{kind=link}

[ad_1]

Editor’s notice: Since this put up was first printed, percentages cited within the first paragraph have been corrected. (February 7, 1pm)

Following our put up on racial and ethnic wealth gaps, right here we flip to the distribution of wealth throughout age teams, specializing in how the image has modified for the reason that starting of the pandemic. As of 2019, people below 40 years outdated held simply 4.9 % of complete U.S. wealth regardless of comprising 37 % of the grownup inhabitants. Conversely, people over age 54 made up an analogous share of the inhabitants and held 71.6 % of complete wealth. Since 2019, we discover a slight narrowing of those wealth disparities throughout age teams, probably pushed by expanded possession of monetary belongings amongst youthful People.

Knowledge

We use the quarterly Distributional Monetary Accounts printed by the Board of Governors of the Federal Reserve System. These information mix sectoral stability sheets from the Fed’s Monetary Accounts and individual-level information from the Survey of Client Funds to estimate wealth holdings by wealth part and demographic group. We look at wealth dynamics from 2019:Q1 by 2023:Q3 for 3 age teams: 18-39, 40-54, and 55 and over. To calculate actual wealth development, we deflate age group wealth ranges in every quarter by the age group-specific worth indices developed within the Equitable Progress Indicators collection.

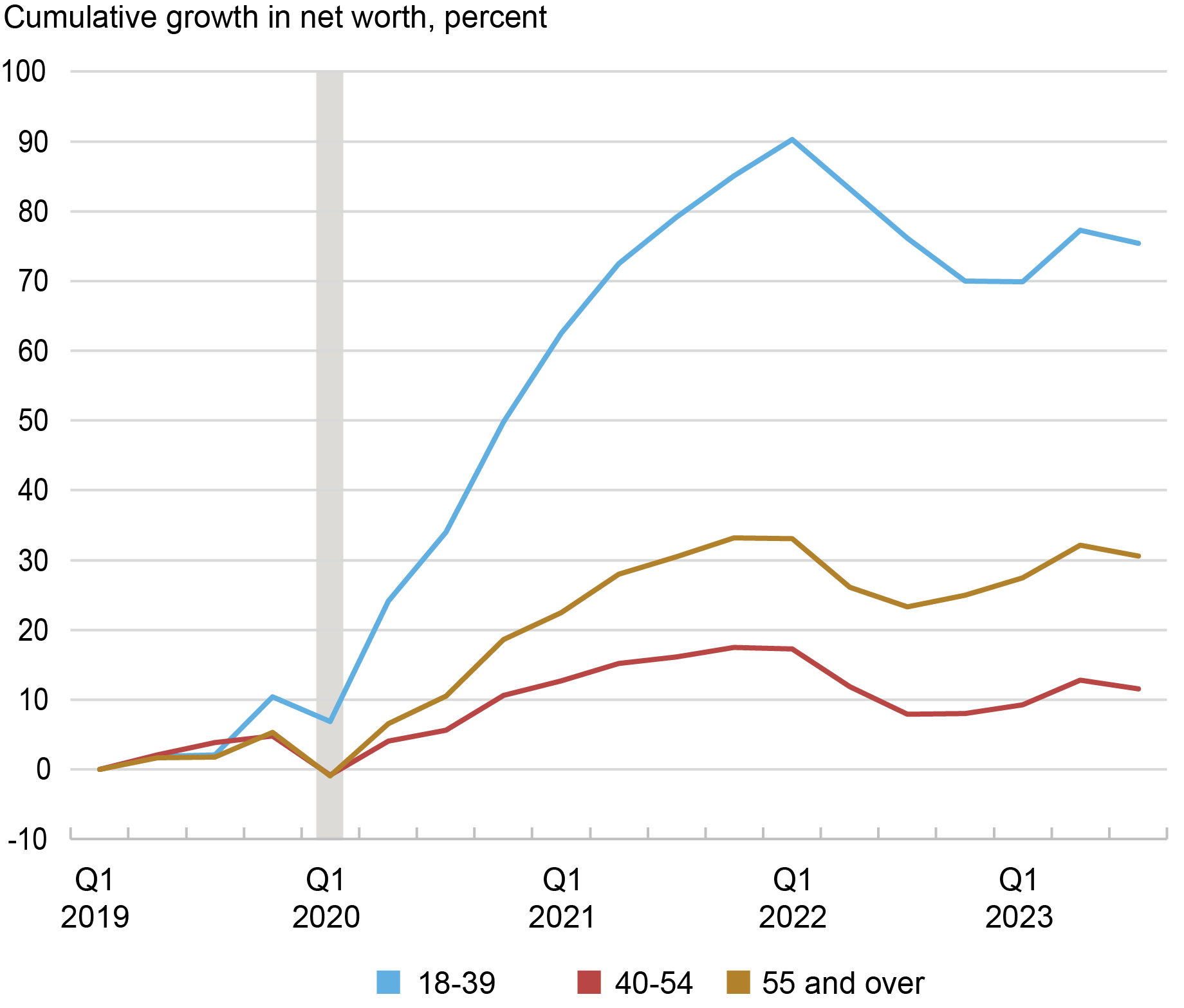

Actual wealth has elevated for all three age teams since 2019, however the change has been most dramatic for youthful adults (see chart under). For people 39 and youthful, wealth elevated by 80 %. In distinction, it grew by solely 10 % for these aged 40-54 and by 30 % for these 55 and over.

Youthful Adults Far Outpace Different Teams in Wealth Progress for the reason that Pandemic

Notice: Calculations are based mostly on actual (inflation-adjusted) costs.

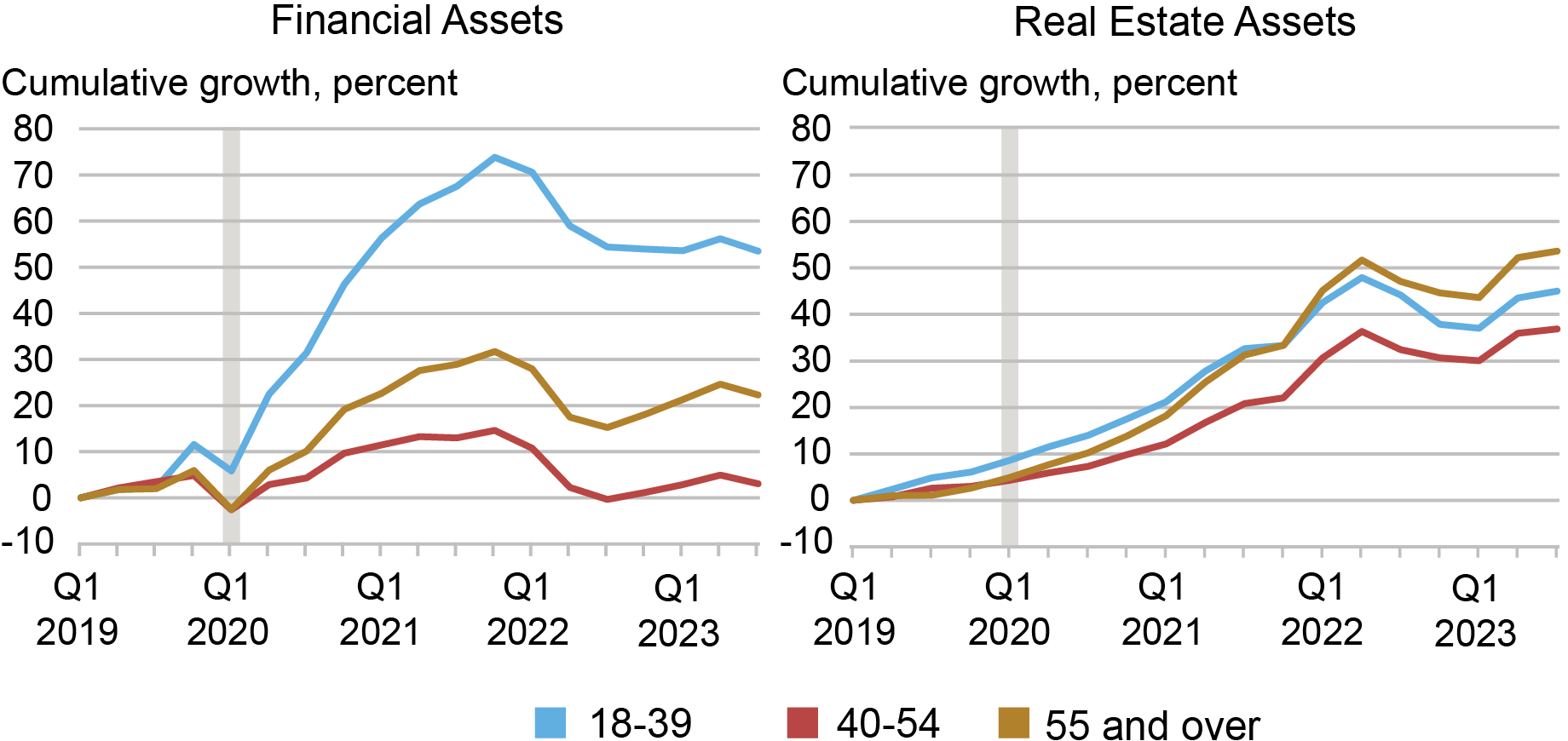

What accounts for the dispersion in wealth development over this era? There may be little or no dispersion in development of liabilities. The expansion price of liabilities amongst 40–54-year-olds was solely about 5 proportion factors larger than these of the opposite age teams. Actual property belongings, which elevated by about 40 % throughout teams on account of rising residence costs, contribute to however don’t totally account for the dispersion in wealth development (proper panel of the chart under).

Monetary belongings contributed most to the differential development in wealth over this time (left panel under). Monetary asset costs rose by a lot of the COVID interval. These below 40 noticed a higher than 50 % improve in the true worth of their monetary belongings between 2019 and 2023. Those that have been 40-54 noticed solely a 3 % improve, whereas these over 54 noticed a few 20 % improve.

Monetary Belongings Develop Most Quickly for Youthful Adults whereas Actual Property Progress Is Comparatively Even

Notice: Calculations are based mostly on actual (inflation-adjusted) costs.

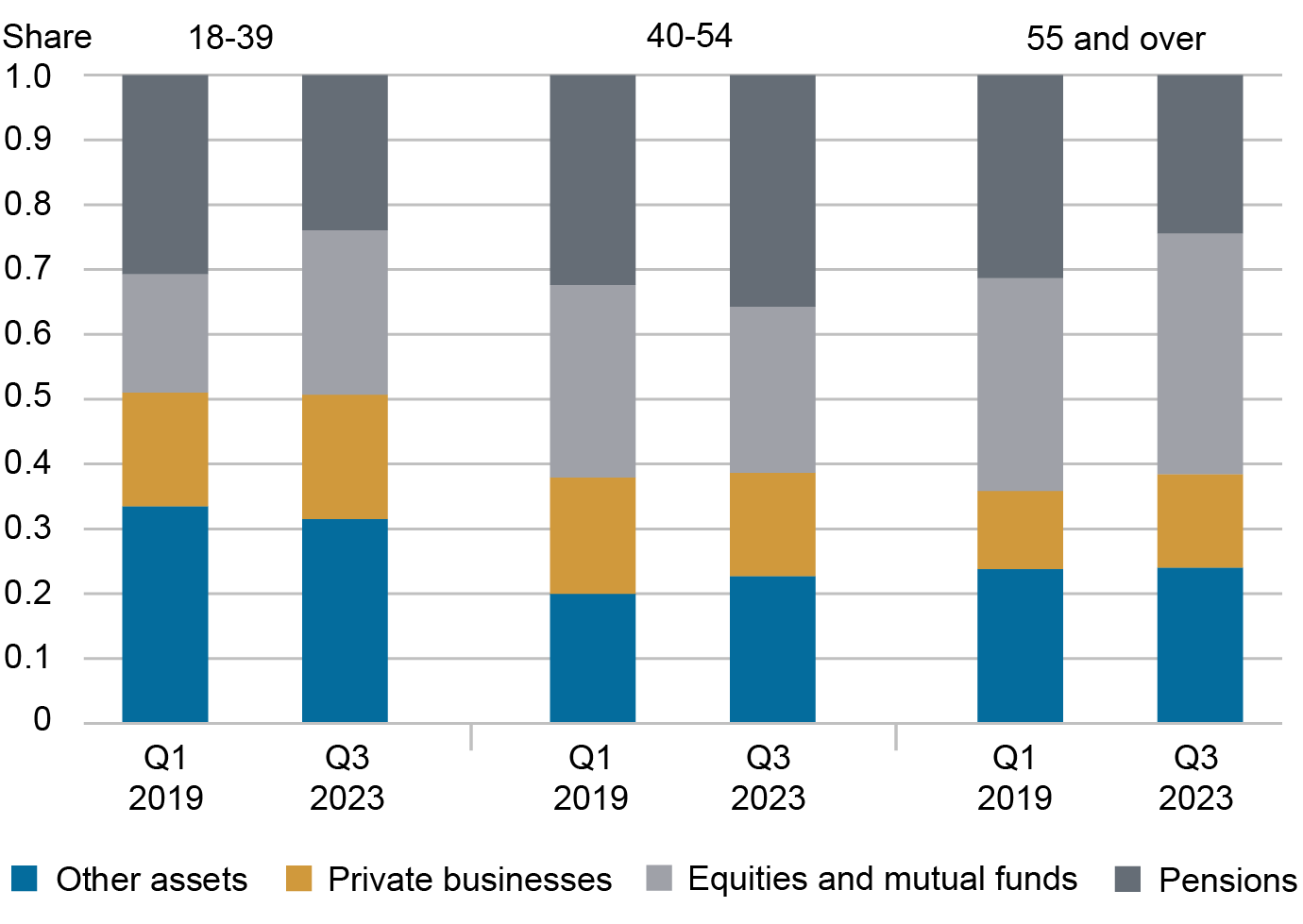

Monetary Asset Composition

To know this dispersion in wealth, we take into account which monetary belongings every age group held. In 2019, all age teams held 31-32 % of their monetary belongings as pensions (determine under). The 2 youthful age teams held about 18 % of their wealth in enterprise belongings, in comparison with 12 % amongst these over 54. The bigger variations are within the share held in company equities and mutual funds. These below age 40 held 18 % of their wealth in equities and funds, in comparison with 30 and 33 % for the 2 older age teams.

Youthful Adults Posted Best Portfolio Shift towards Equities and Mutual Funds

By 2023:Q3, company equities and mutual funds made up 37 % of the monetary belongings held by these over 55, up from 33 % in 2019:Q1. For people below 40, in the meantime, this share rose to 25 %, in comparison with 18 % in 2019:Q1. Thus, the over-55 group noticed their fairness/mutual fund portfolio share improve by 12 % and the under-40 group’s fairness share went up by a whopping 39 %. Accordingly, the share held in pensions shrunk for each of those age teams. In distinction, 40–55-year-olds noticed their fairness/mutual fund portfolio share lower from 30 to 25 %, with their pension holdings climbing from 32 % to 36 %.

The under-40 group skilled a a lot higher improve in fairness portfolio share than the older teams did; this elevated publicity to equities—the fastest-growing monetary asset class in the course of the interval—enabled youthful adults to file larger development in each monetary belongings and general wealth. This shift in portfolio composition towards equities probably displays the truth that youthful adults, being farther away from retirement, can afford to put money into dangerous belongings at a better price than older adults. The youngest age group can be the poorest and thus acquired a lot of the COVID-era fiscal stimulus, granting them extra financial savings to put money into equities. (It’s price noting right here that our information don’t enable us to separate adjustments in investments from adjustments in returns; the outcomes we determine are a mixture of each elements.)

Conclusion

The pandemic and subsequent adjustments available in the market have had differing results on web price throughout age teams. Analyzing shifts within the distribution of wealth since 2019, we discover that quicker wealth development amongst youthful adults has led to a restricted narrowing of age-based wealth disparities over the previous 4 years. This was largely as a consequence of adjustments in holdings of monetary belongings throughout the three age teams, with the under-40 group shifting towards equities on the highest price amid rising fairness costs. We are going to proceed to watch adjustments within the wealth distribution because the coverage and financial surroundings evolves.

Chart information ![]()

Web Price by Race and Age information ![]()

Pension information ![]()

Equities and Mutual Funds by Age information ![]()

Rajashri Chakrabarti is the pinnacle of Equitable Progress Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Natalia Emanuel is a analysis economist in Equitable Progress Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Ben Lahey is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Easy methods to cite this put up:

Rajashri Chakrabarti, Natalia Emanuel, and Ben Lahey, “Wealth Inequality by Age within the Publish‑Pandemic Period,” Federal Reserve Financial institution of New York Liberty Road Economics, February 7, 2024, https://libertystreeteconomics.newyorkfed.org/2024/02/wealth-inequality-by-age-in-the-post-pandemic-era/.

Disclaimer

The views expressed on this put up are these of the creator(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the creator(s).

[ad_2]