{kind=link}

[ad_1]

With so many several types of essential sickness (CI) insurance coverage, how does one go about selecting?

We finally attain a stage of life the place we realise that when essential sickness strikes, it doesn’t actually care about your loved ones historical past, what number of dependents it’s a must to help, or whether or not you’ve been consuming clear and exercising repeatedly.

Studying from the expertise of buddies round me, I quickly realized that those with the precise CI safety plans had a a lot simpler path to restoration since they didn’t have to fret in regards to the monetary stress. However for those who did not get their CI safety in time, they needed to bear the prices – and as such, stopping work was now not an possibility.

Background

Previously, settling one’s essential sickness insurance coverage was a a lot easier affair – we solely needed to determine whether or not we wished the protection to be tagged to our complete life plan or as a standalone CI time period coverage. However as medical diagnostics superior and allowed for extra essential sicknesses to be recognized at an earlier stage – along with a better survival charge – it modified the insurance coverage scene as effectively.

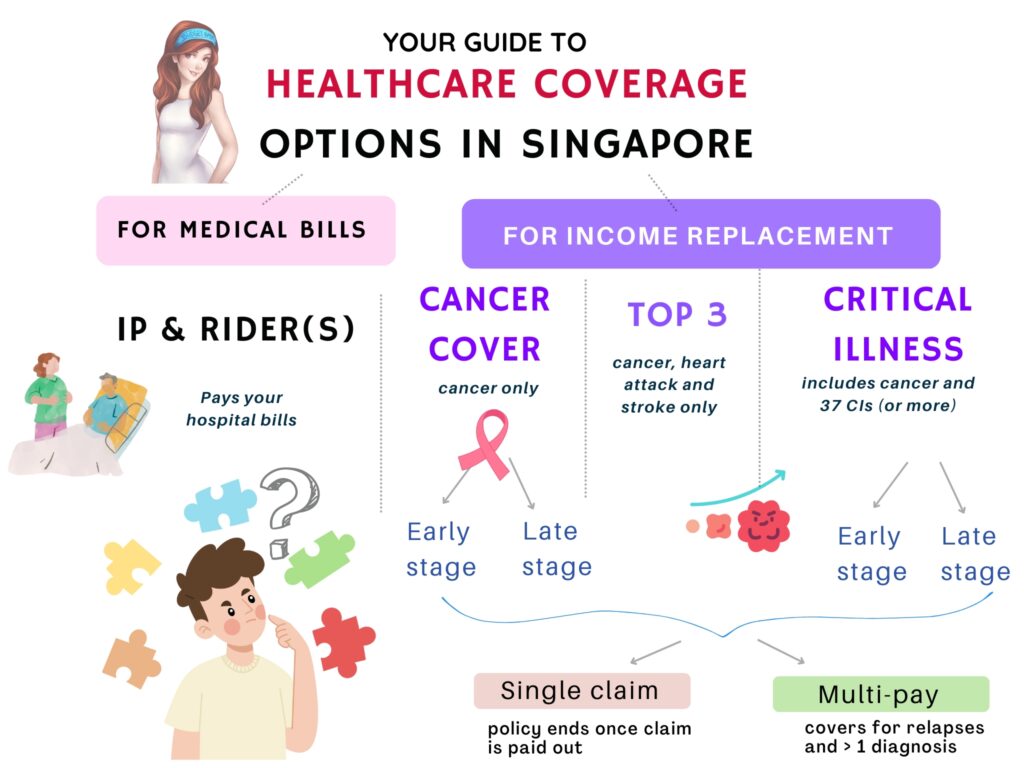

Shoppers can now select from the next choices in relation to getting essential sickness protection:

The issue is, with too many decisions, many individuals additionally find yourself not figuring out which to choose.

For those who’re feeling misplaced by now, don’t fear – you’re not the one one.

The several types of CI protection as we speak

To simplify issues, I’ve summarised the varied kinds of CI insurance coverage available in the market as we speak:

The price of healthcare medical remedies for essential sicknesses might get coated by your Built-in Protect Plan (IP) (together with MediShield Life) and riders that assist cut back the money quantity you have to pay.

Relying on the severity of your situation, most individuals both take day without work work to recuperate, or they depart the job / retrenched because of lengthy intervals of absence. The issue is, our mortgage and different payments (e.g. residing bills to your aged mother and father, youngsters college charges, and so on) nonetheless should be paid for even in the event you get hospitalised! Even in the event you had been to cease your job quickly and redirect your bodily vitality in direction of a faster restoration, you continue to want a supply of revenue to pay for the non-medical payments. Your Built-in Protect Plan (IP) and riders won’t cowl that.

That’s the place insurance coverage insurance policies that present lump sum money payouts can come in useful.

Within the occasion of a essential sickness declare, you should utilize the payouts out of your essential sickness insurance coverage, high 3 CI plan, or your complete CI coverage to assist pay for these different non-medical payments, in addition to any outpatient therapy medical prices (which might be ineligible for claims underneath your Built-in Protect plan).

And in contrast to your IP coverage (you'll be able to solely maintain and declare from 1 Built-in Protect plan), you'll be able to declare from all your CI insurance policies upon the prognosis of CI.

Simply observe that that is topic to the general declare limits and the CI definition in your coverage contract. Phrases and situations apply, the place relevant.

Tips on how to decide the precise CI plan?

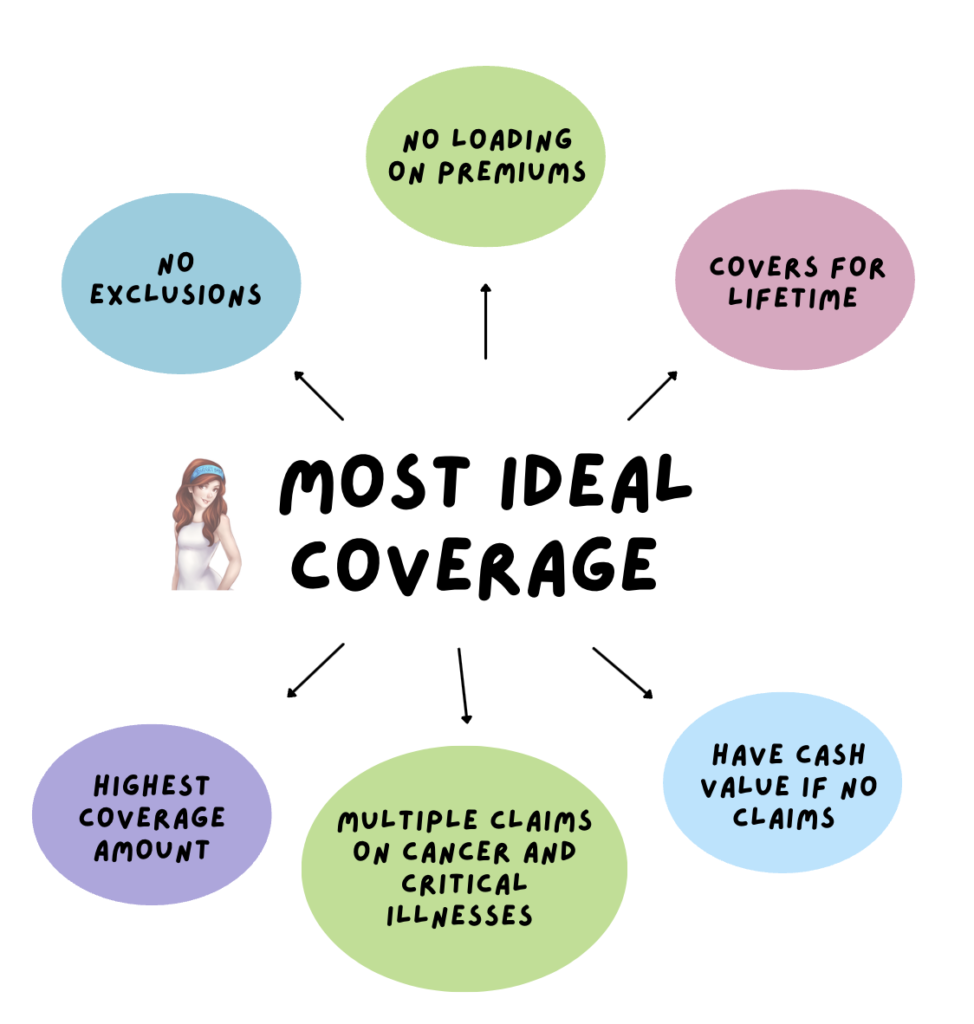

Essentially the most excellent essential sickness insurance coverage, in my opinion, could be one with the next options:

- No exclusions – all situations (together with pre-existing) are coated.

- No must pay larger premiums even if in case you have a pre-existing situation (idealistic, however not all the time possible within the fashionable world)

- Lifetime protection – up until age 100, or till we die.

- Have money worth if no claims are made – some people choose a plan with money worth similar to a life plan as a result of they don’t like the concept that they “paid for nothing” after they made no claims.

- A number of claims allowed – to cowl for relapses, or another subsequent prognosis

- Highest protection quantity to cowl even any sudden future wants

Sadly, we reside within the actual world the place cash is an actual consideration, if not the most essential issue that determines what and the way a lot protection we are able to get.

“As such, you have to handle your expectations collectively together with your price range.”

Funds Babe

Whilst you by no means wish to be ready the place your value of insurance coverage is so excessive that it hinders your high quality of life in different areas, you additionally wish to keep away from being in a scenario the place you’re under-covered financially and unable to pay to your healthcare payments.

Tip 1: If price range is your largest limiting issue, go for a time period plan quite than an entire life coverage.

A complete life plan with essential sickness protection prices considerably extra upfront to safe your protection for all times, particularly if the plan typically gives money worth or premiums refunds sooner or later.

Time period plans, however, are payable yearly to keep up your protection, however usually don’t provide any money worth on the finish of the coverage time period.

The fee distinction is often 4-digit (complete life) vs. 3-digit (time period) in premiums, which after all additionally varies and depends upon your age, gender and life-style i.e. smoker or non-smoker.

Tip 2: Get a complete CI coverage earlier than your well being adjustments.

Ideally, you’d wish to safe your monetary safety towards as many essential sickness situations while you’re nonetheless wholesome and eligible for protection. A very good foundational plan to cowl your bases first would thus be a complete CI coverage which:

- covers you for 37 CIs (or extra),

- pays out even at early-stage prognosis of some sicknesses, and

- comes with the choice for a number of claims (within the occasion of relapse or future CIs).

For instance, a plan like GREAT Essential Cowl: Full with Shield Me Once more rider ticks all of those above standards proper now. With a 100% lump-sum payout upon the prognosis of CI at any stage(s) for every declare, and as much as 3 claims, it covers 53 totally different CIs – greater than the same old 37.

However what in the event you can’t afford a complete CI plan?

Tip 3: Cheaper choices exist for masking the highest 3 CI solely.

Fortunately, you now have an possibility for getting protection for the highest 3 CIs as effectively. These didn’t exist a decade in the past once I was a fresh-faced working grownup shopping for insurance coverage!

Whereas masking for less than 3 essential sickness varieties might not sound excellent, the very fact is that 90% of CI claims are for these situations.

So, if you wish to insure your self towards the situations with statistically highest odds, then think about a plan that covers for not less than most cancers. Even higher could be a plan that covers for most cancers, coronary heart assault and stroke.

Such plans can be utilized for fundamental safety or supplementary protection, particularly in the event you really feel your present protection ranges are inadequate to manage towards the rising prices of continual sickness and residing bills. In that case, you’ll be able to think about having essential sickness/most cancers insurance coverage to assist plug the hole.

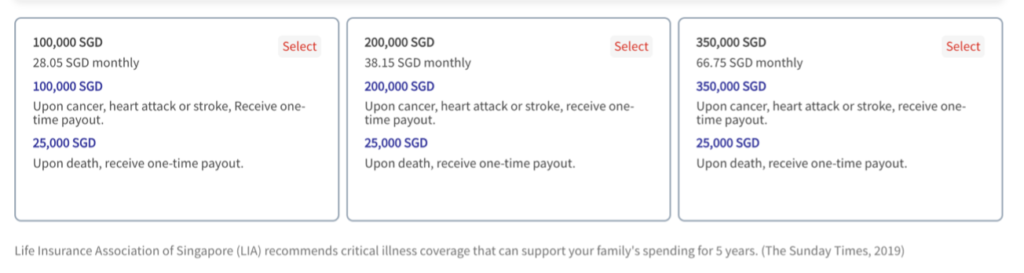

For those who’re fearful in regards to the prices of most cancers, take a look at GREAT Most cancers Guard which might defend you – as much as age 85 – throughout all phases of most cancers. The perfect half? Your premiums don't change with age^, so that you don’t have to fret about paying extra to keep up your protection as you grow old. P.S. GREAT Most cancers Guard comes with 5 kinds of plans so that you can select your protection quantity until age 85 (subsequent birthday).

Tip 4: How a lot protection quantity ought to I get?

“With rising medical prices and price of residing, we are able to solely make best-guess estimates for what we expect we’ll want sooner or later.”

Funds Babe

Proper now, most plans assist you to select from as little as S$50k. LIA recommends for essential sickness safety of ~4 instances of 1’s annual revenue, however after all, some sufferers could possibly recuperate quicker and resume work earlier. In the end, how lengthy it takes may also rely in your bodily well being, how effectively your physique responds to the medication and coverings, in addition to the severity of your medical situation.

If 4X of your annual revenue interprets into hefty insurance coverage premiums that you simply can’t pay for, then let your affordability decide which stage to go for.

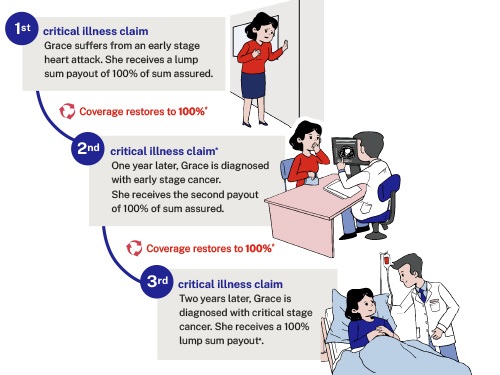

Tip 5: Take into account in the event you want a multi-claim coverage.

After I requested my buddies who survived most cancers on what their largest worry was, most of them mentioned they had been fearful a few relapse and never having sufficient cash for it. Keep in mind, multi-claim insurance policies didn’t exist as an possibility previous to the interval earlier than the 2010s.

What’s extra, new knowledge has emerged to point out some most cancers varieties have a better recurrence charge e.g. ovarian most cancers recurs in 85% of sufferers, whereas half of these with bladder most cancers develop recurrence after cystectomy.

After seeing a number of of my buddies undergo from a relapse, I’m beginning to see the enchantment of getting a multi-claim / multi-pay coverage. Nonetheless, multi-claim plans naturally value greater than their single-claim counterparts, so it’s a must to issue this into your price range.

For instance, plans like GREAT Essential Cowl Sequence provide the choice so as to add a Shield Me Once more rider, which then insures you towards recurrence threat (of being recognized with one other essential sickness) so that you simply stay insured even after a prognosis, for as much as two essential sickness episodes after your first declare.

Conclusion

As you’ll be able to see, getting coated for essential sickness is now not a easy affair. With all of the several types of choices accessible as we speak, it may grow to be fairly perplexing to decide on.

Nonetheless, one factor stays the identical: the extra complete your protection, the extra you’ll have to pay for insurance coverage premiums.

Which is why the finest insurance coverage coverage for you and your loved ones is the one that you would be able to afford and covers your wants accordingly.

To determine this out, you should utilize the guiding questions under that can assist you:

- What are the several types of CI protection I can select from as we speak?

- What are my monetary duties?

- How a lot price range do I’ve?

- Can I afford to pay for a complete essential sickness coverage which covers not less than 37 (or extra) essential sicknesses?

- If not, can I not less than afford to insure myself towards the statistically highest odds of most cancers, coronary heart assault and stroke?

- And even simply most cancers alone?

If you have already got current CI protection, then you’ll be able to ask your self these questions as a substitute:

- How a lot CI protection do I presently have?

- Does my (older) insurance coverage plan cowl me towards early-stage CI claims, or is it restricted to late-stage claims solely?

- Do I would like so as to add on a multi-claim coverage?

- Are there any safety gaps in my portfolio now the place standalone most cancers or high 3 CI plans would possibly have the ability to fill?

Getting your self protected towards the prices of essential sickness doesn’t all the time need to be costly.

Try Nice Japanese’s vary of plans, together with standalone plans for CI and most cancers:

| Essential sickness | Most cancers safety | ||

| GREAT Essential Cowl: Full | GREAT Essential Cowl: High 3 CIs | GREAT Most cancers Guard | |

| Variety of CIs coated | 53 | 3 (most cancers, coronary heart assault, stroke) | 1 (most cancers) |

| Sort of protection | All phases | All phases | All phases |

| Sum Assured | 50K – 350K | 50K – 350K | 50K – 300K |

| Payout | 100% lump sum | 100% lump sum | 100% lump sum |

| Variety of claims allowed? | As much as 3 instances, 100% lump sum per declare (with Shield Me Once more rider) | As much as 3 instances, 100% lump sum per declare (with Shield Me Once more rider) | 1 time, 100% payout |

| Demise profit | 25K | 25K | Nil |

| Entry Age (Age Subsequent Birthday) | 1 – 60 for Coverage Time period as much as age 85; 1 – 55 for Coverage Time period as much as age 65; | 1 – 60 | 17 – 55 |

| Coverage time period (as much as, Age Subsequent Birthday) | 65 or 85 | 85 | 85 |

| Premium construction | Doesn’t improve with age^ (stage) | Yearly improve | Doesn’t improve with age^ (stage) |

| Underwriting wanted? | Full underwriting | 3 Well being Questions | 3 Well being Questions |

| The place to purchase? | By way of Nice Japanese Monetary Representatives solely | On-line or through Nice Japanese & OCBC Monetary Representatives | On-line or through Nice Japanese & OCBC Monetary Representatives |

Additionally they have some present promotions which you should utilize that can assist you save extra in your value of insurance coverage:

Disclosure: This publish is a sponsored collaboration with The Nice Japanese Life Assurance Firm Restricted ("Nice Japanese"). All opinions are that of my very own, and knowledge correct as of March 2024.

^For GREAT Essential Cowl: Full and GREAT Most cancers Guard: The premium quantity is decided on the age of entry and doesn't improve together with your age. For GREAT Most cancers Guard, the premiums are inclusive of and topic to prevailing GST. Premium charges of GREAT Essential Cowl: Full, GREAT Essential Cowl: High 3 CIs and GREAT Most cancers Guard aren't assured and could also be adjusted primarily based on future expertise of the plan. Adjusted charges, if any, will probably be suggested previous to coverage renewals. As these merchandise don't have any financial savings or funding characteristic, there isn't a money worth if the coverage ends or is terminated prematurely. That is solely product data offered by Nice Japanese. The data introduced is for common data solely and doesn't have regard to the precise funding goals, monetary scenario or specific wants of any specific particular person. You could want to search recommendation from a professional adviser earlier than shopping for the product. For those who select to not search recommendation from a professional adviser, you need to think about whether or not the product is appropriate for you. Shopping for medical health insurance merchandise that aren't appropriate for it's possible you'll impression your means to finance your future healthcare wants. For those who determine that the coverage isn't appropriate after buying the coverage, it's possible you'll terminate the coverage in accordance with the free-look provision, if any, and the insurer might recuperate from you any expense incurred by the insurer in underwriting the coverage. Protected as much as specified limits by SDIC. This commercial has not been reviewed by the Financial Authority of Singapore. Data right as at 6 March 2024.

[ad_2]