{kind=link}

[ad_1]

Two payments proposed in Illinois this yr illustrate but once more the necessity for lawmakers to higher perceive how insurance coverage works. Illinois HB 4767 and HB 4611 – like their 2023 predecessor, HB 2203 – would hurt the very policyholders the measures intention to assist by driving up the fee for insurers to jot down private auto protection within the state.

“These payments, whereas meant to deal with rising insurance coverage prices, would have the alternative influence and certain hurt customers by lowering competitors and rising prices for Illinois drivers,” stated a press launch issued by the American Property Casualty Insurance coverage Affiliation, the Illinois Insurance coverage Affiliation, and the Nationwide Affiliation of Mutual Insurance coverage Firms. “Insurance coverage charges are at the beginning a perform of claims and their prices. Moderately than working to assist make roadways safer and cut back prices, these payments search to vary the state’s insurance coverage ranking legislation and prohibit the usage of elements which are extremely predictive of the danger of a future loss.”

The proposed legal guidelines would bar insurers from contemplating nondriving elements which are demonstrably predictive of claims when setting premium charges.

“Prohibiting extremely correct ranking elements…disconnects worth from the danger of future loss, which essentially means high-risk drivers pays much less and lower-risk drivers pays greater than they in any other case would pay,” the discharge says. “Moreover, altering the ranking legislation and elements used is not going to change the economics or crash statistics which are the first drivers of the price of insurance coverage within the state.”

Triple-I agrees with the important thing issues raised by the opposite commerce organizations. As we now have written beforehand, such laws suggests a lack of expertise about risk-based pricing that’s not remoted to Illinois legislators – certainly, comparable proposals are submitted once in a while at state and federal ranges.

What’s risk-based pricing?

Merely put, risk-based pricing means providing totally different costs for a similar degree of protection, primarily based on danger elements particular to the insured individual or property. If insurance policies weren’t priced this fashion – if insurers needed to give you a one-size-fits-all worth for auto protection that didn’t take into account car sort and use, the place and the way a lot the automobile shall be pushed, and so forth – lower-risk drivers would subsidize riskier ones. Threat-based pricing permits insurers to supply the bottom doable premiums to policyholders with probably the most favorable danger elements. Charging greater premiums to insure higher-risk policyholders allows insurers to underwrite a wider vary of coverages, thus bettering each availability and affordability of insurance coverage.

This easy idea turns into sophisticated when actuarially sound ranking elements intersect with different attributes in methods that may be perceived as unfairly discriminatory. For instance, issues have been raised about the usage of credit-based insurance coverage scores, geography, dwelling possession, and motorcar data in setting dwelling and automobile insurance coverage premium charges. Critics say this will result in “proxy discrimination,” with folks of coloration in city neighborhoods generally charged greater than their suburban neighbors for a similar protection.

The confusion is comprehensible, given the complicated fashions used to evaluate and worth danger and the socioeconomic dynamics concerned. To navigate this complexity, insurers rent groups of actuaries and information scientists to quantify and differentiate amongst a spread of danger variables whereas avoiding unfair discrimination.

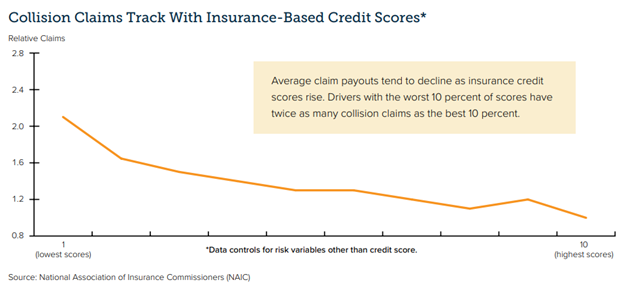

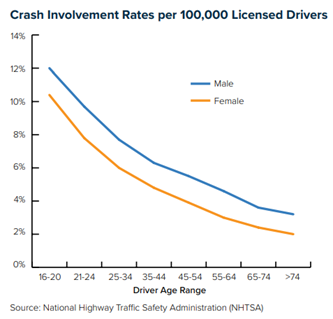

Whereas it might be onerous for policyholders to imagine elements like age, gender, and credit score rating have something to do with their chance of submitting claims, the charts under show clear correlations.

Policyholders have cheap issues about rising premium charges. It’s essential for them and their legislators to know that the present high-rate atmosphere has nothing to do with the applying of actuarially sound ranking elements and every part to do with rising insurer losses related to greater frequency and severity of claims. Frequency and claims traits are pushed by a variety of causes – corresponding to riskier driving habits and authorized system abuse – that warrant the eye of policymakers. Legislators would do properly to discover methods to scale back dangers, comprise fraud different types of authorized system abuse, and enhance resilience, slightly than pursuing “options” to limit pricing that may solely make these drawback worse.

Study Extra

New Triple-I Points Transient Takes a Deep Dive into Authorized System Abuse

How Proposition 103 Worsens Threat Disaster in California

Louisiana Nonetheless Least Inexpensive State for Private Auto, Householders Insurance coverage

IRC Outlines Florida’s Auto Insurance coverage Affordability Issues

Colorado’s Life Insurance coverage Knowledge Guidelines Provide Glimpse of Future for P&C Writers

It’s Not an “Insurance coverage Disaster” – It’s a Threat Disaster

Indiana Joins March Towards Disclosure of Third-Social gathering Litigation Funding Offers

Litigation Funding Legislation Discovered Missing in Transparency Division

[ad_2]