{kind=link}

[ad_1]

What does the current enhance within the federal property tax exemption, plus the introduction of portability, imply for the conventional method to property planning utilizing the AB belief? You might discover that your purchasers are involved that their property planning technique is now not related. Or maybe they only don’t need to spend the money and time to have an legal professional overview their paperwork when federal property legal guidelines might stay in flux.

Given these components, is AB belief planning nonetheless efficient, particularly when it comes to attaining sturdiness and suppleness? Let’s begin by taking a look at precisely what this conventional planning technique encompasses, in addition to among the benefits and drawbacks in contrast with different methods.

How AB Belief Planning Works

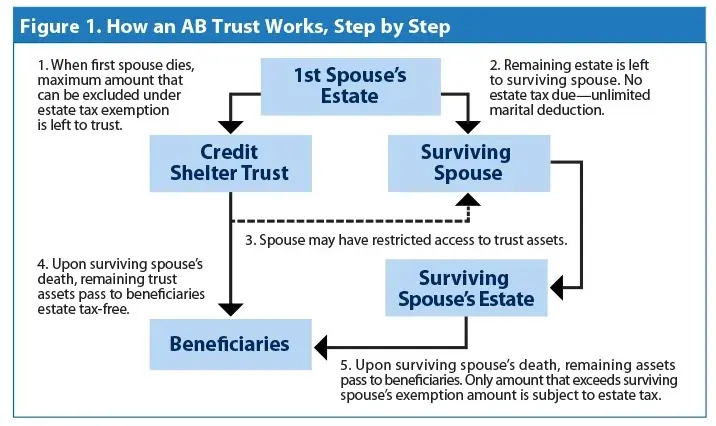

With an AB belief design (aka “bypass” planning), when the primary partner dies, the bypass belief is funded with an quantity equal to the relevant exclusion quantity as a way to reduce federal and state property taxes. Any remaining marital property would switch to the surviving partner outright or be held in belief for his or her profit (see Determine 1).

Belongings owned by the deceased partner obtain a foundation adjustment at his or her dying. The marital property which might be included within the surviving partner’s property get an extra foundation adjustment on the surviving partner’s dying. Though the bypass belief avoids property tax, property held on this belief do not obtain a foundation adjustment when the second partner dies. However the future development of those property stays outdoors the gross property on the dying of the second partner.

A lot of your purchasers probably have an AB belief design in place. Typically instances, they comprise rigid funding formulation that drive substantial property owned by the deceased partner into the bypass belief to attenuate taxes. However with the federal property tax exemption quantity steadily rising—now at $5.49 million—a surviving partner might really feel “disinherited” and left with much less management over the property on the first partner’s dying. A surviving partner, with or with out inspecting the belief’s provisions with an legal professional, may resolve to scrap this funding plan totally and extra towards a extra simplified method.

A Transfer Towards a Simplified Method?

Portability. The present federal portability provision has given rise to a extra simplified method to belief planning. This provision permits the primary partner to depart all of his or her property to the surviving partner. For instance, for federal property tax functions, at right this moment’s $5.49 million exemption quantity, a pair can shield $10.98 million with out utilizing AB belief planning. In consequence, a lot of your purchasers might need to implement this simplified method, usually working with a joint belief established by each spouses slightly than two separate trusts. The benefit? Everything of the couple’s property—these left by the deceased partner and people of the surviving partner—will obtain a foundation adjustment on the surviving partner’s dying.

Disclaimer provisions. Many attorneys draft extra flexibility into the belief by utilizing a disclaimer provision for federal tax planning. With a disclaimer belief, when the primary partner dies, the surviving partner receives the belief property. The surviving partner then has the chance to make a disclaimer election, whereby the belief directs the disclaimed property to the bypass belief. This enables the surviving partner to make use of all or a portion of the deceased partner’s property tax-applicable exclusion quantity. Additional, it might deliver purchasers peace of thoughts, as they don’t must decide to mechanically funding the bypass belief.

Right here, ensure the consumer understands the planning accountability left to the surviving partner.

-

Will the surviving partner have to look at the tax image and execute a disclaimer to attenuate taxes?

-

Does the surviving partner perceive the character of the election?

If not correctly educated about the advantages of this planning choice, the surviving partner may find yourself believing that she or he has been disinherited by executing a disclaimer and permitting property to be positioned within the bypass belief.

Don’t Overlook State Property Planning

Take into account that some states haven’t adopted portability, and lots of states have carried out property tax laws with considerably decrease exemption quantities. In consequence, the standard AB belief technique stays a legitimate answer for preserving the provision of the state tax exemption between spouses. Let’s take a look at an instance to assist illustrate this level.

Massachusetts has a $1 million property tax exemption. A pair with a mixed property of $2 million places in place an easier property plan, leaving the property to the surviving partner upon the primary partner’s dying.

On this situation, there can be no Massachusetts property tax (or federal property tax) due to the limitless marital deduction. Having relied on the portability election, the property wouldn’t incur federal property taxes on the dying of the surviving partner. But when the surviving partner’s property was nonetheless $2 million, it will be topic to Massachusetts property tax. Why? As a result of the primary partner to die misplaced the chance to guard his or her $1 million exemption quantity, which might due to this fact not be obtainable to the surviving partner. So as a substitute of defending $2 million from taxes, the couple might shield solely $1 million.

Backside line? If the couple had used conventional AB planning, they might have eradicated all Massachusetts property taxes, along with federal property taxes.

Extra Benefits

Along with state property taxes, there are different planning benefits to AB trusts:

-

Creditor safety: Safety varies from state to state, so your purchasers ought to seek the advice of with their attorneys to know the restrictions.

-

Safety of subsequent spouses: If a surviving partner remarries and is once more predeceased, the unused exclusion quantity from the primary decedent partner is wasted if portability alone was relied upon for property planning.

-

Spendthrift safety: By planning to put property in an AB belief when the primary partner dies, a pair can predetermine how the surviving partner will profit, along with controlling the property for kids and grandchildren. When a surviving partner remarries and property paperwork are redrafted to offer monetary help to the brand new partner, property could also be comingled. If finished with out cautious consideration to the present and new household construction, kids from the earlier marriage may very well be unintentionally disinherited or might not profit within the method during which the deceased first partner would have wished. In that regard, an AB belief can present for spendthrift safety.

-

No probate: Belongings within the AB belief will keep away from probate when the surviving partner dies.

The Disadvantages

In fact, there will likely be some disadvantages when utilizing the AB belief:

-

No foundation adjustment: Belongings held in a bypass belief don’t obtain a foundation adjustment on the surviving partner’s dying. As such, heirs who inherit these belief property will inherit foundation equal to the honest market worth of the property on the first partner’s dying.

-

The expense: Trusts with extra complicated tax planning provisions, equivalent to AB trusts, are a costlier engagement for the consumer in contrast with different planning choices.

-

Restricted entry to funds: There are advantages to limiting a partner’s outright entry to belief property, however unexpected issues might come up if the partner requires unfettered entry to funds.

-

Compressed belief earnings tax brackets: Given this compression, cautious consideration ought to be given to funding distribution methods.

One Measurement Does Not Match All

Property planning is unquestionably not a one-size-fits-all situation. Relying on the progress of federal property tax laws and the way that can have an effect on the legislative conduct of particular person states, you may assist your purchasers resolve whether or not the standard AB belief or a extra simplified method most closely fits their wants. It is probably not potential to realize all of their planning aims. As an alternative, to get near attaining their aims, it might be a matter of fastidiously analyzing and weighing the professionals and cons of the varied tax planning methods when it comes to your purchasers’ private beliefs and objectives.

Commonwealth Monetary Community® doesn’t present authorized or tax recommendation. You must seek the advice of a authorized or tax skilled concerning your particular person scenario.

[ad_2]