{kind=link}

[ad_1]

A earlier publish explored the potential implications for U.S. progress and inflation of a manufacturing-led increase in China. This publish considers spillovers to the U.S. from a draw back state of affairs, one during which China’s ongoing property sector hunch takes one other leg down and precipitates an financial arduous touchdown and monetary disaster.

China’s Coverage House Is Changing into Extra Constrained

On this state of affairs, Chinese language authorities’ coverage house proves inadequate to forestall a deep and protracted downturn. Our view is that this state of affairs is much less more likely to materialize than the upside state of affairs described in our earlier publish. We share the consensus view that the Chinese language authorities retain appreciable scope for managing the financial system and related monetary dangers.

In earlier work, we examined the Chinese language authorities’ coverage house and its potential limits. To recap, China’s coverage instruments draw added energy from distinctive options of the nation’s political and monetary system. China’s authorities maintains direct and oblique management of the nation’s monetary and nonfinancial sectors. Furthermore, the home financial system is shielded from exterior shocks by the nation’s present account surplus, giant inventory of international trade reserves, and system of capital controls. Total, the authorities possess appreciable scope for utilizing financial, credit score, and central authorities fiscal insurance policies to dampen financial fluctuations.

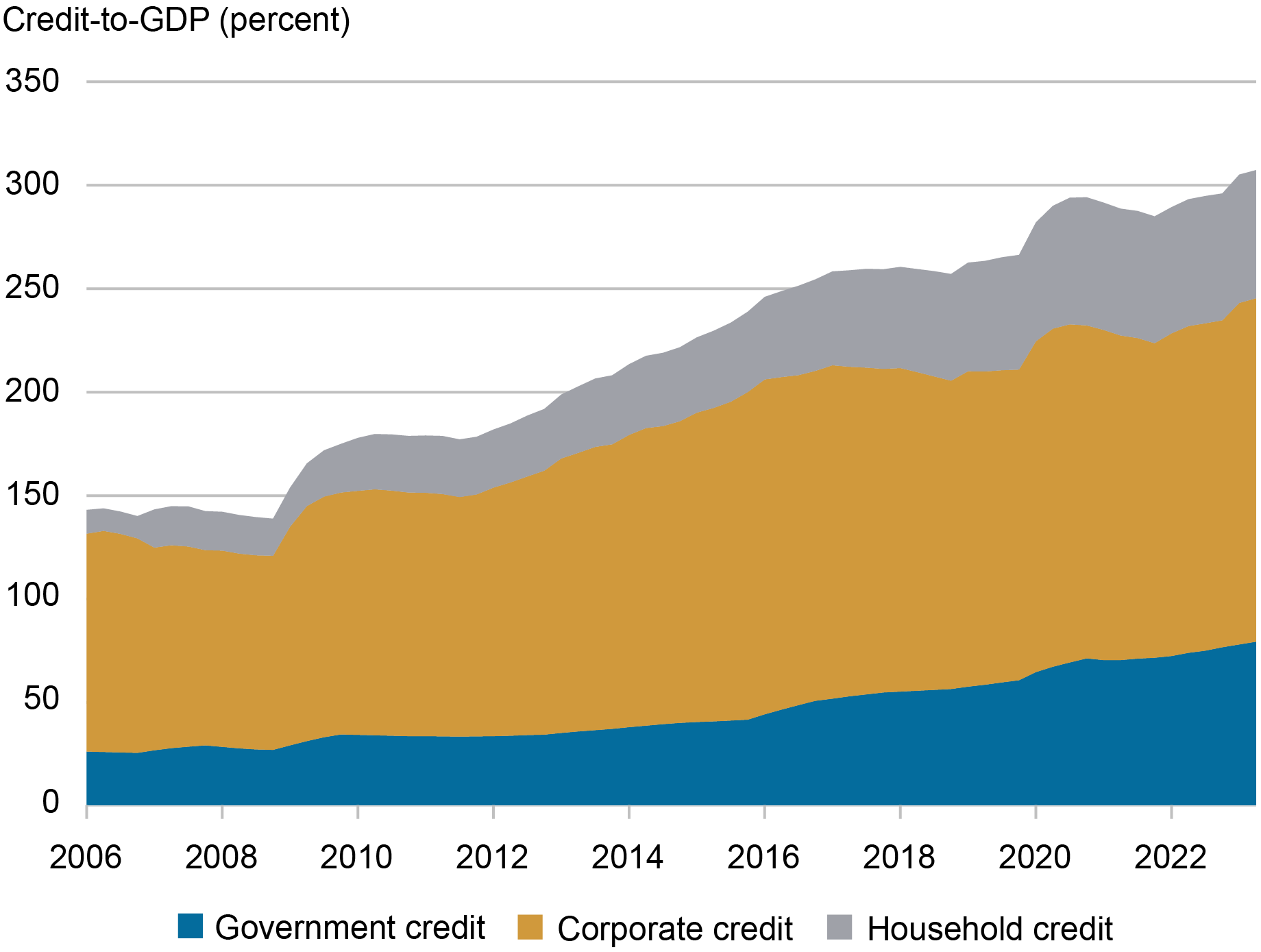

Nevertheless, coverage house is rising extra constrained as debt continues to construct. The ratio of nonfinancial sector debt to GDP surged once more in 2023 and now tops 300 p.c (chart under). Worldwide expertise means that fast debt accumulation is commonly a harbinger of monetary crises or prolonged intervals of sluggish financial progress. This conclusion can also be backed by educational analysis, and explored elsewhere on Liberty Avenue Economics.

China’s Debt Ranges Proceed to Climb

The Potential for One other Leg Down within the Property Sector

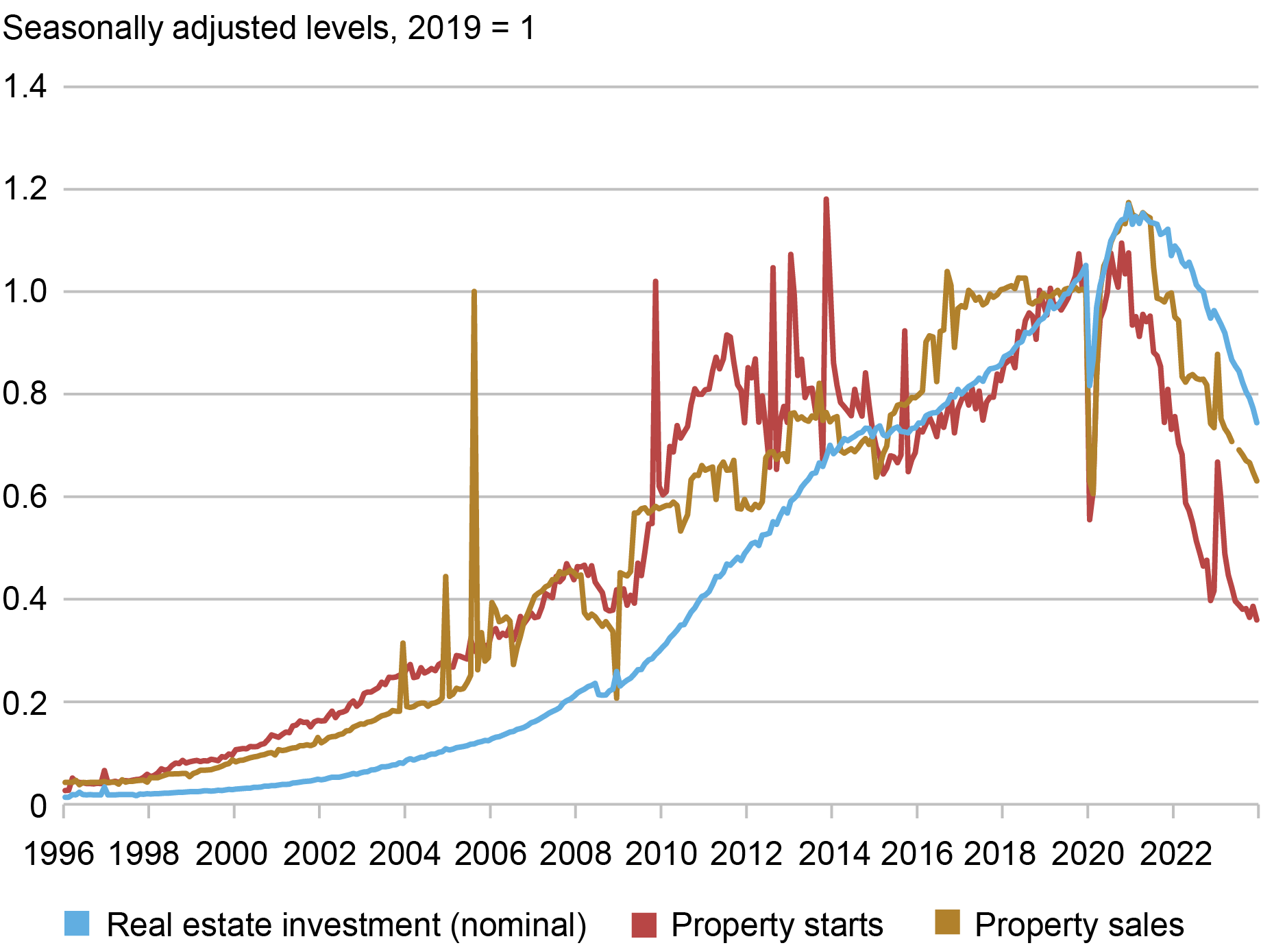

The important thing driver for our draw back state of affairs can be additional stress within the property sector. Since late 2020, new property begins and gross sales have fallen by two-thirds and one-third, respectively (chart under). Lending to builders got here to a virtually full halt by means of the tip of 2022 earlier than modest internet lending resumed when authorities coverage on property sector lending was eased. However complete lively building initiatives have fallen a a lot smaller 13 p.c since peaking in 2021, with stronger state-owned or supported builders persevering with work on uncompleted initiatives. Development exercise might fall additional if stronger builders start to face elevated monetary stress.

Additional stress within the property sector would amplify ongoing fiscal tightening on the native degree. On this case, distinctive options of China’s political and financial system would work in opposition to it. Native governments have historically derived a big portion of their revenues from land gross sales, a supply that dries up in a falling worth atmosphere. In flip, these fiscal pressures would undermine native governments’ potential to assist builders and different native corporations, together with native manufacturing champions.

Might Property Sector Exercise Fall Additional?

Notice: Figures are calculated from official printed ranges.

The important thing position of the property sector within the Chinese language financial system makes troubles there a believable set off for an financial arduous touchdown and monetary disaster. Property-related exercise accounted for roughly one-quarter of Chinese language GDP earlier than the current hunch and nonetheless represents an outsized share of exercise by worldwide requirements. Property-related credit score continues to account for roughly one-quarter of complete debt excellent. And property accounts for roughly two-thirds of family property. Given this backdrop, it’s no shock that the property hunch has coincided with a extreme erosion in family and enterprise confidence.

A Draw back State of affairs for China and Its Implications for the U.S.

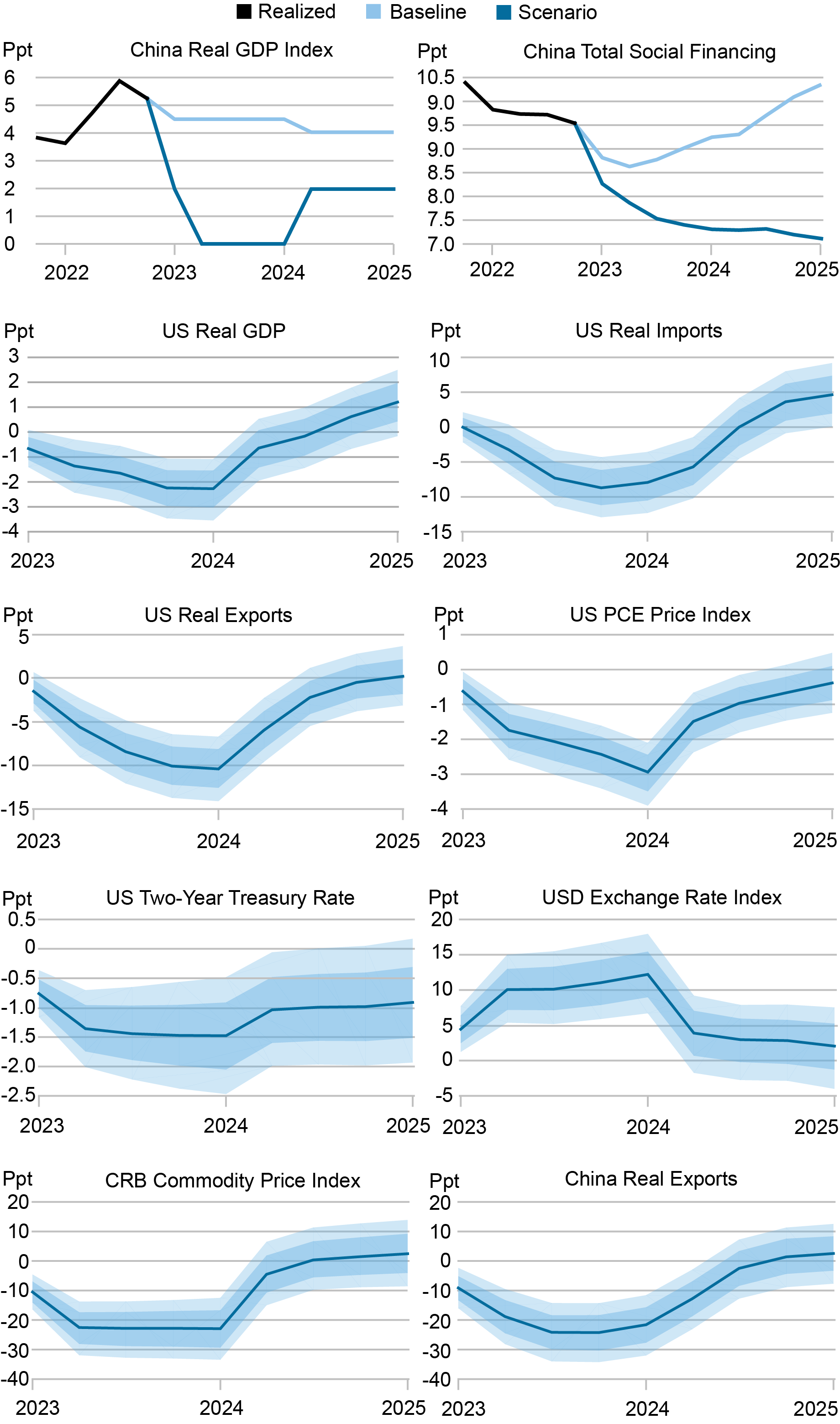

Below our property crash state of affairs, GDP progress in China falls to zero in 2024. That is adopted by a tepid restoration to about 2 p.c over the subsequent yr. This degree represents dramatic underperformance relative to the Worldwide Financial fund (IMF) baseline, which requires progress of 4.6 p.c in 2024 and 4.0 p.c the next yr. Credit score progress (complete social financing) additionally falls under the IMF baseline, albeit much less dramatically.

To quantify the affect of this draw back state of affairs on the U.S. financial system, we depend on the Bayesian VAR mannequin launched in our earlier publish. This mannequin is designed to seize the historic joint dynamics of the U.S. and Chinese language economies. We use the estimated mannequin relationships to assemble counterfactual paths for U.S. macroeconomic aggregates whereas constraining Chinese language output and credit score progress to observe the paths in our crash state of affairs. As in our earlier train, we measure state of affairs impacts in opposition to a baseline during which the Chinese language financial system evolves in line with the IMF projections.

The highest two panels within the chart under present the conduct of GDP and credit score progress—our key conditioning variables—below the crash and baseline eventualities, reported as year-over-year p.c modifications. As already famous, the crash state of affairs includes dramatic GDP-growth underperformance relative to the baseline. The remaining panels present the implications of the crash state of affairs for U.S. and chosen Chinese language and international macro variables, measured as proportion deviations from the baseline, with the blue shading exhibiting estimated confidence intervals.

This train exhibits {that a} Chinese language arduous touchdown might end in materially weaker U.S. progress and commerce efficiency and decrease U.S. inflation, with the most important impacts occurring over the primary 4 quarters following a crash. Actual GDP progress falls as a lot as 2 proportion factors (ppt) under baseline earlier than starting to get better, whereas export volumes fall as a lot as 10 ppt under baseline. The PCE worth index, for its half, falls some 3 ppt under baseline earlier than disaster impacts start to fade.

Projected Path for Key Macro Variables in a Exhausting Touchdown State of affairs

The magnitude of those impacts is bigger than in our earlier publish premised on a manufacturing-led increase in China, according to the bigger deviation of GDP progress from baseline. The underlying mechanisms are nevertheless the identical, albeit now working in the other way.

The sudden plunge in Chinese language home demand progress results in sharp falls in international commodity costs and Chinese language exports. These impacts mirror the important thing position China performs in international commerce and manufacturing networks. Weaker Chinese language demand interprets into weaker demand for China’s worldwide worth chain companions, with this affect amplified by the knock-on tightening of these corporations’ financing constraints. The deterioration in international commerce, in fact, feeds into the same deterioration in U.S. commerce volumes.

The U.S. greenback, in the meantime, sees important appreciation, according to its longstanding unfavorable correlation with international commodity costs. Within the context of our property crash state of affairs, this energy could be understood as reflecting risk-off conduct amongst international traders, who search refuge in U.S. monetary markets and U.S. greenback property. The stronger greenback, in flip, contributes to a tightening in international monetary circumstances. Actually, the primary affect of weaker Chinese language demand on international monetary circumstances is by way of this oblique channel.

Briefly, the materialization the property crash state of affairs in China would tilt the steadiness of dangers for U.S. progress and inflation to the draw back. As we’ve mentioned, nevertheless, the Chinese language authorities seem to have satisfactory instruments to comprise new downward pressures on the nation’s financial system. At current, we regard the materialization of this state of affairs as much less seemingly than the upside manufacturing increase state of affairs.

The 2 eventualities, in fact, would carry totally different coverage implications. A deep Chinese language slowdown would contribute to decrease U.S. and international inflation, seemingly bringing ahead investor expectations for coverage easing. In distinction, materially quicker progress in China may add to the challenges of bringing inflation again to central financial institution targets, seemingly pushing out investor expectations for alleviating.

Ozge Akinci is head of Worldwide Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Hunter L. Clark is a global coverage advisor in Worldwide Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Jeffrey B. Dawson is a global coverage advisor in Worldwide Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Matthew Higgins is an financial analysis advisor in Worldwide Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Silvia Miranda-Agrippino is a analysis economist in Worldwide Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Ethan Nourbash is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Ramya Nallamotu is a senior analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

How you can cite this publish:

Ozge Akinci, Hunter Clark, Jeff Dawson, Matthew Higgins, Silvia Miranda-Agrippino, Ethan Nourbash, and Ramya Nallamotu, “What Occurs to U.S. Exercise and Inflation if China’s Property Sector Results in a Disaster?,” Federal Reserve Financial institution of New York Liberty Avenue Economics, March 26, 2024, https://libertystreeteconomics.newyorkfed.org/2024/03/what-happens-to-u-s-activity-and-inflation-if-chinas-property-sector-leads-to-a-crisis/.

Disclaimer

The views expressed on this publish are these of the creator(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the creator(s).

[ad_2]