[ad_1]

Lambert and I’ve inveighed repeatedly towards utilizing cute advertising and marketing classes (GenX, Millennials, Boomers) in political evaluation. Generational cohorts shouldn’t have company. Please establish a GenX celebration or a Millennial foyer, for starters. However that typology however proved to be very profitable in stoking one more implementation of the Jay Gould saying, “I can rent on half of the working class to kill the opposite half.” And as Gould intimated, the wealthy who had been pulling the strings remained as the true menace to the frequent man.

Nonetheless, the moneyed have efficiently stoked generational hatred as a Malicious program for their very own pursuits. One noteworthy instance was billionaire and Soros fund supervisor Stan Druckenmiller. Within the years shortly after the monetary disaster (there was a interval when unemployment amongst current faculty grads was larger than amongst high-school-only job seekers), he sponsored shows on faculty campuses that offered Boomers (and never different age cohorts) as leaching off the younger. His talks targeted on Social Safety and Medicare, contending that Boomers had been getting an incredible deal and the younger would get nothing like that.

That argument was designed to create that actuality. Social Safety and Medicare are pay as you go packages, regardless of the handy fiction of a belief fund and depicting them as insurance coverage. Even so, “fixing” them, even on that foundation, requires just some tweaks, one of the crucial necessary being elevating the ceiling on incomes topic to payroll taxes. Many economists, notably Dean Baker, have made detailed proposals and confirmed out the maths.

Financiers like Druckenmiller have additionally been selling the Social Safety treatment of privatizing it. Think about how a lot Wall Road would make by getting its greasy mitts on such ginormous property.

Furthermore, contemplate how we wound up the place we’re. The shift to financialization truly began in 1976, when actual wage good points and productiveness good points began diverging. To place it extra colloquially, laborers stopped getting their justifiable share of effectivity enhancements, and that solely acquired progressively worse over time. 1976 was too early for Boomers to have had something to do with that coverage shift; even the oldest Boomers had been barely seasoned sufficient to be establishing themselves as politicians or pundits.

Milton Friedman, born 1912, was singlehandedly the best promoter of neoliberalism and demonizer of presidency intervention and security nets, depicting them each as opposite to “freedom”. Louis Powell, writer of the then excessive proper wing Powell memo, which set forth a long-term, open ended technique to roll again the New Deal and make People extra receptive to business-friendly insurance policies, was born in 1907. Jimmy Carter, the primary trendy US president to undertake deregulatory insurance policies (as an example, of trucking) was born in 1924. Ronald Reagan, who campaigned on the concept authorities was the issue, was born in 1911. Alan Greenspan, who as Fed chair actively promoted a hands-off, financial institution pleasant financial regime, was born in 1926. His common companion in inequality crimes, Bob Rubin, was born in 1941.

Even our strongest pols right this moment, Joe Biden and Nancy Pelosi, will not be Boomers.

Specifically, the shift away from progress and prosperity based mostly on rising wages to based mostly on asset progress and extra client entry to credit score as a cover-up for stagnating actual wages, actually took maintain after Volcker determined he’d had sufficient with elevating rates of interest to the moon to self-discipline labor. The ensuing fall in rates of interest kicked off a really lengthy interval of disinflation, which continued by means of 2007 and set the worth for an extended asset worth increase (admittedly with some hiccups alongside the best way).

Now clearly Boomers of some means benefitted from housing and inventory worth rises. However had been they really higher off than older cohorts, the place not simply many white collar employees but in addition union members, had outlined profit pensions? And attributable to restricted rentierism, notably in housing prices and medical care, these stipends weren’t shabby in buying energy phrases?

That isn’t to say that youthful cohorts haven’t suffered in relative phrases because the neoliberal con of asset worth goosing has began hitting its limits. However the massive winners have been the rich, as revenue and asset concentrations within the prime 1% and 0.1% exploded within the neoliberal period.

Now to the Monetary Occasions sighting, that the younger are lastly realizing who their actual enemies are.

When millennials first emerged, blinking, into the grownup world within the 2010s, they rapidly bonded over shared adversity….

It was a grim decade, however a minimum of they’d one another, and had been united towards a standard foe within the form of the rich, homeowning child boomer era…

because the targets of millennial ire more and more recede from view, they could quickly get replaced by one other privileged, property-owning elite a lot nearer to house: millennials who’ve benefited from household wealth….

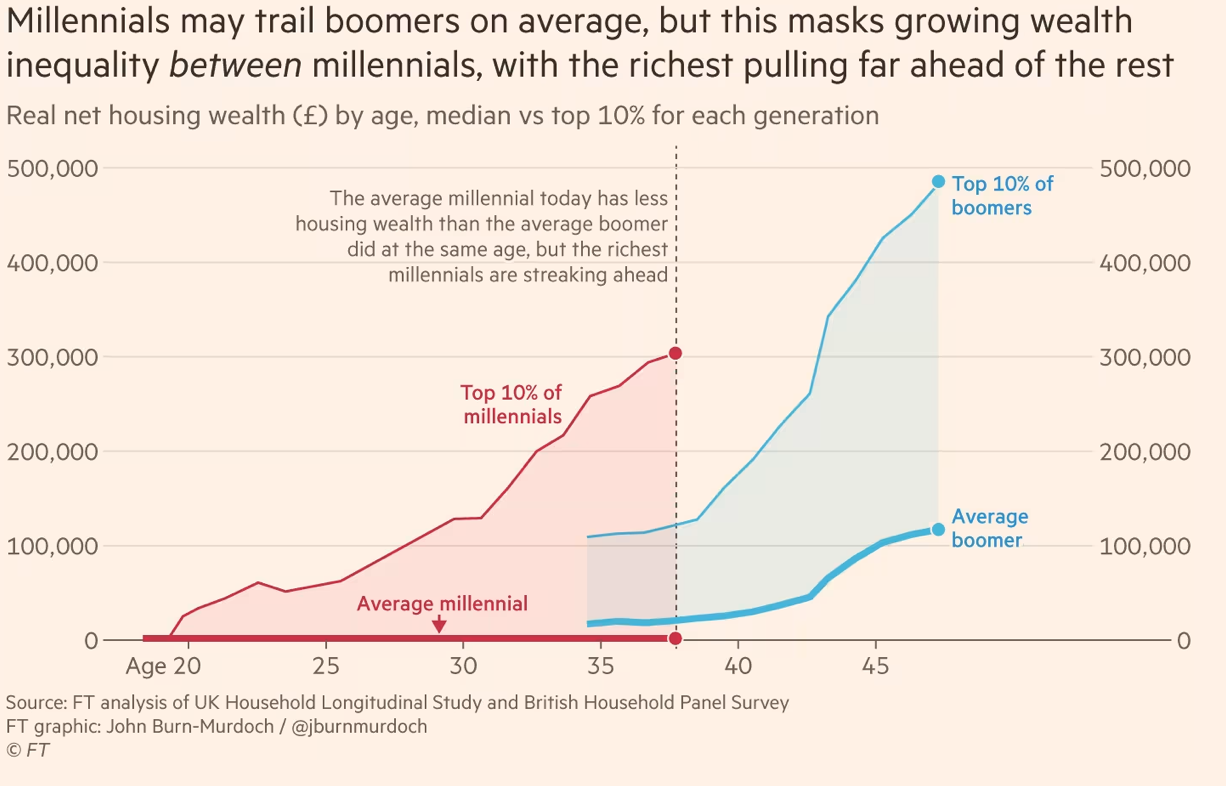

Within the UK and US alike, the typical millennial had amassed much less wealth in actual phrases by their mid-thirties than the typical boomer on the identical age. However this mixture image obscures what is occurring on the prime finish of the distribution.

Within the US, whereas the typical millennial had 30 per cent much less wealth than the typical boomer by age 35, the richest 10 per cent of the cohort at the moment are about 20 per cent wealthier than their boomer counterparts had been on the identical age, in line with a current research by researchers in Cambridge, Berlin and Paris. Not all millennials are created equal.

My evaluation finds the same image within the UK. The common millennial nonetheless has zero housing wealth at some extent the place the typical boomer had been constructing fairness of their first house for a number of years. However the prime 10 per cent of thirtysomethings have £300,000 of property wealth to their names, nearly triple the place the wealthiest boomers had been on the identical age.

So, whereas it’s true that in each international locations the typical younger grownup right this moment is much less nicely off than the typical boomer was three a long time in the past, that deficit is dwarfed by the hole between wealthy and poor millennials, which is widening yearly…

The truth that some thirtysomethings now personal expensive houses in London, New York and San Francisco, regardless of it taking the typical earner 20 to 30 years to avoid wasting up the required deposit in these cities, provides away the open secret of millennial success: substantial parental help.

Analysis from property dealer Redfin in February confirmed that 36 per cent of younger People had monetary assist from household when shopping for their first house…

Bee Boileau and David Sturrock on the Institute for Fiscal Research discovered that greater than a 3rd of younger UK householders acquired assist from household. Even amongst these getting help there are big disparities, with essentially the most lucky tenth every receiving £170,000, in contrast with the typical reward of £25,000.

{kind=link}

Parental help of house buys is a type of key details out within the open the place weirdly few have related the dots. I’ve to confess to it not registering with me what number of of my buddies casually remarked that they’d purchased a condominium or home for one in every of their youngsters, or alternatively, made a stealthy massive contribution whereas the kid depicted the fairness as all theirs. Even the house I simply offered, my mom’s in Alabama, was bought by a pair who’d offered their home in Charlottesville very nicely and thus might simply have purchased a pricier home (they’d missed out on a number of bids). Even so, they plan a really massive renovation and the spouse’s mom, who lives close to by, deliberate to kick in.

This wealth hole is one more side of the collapse in revenue mobility within the US. It has been true since a minimum of the early 2010s that these born into the underside 40% of the revenue distribution have nearly no probability of shifting out of that backside group. We at the moment are seeing much more stratification and ossification on the prime.

[ad_2]