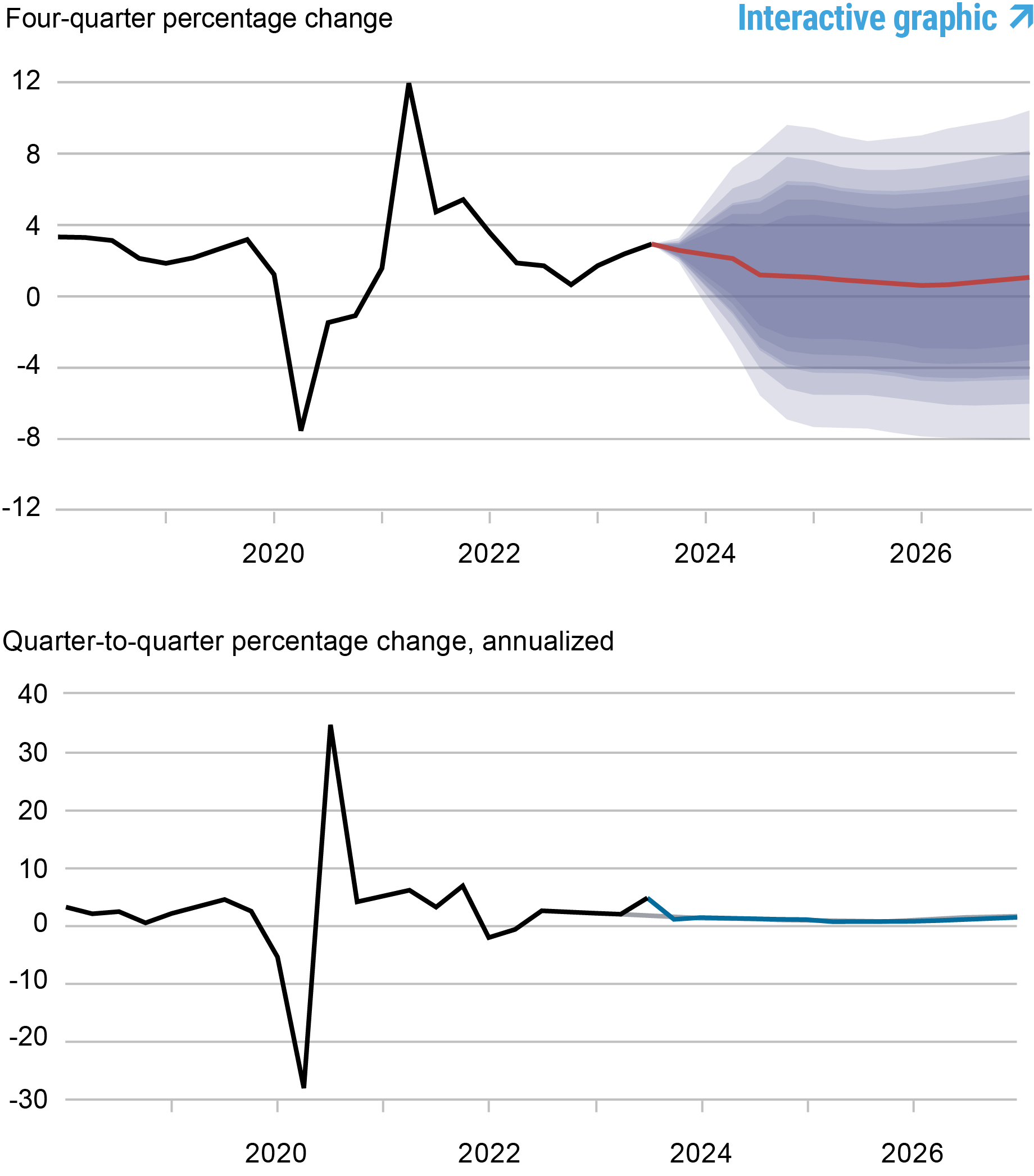

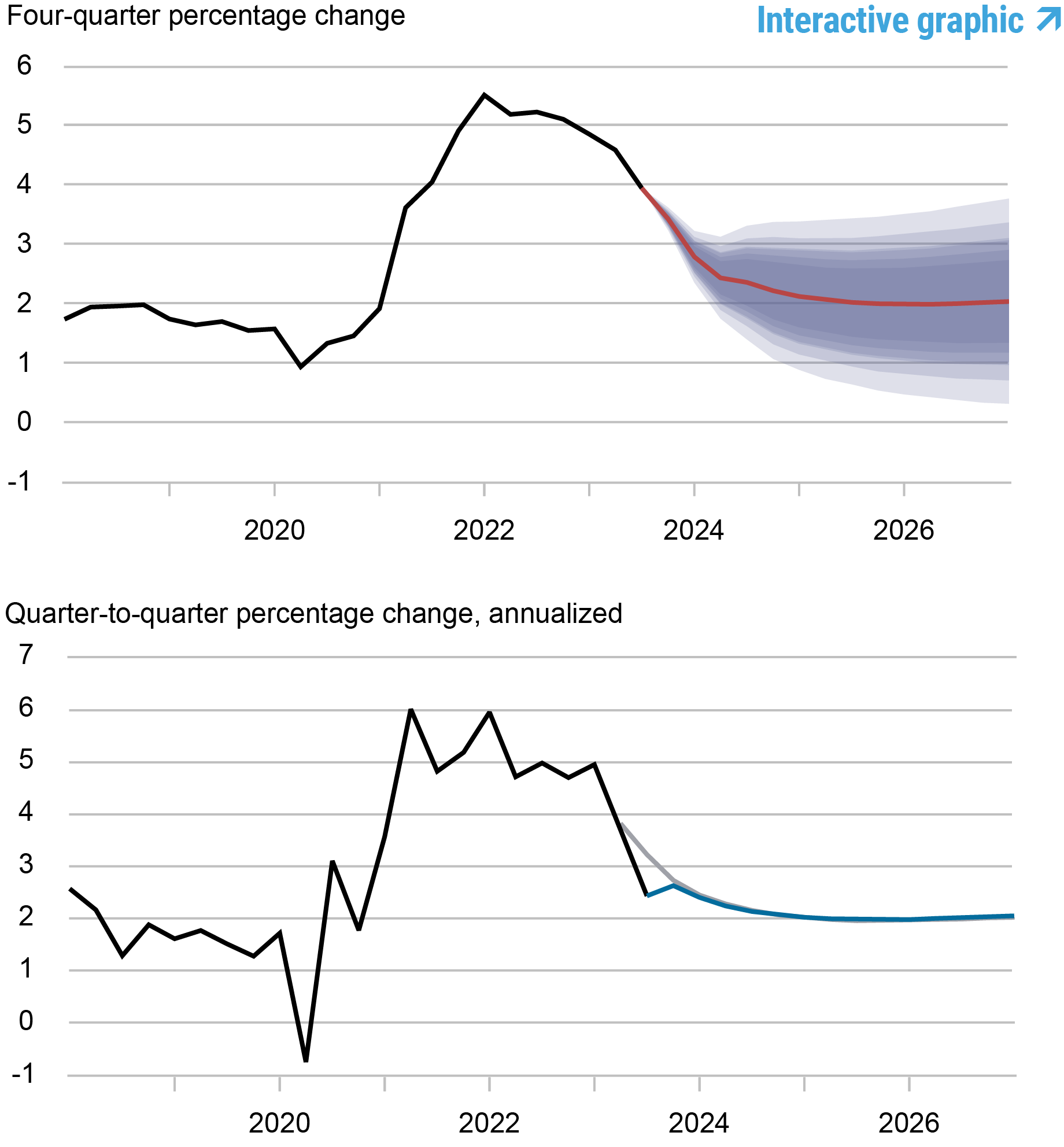

The financial system turned out to be stronger in Q3 than predicted by the mannequin. This forecast error naturally pushes up the output progress forecast for the present yr however has solely a small impression on projections for exercise in any other case. The mannequin expects output progress to be 0.7 share factors greater in 2023 than forecasted in September (2.6 versus 1.9 %) however not very totally different from the September predictions for the remainder of the forecast horizon (1.2, 0.7, and 0.9 % in 2024, 2025, and 2026, versus 1.1, 0.7, and 1.2 % in September, respectively). The output hole is projected to be considerably decrease in 2023 than was predicted in September, because the mannequin attributes the current power of the financial system primarily to produce moderately than demand components. The output hole predictions are much like these made in September for the rest of the forecast horizon. Inflation projections are decrease in 2023 than they had been in September (3.4 versus 3.7 %), largely as a result of Q3 inflation stunned the mannequin on the draw back. The anticipated path for inflation is unchanged in any other case: 2.2 % in 2024 and a pair of.0 % in 2025 and 2026.

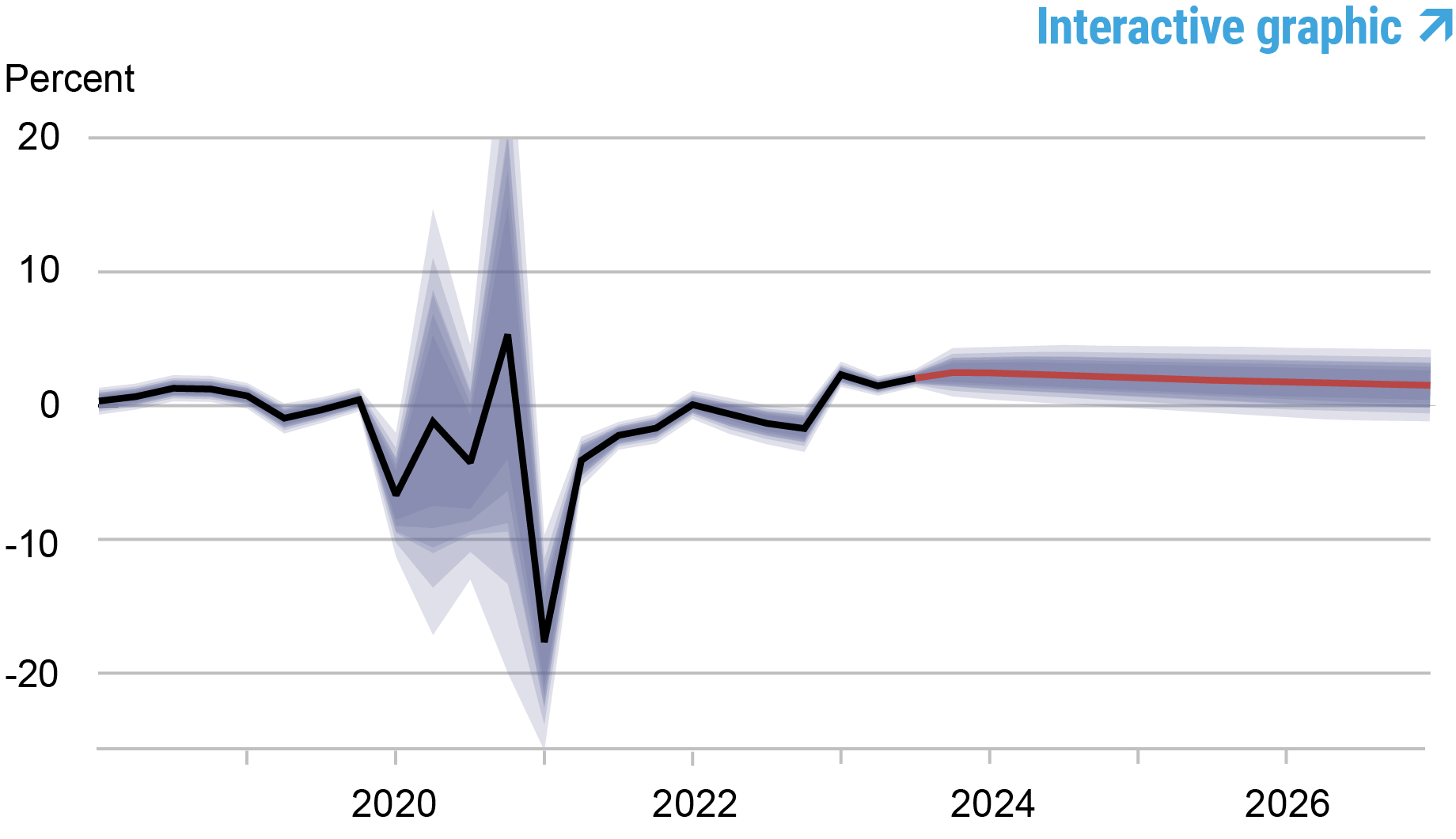

The short-run actual pure price of curiosity is anticipated to stay on the similar elevated degree as projected in September for 2023 (2.5 %), declining to 2.2 % in 2024, 1.8 % in 2025, and 1.6 % in 2026. The anticipated path of the coverage price is actually unchanged relative to September. The mannequin sees financial coverage as being restrictive via the top of 2024 within the sense that the FFR in actual phrases is above the short-term pure price of curiosity.

Forecast Comparability

| Forecast Interval | 2023 | 2024 | 2025 | 2026 | ||||

|---|---|---|---|---|---|---|---|---|

| Date of Forecast | Dec 23 | Sep 23 | Dec 23 | Sep 23 | Dec 23 | Sep 23 | Dec 23 | Sep 23 |

| GDP progress (This autumn/This autumn) |

2.6 (2.2, 3.0) |

1.9 (0.2, 3.6) |

1.2 (-3.8, 6.2) |

1.1 (-4.0, 6.3) |

0.7 (-4.3, 5.7) |

0.7 (-4.4, 5.8) |

0.9 (-4.5, 6.3) |

1.2 (-4.2, 6.6) |

| Core PCE inflation (This autumn/This autumn) |

3.4 (3.3, 3.5) |

3.7 (3.4, 3.9) |

2.2 (1.5, 2.9) |

2.2 (1.5, 3.0) |

2.0 (1.1, 2.9) |

2.0 (1.1, 2.9) |

2.0 (1.0, 3.0) |

2.0 (1.0, 3.0) |

| Actual pure price of curiosity (This autumn) |

2.5 (1.4, 3.5) |

2.5 (1.3, 3.7) |

2.2 (0.8, 3.6) |

2.2 (0.8, 3.7) |

1.8 (0.3, 3.3) |

1.9 (0.3, 3.4) |

1.6 (0.0, 3.2) |

1.6 (0.0, 3.3) |

Notes: This desk lists the forecasts of output progress, core PCE inflation, and the actual pure price of curiosity from the December 2023 and September 2023 forecasts. The numbers exterior parentheses are the imply forecasts, and the numbers in parentheses are the 68 % bands.

Forecasts of Output Development

Notes: These two panels depict output progress. Within the high panel, the black line signifies precise knowledge and the pink line exhibits the mannequin forecasts. The shaded areas mark the uncertainty related to our forecasts at 50, 60, 70, 80, and 90 % likelihood intervals. Within the backside panel, the blue line exhibits the present forecast (quarter-to-quarter, annualized), and the grey line exhibits the September 2023 forecast.

Forecasts of Inflation

Notes: These two panels depict core private consumption expenditures (PCE) inflation. Within the high panel, the black line signifies precise knowledge and the pink line exhibits the mannequin forecasts. The shaded areas mark the uncertainty related to our forecasts at 50, 60, 70, 80, and 90 % likelihood intervals. Within the backside panel, the blue line exhibits the present forecast (quarter-to-quarter, annualized), and the grey line exhibits the September 2023 forecast.

Actual Pure Charge of Curiosity

Notes: The black line exhibits the mannequin’s imply estimate of the actual pure price of curiosity; the pink line exhibits the mannequin forecast of the actual pure price. The shaded space marks the uncertainty related to the forecasts at 50, 60, 70, 80, and 90 % likelihood intervals.

Marco Del Negro is an financial analysis advisor in Macroeconomic and Financial Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Pranay Gundam is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Donggyu Lee is a analysis economist in Macroeconomic and Financial Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Ramya Nallamotu is a senior analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Brian Pacula is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Tips on how to cite this publish:

Marco Del Negro, Pranay Gundam, Donggyu Lee, Ramya Nallamotu, and Brian Pacula, “The New York Fed DSGE Mannequin Forecast—December 2023,” Federal Reserve Financial institution of New York Liberty Road Economics, December 15, 2023, https://libertystreeteconomics.newyorkfed.org/2023/12/the-new-york-fed-dsge-model-forecast-december-2023/.

Disclaimer

The views expressed on this publish are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the writer(s).

[ad_2]