{kind=link}

[ad_1]

hree years have handed since inflation started its surge in Spring 2021, which continued till early 2023. Because the inflation fee has since begun a hesitant decline, the time has come to look again at and mirror on what has occurred throughout these difficult years. A current analysis of the causes of U.S. pandemic inflation comes from Ben Bernanke and Olivier Blanchard (2023), who (in their very own phrases) use a easy dynamic mannequin of wage-price dedication to clarify the sharp acceleration in U.S. inflation throughout 2021-2023. The Bernanke and Blanchard mannequin evaluation gives a consultant specimen of the method taken by institution economists to the current inflationary disaster, because it contains every little thing essential that’s problematic about New Keynesian macroeconomics.

Distinguished central bankers, together with Federal Reserve Chair Jerome Powell[1] and ECB President Christine Lagarde[2], take a quite totally different view once they state that their coverage fee selections, in these turbulent and unsure occasions, are based mostly on a data-driven method, and never on commonplace macro fashions or financial coverage guidelines derived from these commonplace fashions. These central bankers are clear that commonplace macro fashions are of little use to them within the present macroeconomic atmosphere that’s significantly fluid economically and politically at home and world ranges (Ferguson and Storm 2023).

Bernanke and Blanchard beg to disagree. With the advantage of hindsight, they current and estimate their easy dynamic mannequin of costs, wages, and short-run and long-run inflation expectations which they declare intently tracks the pandemic-era inflation. Primarily based on their evaluation, Bernanke and Blanchard (2023, pp. 38-39) confidently conclude that “… we don’t assume that the current expertise justifies throwing out present fashions of wage-price dynamics.” The paper of Bernanke and Blanchard constitutes one other contribution to – what I’ve elsewhere (Storm 2023a) – referred to as the artwork of sustaining the New Keynesian paradigm. How convincing is the mannequin evaluation by Bernanke and Blanchard? How empirically related are their mechanisms inflicting inflation – and the way strong and believable are their econometric findings? In a new INET working paper, I reply these questions based mostly on a vital evaluation of the mannequin evaluation of Bernanke and Blanchard.

Bernanke and Blanchard’s (2023) Findings – However Put into Context

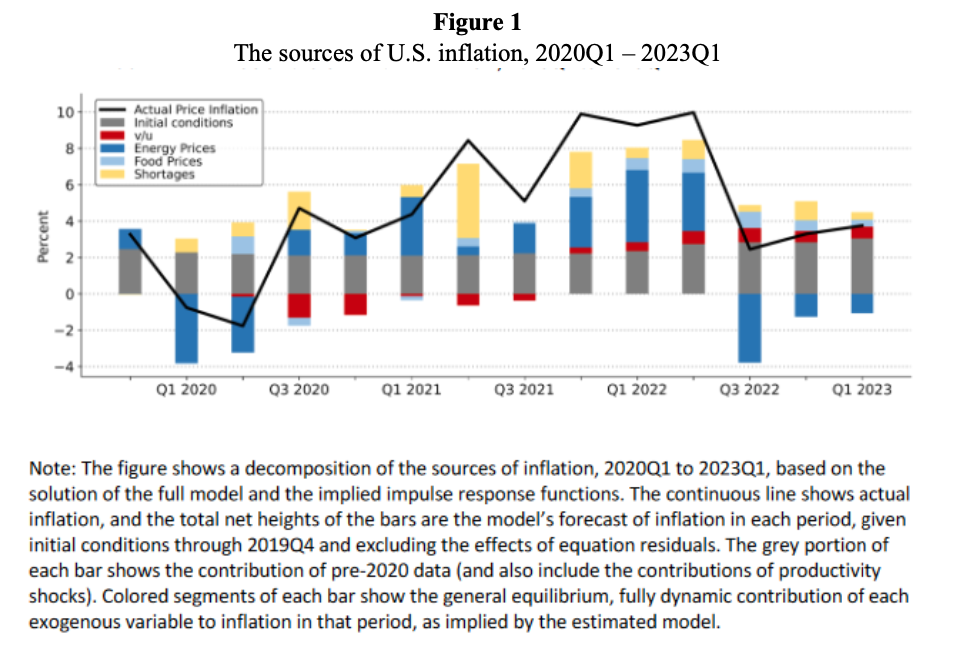

Bernanke and Blanchard’s reply to the query posed by the title of their paper (“What precipitated the U.S. pandemic inflation?”) is given in Determine 12, reproduced right here as Determine 1. The determine reveals the decomposition of the U.S. Client Value Index (CPI) inflation fee throughout the interval 2020Q1-2023Q1, which is predicated on the estimated model of the dynamic mannequin of the 2 authors. The quarterly CPI inflation fee, at annualized charges, is decomposed into the next three contributions: (1) preliminary circumstances (which embody the fixed phrases within the estimated equations in addition to the exogenous fee of labor productiveness progress); (2) supply-side shocks to power and meals costs and world provide chains that increase manufacturing prices; and (3) the job emptiness ratio 𝑣/𝑢, which captures the inflationary impression of tight labor market circumstances.

The surge within the CPI inflation fee – from 2.8% within the fourth quarter of 2020 to a peak of 9.7% within the second quarter of 2022 – is overwhelmingly because of the supply-side shocks that raised manufacturing prices. This isn’t stunning, as that is precisely what any data-driven method would additionally reveal. A visible inspection of Determine 1 means that supply-side shocks have been liable for round two-thirds to three-fourths of the surge within the inflation fee throughout 2020Q4 and 2022Q2.

The contribution of ‘preliminary circumstances’ to the U.S. inflation fee is discovered to be roughly fixed over the interval of research, at round 2 share factors.

Lastly, and importantly, the contribution to inflation of tight labor-market circumstances—the principle concern of many early critics of U.S. financial and monetary insurance policies (Summers 2021; Blanchard 2021; Summers and Domash 2022)—was detrimental throughout the first two quarters of 2021 and optimistic however minuscule throughout 2021Q3-2023Q2.

This discovering is placing as a result of the U.S. labor market is meant to have been ‘extraordinarily tight’, even ‘purple scorching’, as a result of the job emptiness ratio (the variety of job openings per unemployed employee, or 𝑣/𝑢) rose to 1.9 job openings per unemployed employee within the second quarter of 2022 – a stage significantly larger than in any ancient times since these information have been collected.

Studying between the traces, it’s clear that Bernanke and Blanchard are unpleasantly stunned by the invention that the ‘extraordinarily excessive’ emptiness ratio throughout the post-pandemic interval didn’t considerably contribute to the rise within the CPI inflation fee. The cognitive dissonance have to be massive. The reason being that their discovering of a pitiful contribution of 𝑣/𝑢 to rising inflation doesn’t match the established narrative that the current bout of inflation will need to have been brought on by expansionary fiscal insurance policies, resulting in an overheated labor market and to a scenario during which precise output exceeds the economic system’s potential. On this omnipresent narrative, President Biden’s ‘extreme’ COVID aid spending and the much more ‘cavalier’ $1.9 trillion American Rescue Plan are generally singled out to have stoked inflation by pushing precise output above potential and by overheating the labor market (Blanchard 2021; Summers 2021).

Contradicting this narrative, the Working Paper reveals that the output hole of the U.S. economic system hovered round zero throughout 2021Q1-2023Q4, proper when the speed of CPI inflation started its surge. The (near) zero output hole does not sign a structurally overheated American economic system – and additionally it is not aligned with claims of a ‘red-hot’ labor market and a traditionally unprecedented job emptiness ratio of practically 2.

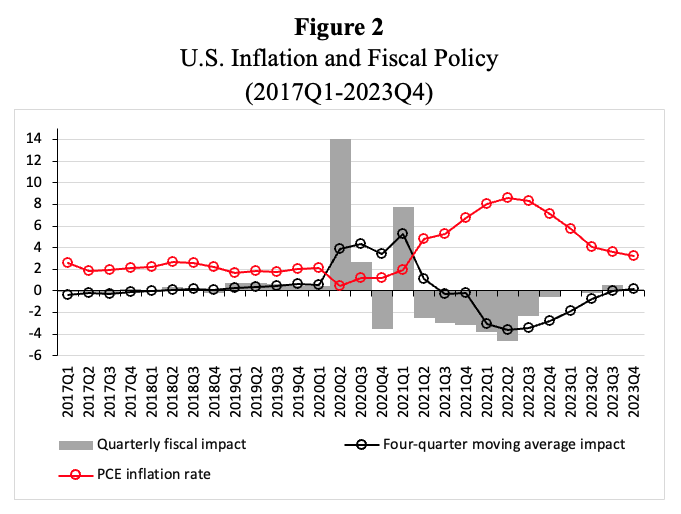

The established narrative blaming the inflation on the Biden aid spending throughout 2021 will get one other blow when one considers Determine 2, which reveals the contribution of the fiscal coverage stance to actual GDP progress throughout 2017Q1-2023Q4. It may be seen that the contribution of fiscal coverage to actual GDP progress has been detrimental throughout 2021Q2-2023Q3, amounting to —4.6% within the second quarter of 2022. Throughout 2021Q2-2023Q3, fiscal coverage has been a major drain on financial progress. It’s not believable to attribute the surge in U.S. inflation to the de facto fiscal austerity of the Biden administration.

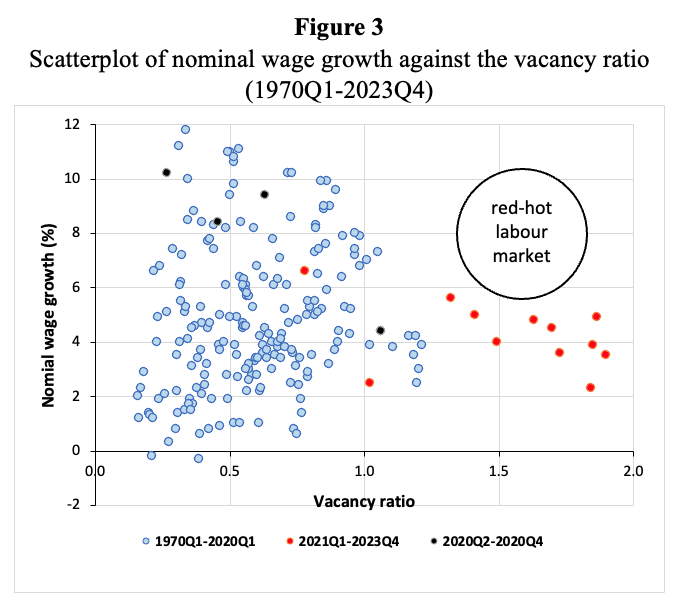

Lastly, Determine 3 presents direct quarterly proof of the connection between the emptiness ratio and nominal wage progress for 53 years (1970Q1-2023Q4). Nominal wage progress is measured by the expansion fee of hourly compensation of all employees within the U.S. non-farm enterprise sector. The observations for the ‘tight-labor-market’ interval 2021Q3-2023Q4 seem in purple; the 4 observations for the yr 2020 are in black. It’s evident that the interval 2021Q3-2023Q4 is traditionally distinctive when it considerations the extent of the emptiness ratio, however is totally odd or common when it comes to the expansion fee of nominal earnings.

The extraordinarily excessive emptiness ratio did, due to this fact, not result in significantly excessive nominal wage progress – one other inconvenient indisputable fact that contradicts claims of an operative wage-price inflation spiral.

However Bernanke and Blanchard don’t surrender. They conclude their paper by presenting model-based inflation projections for the interval 2023Q1-2027Q1, based mostly on three various (low, medium, and excessive) eventualities for 𝑣/𝑢. If 𝑣/𝑢 stays completely at a stage of 1.8 job openings per unemployed employee, inflation will stay excessive and effectively above the putative inflation goal of two%. This conclusion brings us into harmful coverage territory. Bernanke and Blanchard (2023, p.38) finish by concluding that

“[A]s of early 2023, tight labor market circumstances nonetheless accounted for a minority share of extra inflation. However based on our evaluation, that share is more likely to develop and won’t subside by itself. The portion of inflation which traces its origin to overheating of labor markets can solely be reversed by coverage actions that deliver labor demand and provide into higher steadiness.”

Therefore, the conclusion is that “labor-market steadiness ought to in the end be the first concern for central banks trying to keep up worth stability.” Financial coverage thus has to stay tight, as a result of it has to create the additional unemployment that’s essential to deliver down the 𝑣/𝑢 ratio, decrease nominal wage progress and convey again inflation to 2%. Nonetheless, the coverage conclusions are solely related when the mannequin evaluation is sound and credible.

The Wage-Value Spiral Mannequin: A Critique

As is argued within the Working Paper, the econometric findings of Bernanke and Blanchard have to be taken with a couple of pinches of salt. Leaving apart questions regarding the quite eccentric econometrics underlying the mannequin evaluation, it is very important observe that Bernanke and Blanchard’s estimate of the impression of a rise within the job emptiness ratio on nominal wage progress significantly exaggerates the inflationary results of a good labor market, as it’s extra than twice as massive as different, extra dependable estimates of the identical impact within the literature. Regardless of this ‘bias’ in favor of wage-push inflation, Bernanke and Blanchard discover that (exogenous) supply-side shocks have been liable for round two-thirds to three-fourths of the surge within the inflation fee throughout 2020Q4 and 2022Q2, whereas the contribution to inflation of tight labor-market circumstances was detrimental throughout the first two quarters of 2021 and optimistic however minuscule throughout 2021Q3-2023Q2 (Determine 1).

Nonetheless, extra essential than the weak econometrics are main considerations with respect to the interior logic of the easy dynamic New Keynesian mannequin that Bernanke and Blanchard make use of to determine the causes of the U.S. pandemic-era inflation. Two points stand out.

First, it’s claimed {that a} completely tighter labor market results in completely larger inflation. This sounds very harmful, however the final result of completely rising inflation is predicated on the non-plausible inflation-expectations channel, formalized by Bernanke and Blanchard, that doesn’t survive a confrontation with financial actuality and empirical proof. This inflation expectations channel is predicated on two contradictory (and equally unrealistic) assumptions. On the one hand, U.S. employees are assumed to own the bargaining energy to pressure companies to pay nominal wage will increase according to will increase in short-run anticipated inflation. This presupposes a employee wage bargaining energy that palpably doesn’t exist (Stansbury and Summers 2020).

However, these highly effective, forward-looking employees don’t strongly ratchet up their inflation expectations within the face of a sudden surge in precise inflation, as a result of their inflation expectations are well-anchored within the perception that the Federal Reserve will shortly and successfully deliver inflation right down to its goal. Consequently, inflation expectations completely fall in need of precise inflation, which is – on this mannequin – a cause why the acceleration of inflation is going on in slow-motion; it takes a few years earlier than the Phillips curve turns into vertical, however, as everyone knows, “The long term is a deceptive information to present affairs. In the long term we’re all lifeless,” as John Maynard Keynes wrote in his 1923 work, A Tract on Financial Reform.

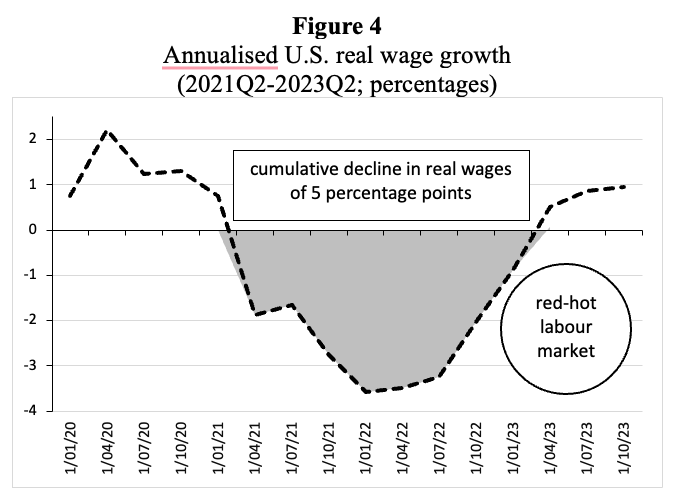

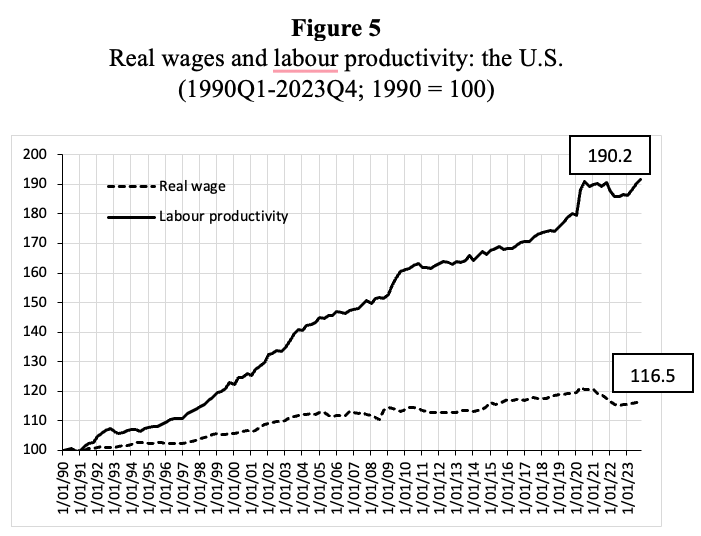

It’s a thriller why Bernanke and Blanchard assume that American employees are capable of increase wages according to anticipated inflation and on the identical time are gullible sufficient to consider that the Fed’s inflation concentrating on is credible. It’s not, as a result of the results of financial tightening on inflation are restricted and take time to construct, with the outcome that employees must undergo a chronic interval of actual wage declines. As is proven in Determine 4, as a result of nominal wage progress fell in need of the CPI inflation fee throughout 2021Q2-2023Q2, employees needed to swallow a cumulative actual wage decline of round 5 share factors. Allow me to repeat the plain level that that is precisely the interval throughout which the U.S. labor market is meant to have been ‘purple scorching’, with a job emptiness ratio of just about 2 job openings per unemployed employee.

Bernanke and Blanchard argue that the extended decline in actual wages has been brought on by unanticipated provide shocks that raised prices and, therefore, costs. Employees, of their view, behaved rationally by placing religion within the Fed’s means to regulate inflation, as a result of the inflationary final result would have been far worse if that they had executed in any other case. In spite of everything, if American employees had determined to assert larger nominal wage progress in response to the sudden supply-side-driven surge in inflation, inflation expectations would have change into un-anchored, and the inflation fee would have accelerated extra and quicker. Thank goodness, American employees are actual patriots who know what must be executed throughout a nationwide emergency: preserve belief within the courageous inflation fighters of the Federal Reserve.

This leads us to a second, even larger drawback in Bernanke and Blanchard’s mannequin: Bernanke and Blanchard assume that American employees have wage bargaining energy, which they use to guard their actual wages. Within the mannequin’s regular state, actual wage progress equals (exogenous) labor productiveness progress. This isn’t a bug, however a characteristic of their mannequin, behind which the financial actuality – for ages, actual wages have didn’t sustain with labor productiveness progress, and the labor earnings share is in secular decline – has been hidden. Determine 5 illustrates the purpose.

Therefore, U.S. actual wages aren’t downwardly inflexible however quite have been falling relative to labor productiveness. Slightly than being a supply of inflationary stress, actual wages have acted as an absorber of inflationary shocks. By constructing real-wage rigidity into their mannequin, by way of the inflation-expectations channel, Bernanke and Blanchard once more exaggerate the inflationary penalties of a good labor market and of value shocks. Their mannequin evaluation is biased, designed to show the supposedly Very Critical Inflationary Penalties of an exaggerated tightness of the labor market, setting financial policymakers as much as ship considerably extra financial tightening than may be justified on the premise of other and arguably extra reasonable mannequin analyses (e.g., Honest 2021, 2022).

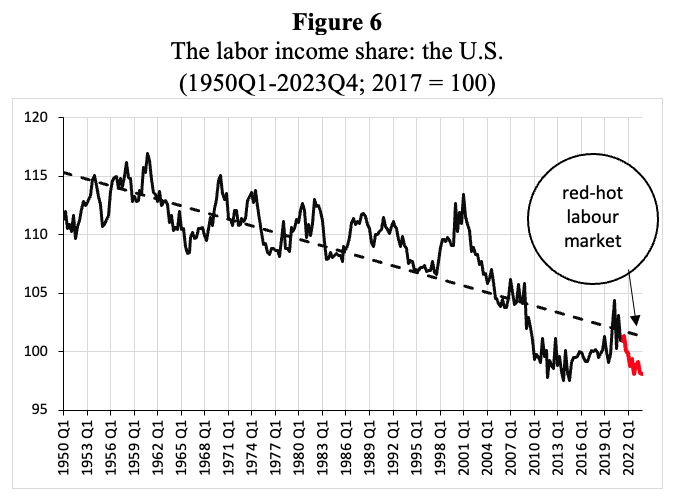

In doing so, Bernanke and Blanchard handle to disregard the only most essential stylized truth on the post-1980 U.S. economic system: the secular decline within the labor earnings share (Determine 6). The declining labor earnings share is a direct consequence of the decline in employee (union) energy (Stansbury and Summers 2020), which, in flip, is in step with one other salient facet of the macroeconomic expertise of the U.S. in current many years: the substantial decline in each unemployment and inflation, mirrored within the flattening of the value Phillips curve (Storm 2023a).

Bernanke and Blanchard overlook, or refuse to think about, the truth that employee energy has dwindled within the U.S., as many women and men needed to go from steady, decently paying jobs in factories and shops to insecure work within the gig or providers economic system – and the decline of private-sector unions has resulted within the near-monopoly of political lobbying about non-public sector financial points by company and shareholder pursuits, influencing Democrats and Republicans alike. Likewise, Bernanke and Blanchard don’t want to entertain the likelihood that a number of the inflation surge throughout 2021Q2-2023Q4 have to be attributed to will increase in company revenue markups (Storm 2023b) and hypothesis in oil and power markets (Breman and Storm 2023). These are errors of fee, not omission, and they don’t seem to be impartial, however present an apologetics for an unequal, unjust, oppressive, and politically unstable social order (Rudd 2022).

It’s not stunning, due to this fact, that the Federal Reserve and different central banks use a data-driven method to their financial coverage selections. The established New Keynesian fashions are of no use. The state of macro shouldn’t be good.

_____________

[1] For instance, at a press convention on July 26, 2023, Powell (2023) mentioned, “Wanting forward, we’ll proceed to take a data-dependent method in figuring out the extent of further coverage firming that could be acceptable.”

[2] In line with Lagarde (2023), President of the European Central Financial institution, the “elevated stage of uncertainty reinforces the significance of a data-dependent method to our coverage fee selections, which shall be decided by our evaluation of the inflation outlook in mild of the incoming financial and monetary information, the dynamics of underlying inflation, and the power of financial coverage transmission.”

See unique publish for references

[ad_2]