{kind=link}

[ad_1]

Yves right here. The Fed retains attempting to rein in inflation with fee hikes, which as now we have repeatedly identified, will do little to test price improve which aren’t the results of a wage-price spiral. This inflation began out with provide shocks. Inflation was extraordinarily excessive in some sectors, akin to vitality, lumber, and meals, laborious to see in others. That isn’t the sample you see with demand-pull inflation. On high of that, now we have different components that the Fed is just not well-disposed to contemplate, akin to “greedflation” and lengthy Covid constraining the labor provide.

On high of that, we see perilous little point out that the Biden Administration engaged in an insane degree of fiscal stimulus in 2023 on condition that the Fed was attempting laborious to hit the brakes, with the deficit amounting to six.2% of GDP. So the central financial institution is certainly seeing the potential for an enormous uptick in spending, not primarily from shoppers as you’d anticipate in historic demand-pull inflation, however companies if the Fed relents.

By Wolf Richter, editor of Wolf Avenue. Initially printed at Wolf Avenue

If it’s unleashed on the “first trace” of a fee minimize, it “would create upward strain on costs.” However it could be too late, it has been unleashed by rate-cut mania.

Atlanta Fed President Raphael Bostic got here up with a brand new danger to the inflation state of affairs, or not likely a brand new danger – as a result of it’s been there and it’s already occurring – however a brand new phrase to explain that danger, a phrase that can resonate right here: “pent-up exuberance.”

“Pent-up exuberance” is that companies, “able to pounce,” would unleash a torrent of latest hiring and funding on the “first trace of an rate of interest minimize,” which might unleash inflation over again.

It has already been occurring. The speed-cut mania has loosened monetary circumstances to pre-rate-hike ranges, employment has surged over the previous few months, hourly earnings have spiked, and inflation in providers has begun to re-accelerate. So this rate-cut mania has already unleashed the primary wave of this “pent-up exuberance.” And Bostic nodded in that path:

“It’s untimely to say victory within the struggle towards inflation,” Bostic mentioned in his speech. “January inflation readings got here in surprisingly excessive, the most recent reminder that the trail to cost stability is just not a straight line.”

There’s a “New Upside Danger” in City: “Pent-Up Exuberance.”

“As my workers and I’ve talked to enterprise decision-makers in latest weeks, the theme we’ve heard rings of expectant optimism. Regardless of enterprise exercise broadly moderating, corporations will not be distressed. As an alternative, many executives inform us they’re on pause, able to deploy belongings and ramp up hiring when the time is true,” Bostic mentioned.

“I requested one gathering of enterprise leaders in the event that they had been able to pounce on the first trace of an rate of interest minimize. The response was an awesome ‘sure,’” he mentioned.

“If that state of affairs had been to unfold on a big scale, it holds the potential to unleash a burst of latest demand that might reverse the progress towards rebalancing provide and demand. That may create upward strain on costs,” he mentioned.

“This risk of what I’ll name pent-up exuberance is a brand new upside danger that I feel bears scrutiny in coming months,” he mentioned.

Worry that this “pent-up exuberance” might reignite – or already has reignited – the inflation hearth is legitimate. We’ve seen situations over the previous few months.

Placing three fee cuts in 2024 into the dot plot on the FOMC’s December assembly and letting markets assume six or seven fee cuts in 2024 and run wild with this rate-cut mania, has turned out to be a strategic blunder of colossal proportions by the Fed.

And ever since, Fed officers have been backpedaling on the speed minimize state of affairs, and markets have dialed again their rate-cut mania by a few notches. However it could be too late. That pent-up exuberance could have already gotten out of the bull pen, and it’s doing its darndest to make the inflation struggle tougher and longer.

Right here’s That Un-Pent Exuberance at Work

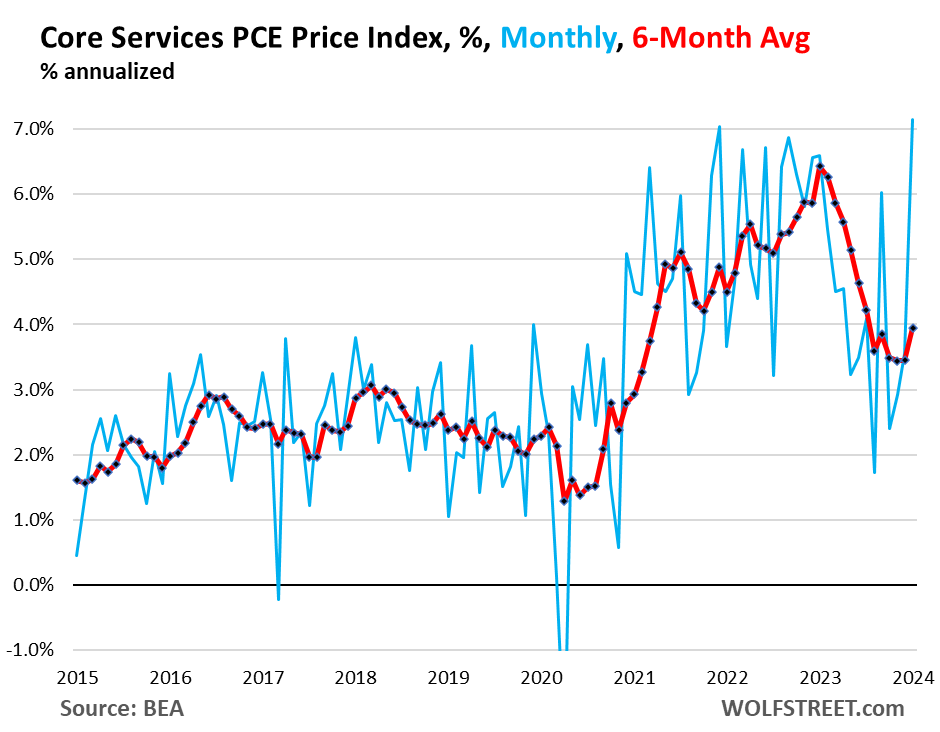

The core providers PCE value index spiked to 7.15% annualized in January from December, the worst month-to-month bounce in 22 years (blue line). Drivers of the spike had been non-housing measures in addition to housing inflation. The six-month shifting common, which irons out the month-to-month volatility however is slower to react, accelerated to three.95% annualized, the worst since July, after having gotten caught on the 3.5% degree for 3 months in a row (crimson):

[ad_2]